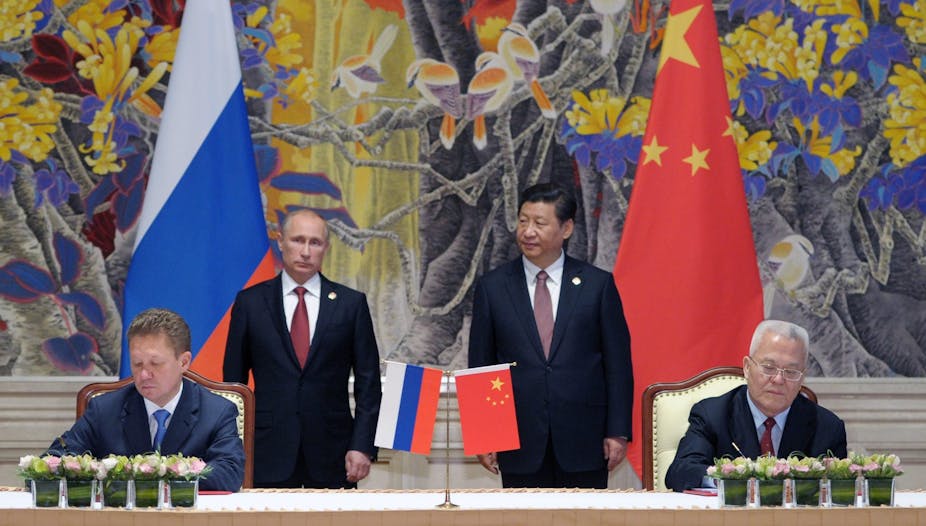

The US$400 billion gas deal signed between Russia’s giant state-owned corporation Gazprom and China last week is 16 times larger than its predessor in the supply of gas to China - a US$25 billion LNG project based on offshore Western Australian gas signed more than ten years ago.

To put it in context, the project will transfer 38 billion cubic metres (bcm) of gas per year, which is close to a third of total Russian pipelined exports to Europe, and compares with the 592 bcm/y of total Russian production in 2012.

As with Australian and other suppliers, Russia, with the world’s largest gas reserves, is seeking similar Asian markets including Japan, which currently imports a total of 119 bcm of LNG per year. In 2012 Australia exported 28 bcm of LNG of which 20 bcm went to Japan.

So should Australia be seriously concerned about the deal? One comment from the industry was that Australia’s LNG exporters must cut their costs in the face of an increasingly competitive Asian market (and despite the lucrative high prices still ruling there in the shorter term).

Diversifying China’s gas sources

China is already close to taking delivery of gas pipelined from the Central Asian republic of Turkmenistan, and Russian supplies of conventional gas to China can be viewed as competing also with non-conventional gas from sources such as Eastern Australia (coal seam gas), and the US (prospective shale gas exports to Asia). China itself has a non-conventional gas resource twice the size of that estimated for the US, but not without significant environmental challenges and constraints.

Asian and other gas importers also stand to benefit from normalisation of Iran’s international status, assuming this can be achieved as a result of current negotiations designed to curb Iran’s nuclear weapons aspirations. Iran is the world’s largest holder of conventional gas resources after Russia. The team negotiating with Iran on the nuclear weapons issue significantly includes both Russia and China, as permanent members of the UN Security Council along with the US.

The Russia-China gas contract is take-or-pay and the price of the contract price for the gas is to remain linked to international oil prices rather than to spot gas prices. China has obtained other important concessions in return.

A sensitive political dance

With this pipeline deal, the US is now looking at a multidimensional agreement between two great powers, Russia and China, often designated (however problematically) as its “adversaries”. The arrangement has also been viewed as part of a Russian “pivot” to the East countervailing the much vaunted US version.

Meanwhile in the context of the Ukraine crisis, some US figures had urged export of LNG to the European Union based on the vastly expanded US shale gas resource. This would supposedly undercut Russia’s access and influence in the EU. This threat was hard to sustain given the long infrastructure lead times involved, the competitive strength of Gazprom, and the Russia-EU gas grid already in place and developing ─ notably to reduce dependence on the gas transit state of Ukraine.

More lucrative markets for US-sourced LNG beckon in Asia where gas prices have been as high as $18/GJ compared with only $5/GJ in the US (1 Gigajoule = 0.95 million British thermal units). This gap reflects the time-lags in constructing relevant infrastructure to liquefy and ship the LNG. Also at issue are the transport and handling costs for LNG versus those for transcontinental pipelined gas. These potential US LNG exports are said to trail planned Russian pipelined supplies to Asia by 3-4 years.

Geopolitically, all this is against a background of an increasingly “multipolar” international system of states, including emerging or resurgent Eurasian “great powers”. It is easy to forget just how weak both Russia and China were relative to the US, even as recently as 2000. Since then the Chinese economy has by 2014 become the world’s largest now ahead of the US (on a GDP/PPP basis).

Similarly, 15 years ago Russia’s GDP had been no more than that of Mexico. Now the Russian economy has displaced Germany to be ranked fifth. As the world’s largest gas exporter and second largest oil exporter, this reordering in part reflects that oil prices have been sustained since the mid-2000s at five to 10 times those in 1998, a year of severe financial crisis for both East-Asian and Russian economies. Ironically, that sustained high oil price has in large measure been due to demand from the thriving Chinese economy.

Indexing of export gas contract prices to oil prices as in the present deal might turn sour for Russia if oil prices were to collapse. Russia’s future would also seem to remain under severe pressure from a potential prolonged civil war within Ukraine and other near neighbours, all viewed as elements of NATO-led “encirclement”, and also as US interference in mutually beneficial Russian-EU economic relations.

Such “encirclement” is analogous to ongoing but perhaps ill-advised US attempts to “contain” China (its greatest financial creditor). The latter is a US strategy given spurious legitimacy by perennial disputes between China and its neighbours in the South and East China seas. These disputes are linked to national energy security concerns because of suspected petroleum resources in the region. These indeed dangerous tensions should be somewhat relieved by diversifying gas supply sources ─ not only China’s but those of Japan and other Asia-Pacific petroleum-importing states.

As a major gas exporter, Australia can play a part in this supply diversification. As a middle-range power having an interest in stability in this dynamic region, there is an increased questioning of its existing foreign policy of “strategic dependence” on the US. Drawing on both of these roles, Australia is also well suited to play a positive international role in mitigating climate change.

Carbon reduction the elephant in the room

Perhaps the greatest single concern about global CO2 emissions growth internationally is the continuing expansion of already large coal-based generation in China. An obvious alternative is gas-fired CCGTs with CO2 emissions (per kWh) only half those from coal. Such generation also produces much reduced levels of toxic air pollution ─ a major advantage given the mass protests around these concerns in China.

Gas-fired generation in China thus holds considerable promise for cost-effectively mitigating global climate change. End-use efficiency improvement and, over time, a range of zero-emissions technologies must be brought to bear. But the good news is that gas-fired CCGTs are much more compatible with renewable technologies than is coal. IEA scenarios for China (see graphic below) indicate scope for major increases in use of gas, along with other adjustments necessary to meet the key 450 ppm limit in CO2e levels in the atmosphere (the ‘other’ category refers to non-hydro renewables). Specifically, the gas share in electricity generation increases from 2 % in 2011 to 5 % in 2035 under ‘current policies’ but under the ‘450 ppm’ scenario the 2035 gas share doubles to 12 % but of a smaller total of electricity units generated. However, there is scope for a significantly larger gas share. This could occur if there is a more rapid backing out from coal-fired generation, for example due to the politics of air pollution; or if there turn out to be significant obstacles to the foreshadowed rapid increase in nuclear electricity generation.

One important proviso in this climate-based argument for expanding imported gas is about limits on CO2 and fugitive methane emissions right along the supply chain prior to combustion. Satisfaction of this condition is more likely if there is a suitably concerted approach by the major national climate stakeholders such as the US, China, Russia ─ and not least, Australia.

Such an approach is also consistent with the case for establishing a “Concert of great powers” in the Asia-Pacific, an arrangement in which regional middle powers would also play a role.

This kind of arrangement would not only be a superior geopolitical alternative to “containment” and “encirclement”, it could also provide an essential forum and mechanism for mitigating climate change before that issue becomes one in the dysfunctional, competitive and militarised geopolitics of an “adaptation only” response to catastrophic climate change.