An issue that has been creating significant friction within the Liberal National Party (LNP) coalition is the deregulation of the Australian wheat industry. In recent weeks we have seen threats by West Australian (WA) Nationals MP Tony Crook and WA Liberal Senator Dean Smith to cross the floor over the issue. What has emerged is a somewhat bizarre situation in which the Federal LNP is seeking to block, or at least delay for several years, a move by the Federal Labor Government to deregulate the wheat industry in line with recommendations from the Productivity Commission.

The matter is a potentially serious threat to the internal cohesion of the LNP. Deputy Opposition Leader Julie Bishop is at odds with members of the WA Liberal Party over the issue. At the heart of this political row is the divide between farmers in the west and their counterparts in the east. For the WA growers the demand for immediate market deregulation is strong, but for their colleagues in other states the opposite is true.

What then is going on?

A brief history of the Australian wheat industry

Australia’s wheat industry is as old as the nation with the first successful harvest taking place in New South Wales in 1790. The introduction of new disease and drought resistant varieties of wheat, and mechanisation such as the Sunshine Harvester, in the late 19th Century saw the expansion of the industry. However, the growth of Australia’s “Wheat Belts” took place during the last century, with much of the production occurring in the South West and South East of the country.

A key feature of the Australian wheat industry in early 20th Century was the emergence of bulk handling and storage businesses to deal with the supply chain, and statutory marketing boards with “single desk” control over domestic and international grains pricing and distribution. For example, during the period from 1910 to 1960 bulk wheat storage and handling businesses were established across Australia.

In New South Wales, Victoria and Queensland this took the form of State Government owned authorities. By contrast, in Western Australia and South Australia farmer owned co-operative bulk handling businesses were established and given monopoly control over bulk wheat and later some other crops under state legislation.

WA’s Co-operative Bulk Handling (CBH) Group was established in 1933, while the South Australian Co-operative Bulk Handling (SACBH) was founded in 1954. SA growers had sought to establish a co-operative bulk handling business in the 1920s but had been blocked within State Parliament by politicians concerned over the creation of a powerful monopoly.

Single desk marketing authorities were created in the late 1930s and early 1940s in response to the Great Depression and World War Two. The Australian Wheat Board (AWB) first emerged during the World War One on a temporary basis, but was permanently established in 1938.

Grower control within this system was strong, with farmers owning and controlling the likes of CBH and SACBH, and having significant influence over the operations of the Grain Elevators Board of Victoria, Grain Handling Authority of NSW and Bulk Grain Queensland. The statutory marketing boards such as AWB and the Australian Barley Board (ABB) held exclusive rights to buy specific types of grain.

The state-based bulk handling authorities and grower co-operatives were given monopoly rights to receive these grains under state legislation. Even the mode of transportation was controlled by law with the state-owned rail systems getting preference over road transport.

Australia’s approach to grain handling was different to that undertaken in Canada and the United States. Those countries made much greater use of on-farm storage with growers delivering grain to the handling system at different times throughout the season. It was the combination of state intervention and the creation of farmer owned co-operatives that made the difference here.

The deregulation movement commences

By the 1980s pressure for market deregulation was mounting on the Australian wheat industry. This was driven in part by the Australian Industries Assistance Commission (the forerunner of the Productivity Commission). Since the late 1970s the Commission had been pushing to have the monopoly control of AWB over all wheat exports removed. A key protagonist in favour of market deregulation was Trevor Flugge, then President of the Australian Wheat Growers’ Federation in 1983, who was later to become the Chairman of the AWB.

In 1988 a Royal Commission was held into the grain storage, handling and transport system. This was driven primarily by inefficiencies within the state rail authorities in the eastern states of Australia. Variations in rail gauges and poor coordination between systems meant that it was cheaper to move grain to port by road than rail.

This was followed by the Federal Government’s Wheat Marketing Act 1989. This legislation led to the loss of monopoly control by the bulk grain handling organisations. It also gave the grain marketing authorities such as AWB and ABB the freedom to broaden their range of grains from single varieties (e.g. wheat or barley) to a much wider pool. In WA this also included the Grain Pool WA.

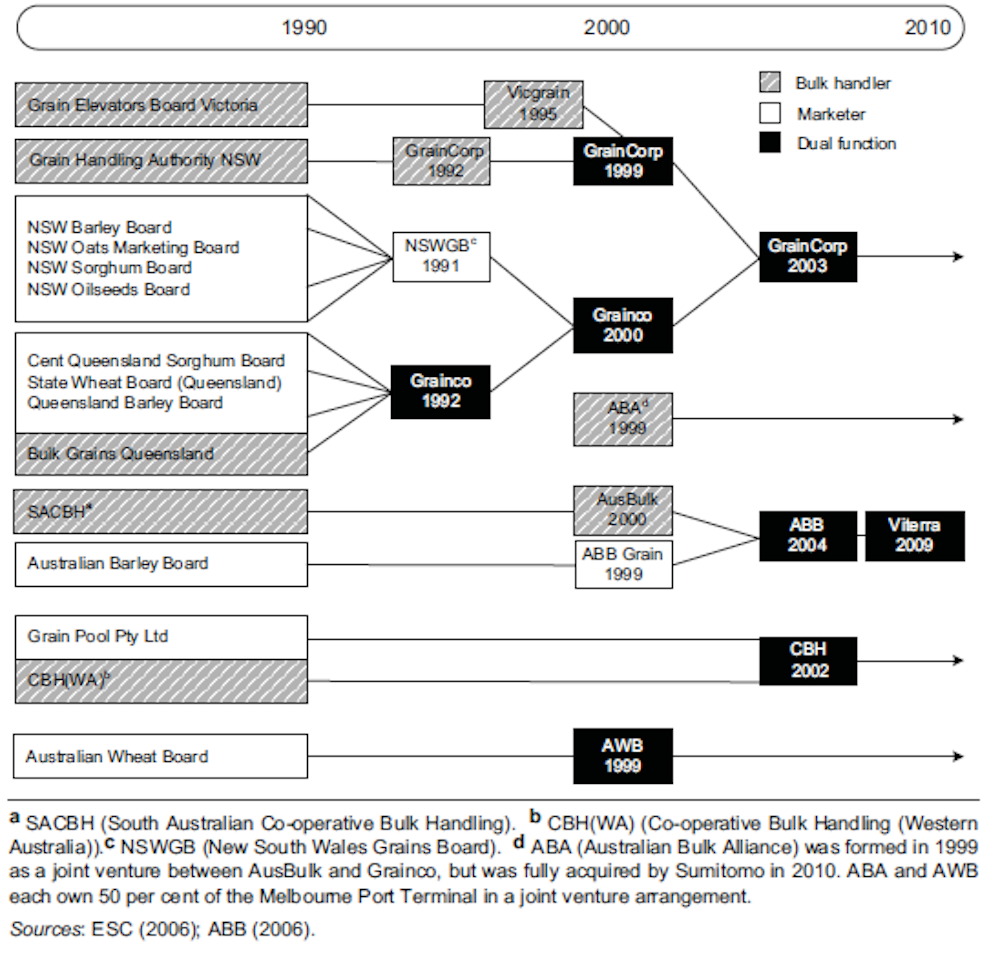

As shown in the figure below, by the early 1990s there were 15 separate organisations involved in the grains industry. This included the five bulk grain handlers and 10 marketing authorities. Over the course of the next two decades the pace of market deregulation accelerated. By 2000 there were only six organisations and by 2010 only four. Of these only CBH has remained a co-operative enterprise owned and controlled by the farmers.

In South Australia the growers’ co-operative SACBH was partially demutualized in 2000 when it was restructured as AusBulk-United Grower Holdings (UGH). It was then merged with the newly privatised ABB Grain in 2004 to become a shareholder owned business that was subsequently listed on the Australian Stock Exchange (ASX). Despite initial hopes that ABB Grain could remain in grower hands, by 2009 this former co-operative had been acquired by Canada’s Viterra. In March 2012 Viterra was negotiating with Anglo-Swiss commodities trading giant Glencore to accept a take-over offer of approximately $6 billion.

In NSW, Victoria and Queensland the various state-based bulk grain handling authorities and grain marketing boards merged to form GrainCorp now a publicly listed company. The privately owned Australian Bulk Alliance (ABA) was established in 1999 and was acquired by the Emerald Group Australia (a grain marketing business that is 50% owned by Japan’s Sumitomo) in March 2012.

In WA the merger between CBH Group and the Grain Pool of WA in 2002 gave the co-operative its own marketing arm. This was consistent with the merger of AusBulk-UGH and ABB Grain in South Australia in 2004 and GrainCorp and Grainco in 2003. CBH has also invested in joint ventures to provide it with flour mills in Asia and its own shipping line and rail operations. Today CBH is Australia’s largest co-operative enterprise with 4,500 members, around 1,000 full time employees, net assets of $1.1 billion and an annual turnover of $1.3 billion.

AWB and WEMA

A key actor in the Australian wheat industry has been AWB. Privatised in 1999 it became a grower owned business and listed on the ASX in 2001. The privatisation of AWB saw the creation of the Wheat Export Authority (WEA) that took control over the regulation of wheat exports from Australia. AWB’s previous “single desk” monopoly control over wheat export was transferred to its subsidiary AWBI, which had veto power over bulk wheat exports by other organisations.

The “Oil-for-Food” scandal involving AWB and AWBI in the murky dealings of former Iraqi leader Saddam Hussein broke in 2006. This led to intervention by the Federal Minister for Agriculture to assume the power of wheat export control and remove AWBI’s right of veto over wheat exports by other organisations.

When the Labor Government of Prime Minister Kevin Rudd took power in 2007 these issues were still in play, and the subsequent Commonwealth Wheat Export Marketing Act 2008 (WEMA) became the principle legislation regulating Australia’s wheat exports. It was complemented by the Wheat Exports Accreditation Scheme (2008) that grants approvals to organisations to export wheat.

The Productivity Commission Report into the wheat industry of 2010 noted grower concerns over the removal of the “single desk” arrangements. Their key concerns were:

1) Low prices and increased price volatility;

2) Loss of Golden Rewards and a return to ‘cliff-face pricing’;

3) Cost and complexity of selling in a competitive market;

4) Increased risk to growers associated with pricing and marketing;

5) Loss of forward hedging, resulting in lower returns to growers;

6) Loss of efficiencies by having more than one entity to control supply and throughput of wheat, resulting in higher storage and transport costs;

7) No buyer of last resort;

8) No payment security; and

9) No real competition between traders, and in some cases a reduction in the number of buyers at harvest.

The Productivity Commission’s study revealed a clear divide between wheat growers in WA and their counterparts in the other states. As the following quotes reflect:

How can the de-regulated system work, when you have 20 plus grain companies trying to secure markets for their wheat before they have actually purchased it? At this moment, most wheat harvested in Northern New South Wales has been warehoused or stored on farm. Most grain trading companies have offered a ridiculously low price at silos for this year’s harvest, hoping to take advantage of growers needing early cash flow and also know that everyone will eventually have to sell. (Dalkeith Warialda, sub. 4, p. 1)

The path of deregulating and rationalising the wheat industry in Australia is progressing, and in general, PGA is pleased with the progress. We as an industry are still working through the remnants of the regulated wheat export markets of our past, and hopefully, within the next three years, we will easily arrive at a fully de-regulated and competitive market. Until then, we must be vigilant that those remnants of the past do not cause us to be pulled backwards instead of moving strongly and competitively into the future. (Pastoralists and Graziers Association of Western Australia sub. DR81, p.6)

While most growers see the merit of market deregulation over the longer term, their differences of view relate to the type of competitive environment in which they operate. While the growers in WA have a degree of protection afforded by their membership of CBH Group, the environment for their counterparts in the others states is more complex.

In general growers felt that their interests would be best served by a national pool managed as a grower-owned co-operative. Since the market deregulation process commenced in the 1990s a number of grower co-operatives have emerged to help farmers gain more bargaining power over the major grain traders. However, few have the size, financial strength and sophistication of these large national and international businesses. The exception is the co-operative CBH Group.

Disclosure: Tim Mazzarol receives research funding from Co-operatives WA and CBH Group however his opinions are his own and do not reflect the official position of these organisations.