Tens of thousands of protesters in red shirts took over the streets of Brasilia on August 15, the last day to register candidacies for the upcoming presidential elections. They were demanding that the Supreme Electoral Court accept the bid of Lula da Silva. Held captive in a cell in the southern city of Curitiba, the former president could only assert his political rights through an op-ed in the New York Times.

Lula remains the most popular politician in Brazil. The memory of economic prosperity under his government makes him favourite to regain the presidency, if only he is allowed to run. While that remains unclear, now that the presidential race is officially underway, the sluggish economy will be at the centre of the political debate either way.

The unemployment rate is above 12% and poverty and extreme poverty are on the rise. For the fifth year in a row, Brazil will run a sizeable primary budget deficit. A recent study linked the current government’s rash austerity measures to increasing child morbidity and mortality. The key question all presidential candidates will have to answer is, how they can bring back the booming performance that made Brazil one of the BRICS.

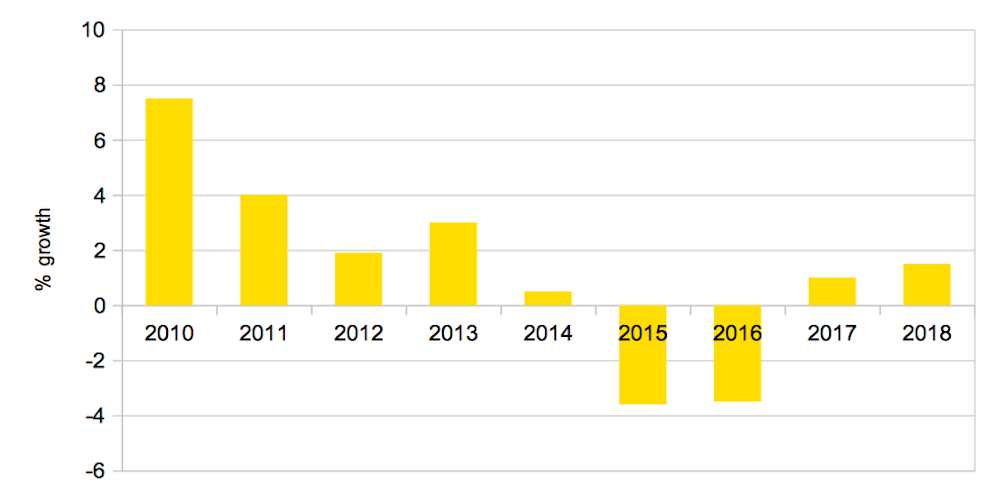

Two years ago, in an article for The Conversation, I claimed that the Brazilian economy was “in for an upswing”. Against prevailing pessimism, I suggested the country would rapidly recover from the steep decline of 2015 and 2016, when GDP contracted by almost 8% – arguably Brazil’s worst recession on record.

Stretching my argument to the limit, I predicted that an imminent recovery would “put whoever emerges victorious in the current political dispute in an excellent position to go on and win the 2018 election”. It is hard to see how I could have been more mistaken.

GDP grew by only 1% in 2017, and the IMF has just revised down its projection for this year to a modest 1.8%. Per capita GDP is now close to US$11,000 (£8,655) – the same as ten years ago. The government’s candidate, Henrique Meirelles can command no more than 1% of voting intentions, and risks having to abort his presidential ambitions altogether.

False dawn

Earlier this year, it looked like economic recovery was finally on track. Brazil’s stock exchange started 2018 on a strong upward trend, anticipating the good results expected for the real economy. The Bovespa index – including all the Brazilian blue chips – rallied to a historical high, following Lula’s imprisonment in April. The IMF was forecasting an economic expansion of 2.3% for the year. Meirelles appeared on television spots as finance minister, selling optimism and setting the stage for his political campaign.

Yet all that seemed solid then melted into thin air. First, the government failed to pass a draconian reform of the pension system aimed at curbing spending. In May, following the economic crisis in Argentina, foreign investors fled the Brazilian stock markets in droves, wiping away the gains of the year and weakening the real against the dollar.

Finally, a traumatic truck drivers’ strike brought the country to a standstill for an entire week in June, paralysing production lines. Market forecasts are now revising down GDP expectations, amid rising inflation and a rapidly deteriorating fiscal situation.

Brazil’s GDP, 2010-18

But why didn’t the current crisis follow the same pattern as 1998, 2002 and 2008 – to mention just the most recent jolts – and quickly pick up? Why is the rollercoaster cart stuck near the bottom of the track? What can the next president do to set the economy in motion again?

State of the nation

After taking office in 2016, the centre-right president, Michel Temer, embarked on a misconceived and poorly executed reformist agenda, which has failed to fix deeply entrenched economic imbalances or reignite growth. At the same time, the impeachment process against his predecessor, Dilma Rousseff, largely seen as a coup by the left, has proved more traumatic than anticipated by the middle class and the political actors that pushed for it.

Temer imposed a strong cap on annual spending, constitutionally limiting it to 2015 levels in real terms for the next two decades. This forceful austerity was deeply unpopular among Brazilians but well received by the financial markets. Nevertheless, its targets look increasingly unrealistic. To meet them, the next government would have to impose painful social spending cuts, starting with the ill-fated pension system reform, with dramatic social and political consequences.

Left and centre-left candidates such as Guilherme Boulos and Ciro Gomes explicitly reject that option. Even if a pro-market candidate such as Geraldo Alckmin becomes president, the spending cap rule will probably be revisited. The scenario is totally unpredictable if extreme-right candidate Jair Bolsanoro emerges victorious in October. Recently converted to economic liberalism, Bolsonaro, a former army captain, made his political career confronting minorities’ individual rights and defending the corporate privileges of the army. It is difficult to see how he would live up to the high expectations of his passionate followers, while also enforcing fiscal austerity.

To complicate things further, the current president, who is not seeking re-election, slashed labour rights and defunded trade unions in the hope of bringing down production costs and creating new jobs. The reform was imposed without negotiation, triggering job insecurity and opposition from labour-court judges.

In the absence of growth or investment, the expected explosion of new jobs simply did not happen. Worse, the downward pressure on salaries and the renewed risk of unemployment thwarted any possibility of a consumption-led recovery in the short term.

To revive the economy, Brazil is therefore down to relying on a surge in private investments or external demand. Again, the prospects are grim. Donald Trump’s trade war will potentially harm global demand, while the permanent instability created by the impeachment process and the fragile allegations against Lula has made investors cautious until they see the election results. The claim that Brazil’s government and judiciary are working well is becoming increasingly untenable, which is not helping the investment mood.

What next? My flawed predictions of two years ago should warn me against the pitfalls of economic forecast. Clearly Brazil’s immense potential is no guarantee of good economic performance. Only a couple of months until the elections, the frontrunner is behind bars and the economic agenda of the next government is anyone’s guess.

Let’s hope that recovery will not be hindered once again by more botched austerity reforms and the further deterioration of the country’s democratic institutions. With the world economy facing turbulence, it is difficult to imagine a way forward under the next president if domestic demand remains compressed.