The days leading up the budget are hectic as many in the Treasury are busy devising financial gimmicks to please the electorate. This forthcoming budget is particularly important as next year’s budget will be too close to the election to have much of an impact on the economy or the “feel-good factor”. Government politicians are also busy revelling in good economic data including a return to economic growth and falling unemployment. The chancellor has been telling colleagues that “we have won”. Have they?

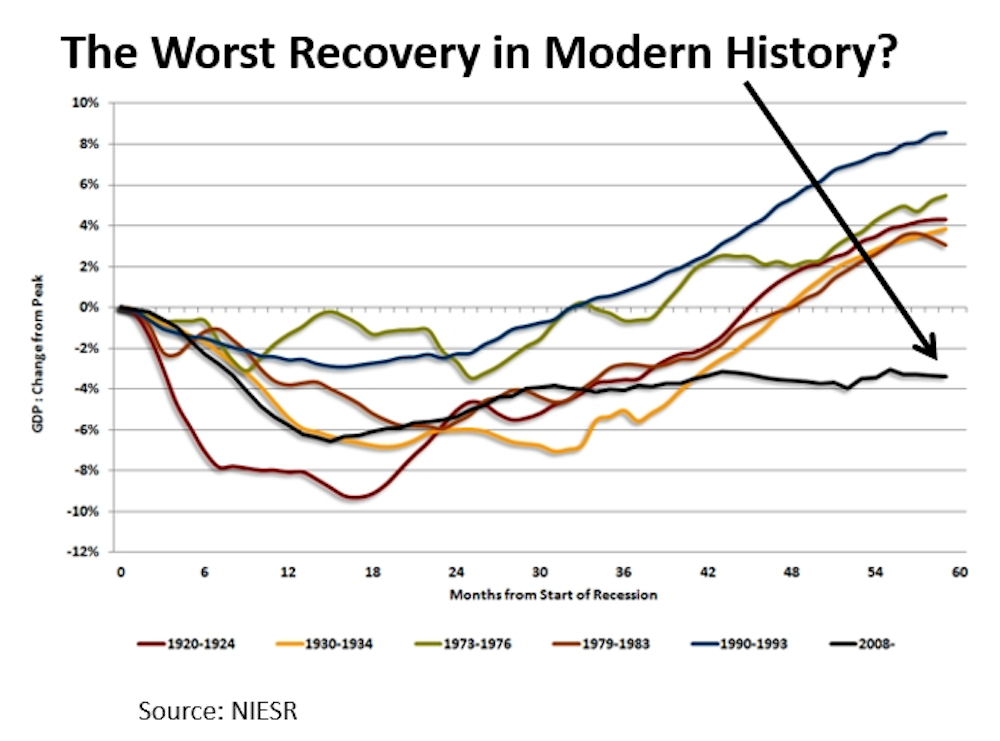

No return to normal

There is less rosy picture when you scratch beneath the surface of a few months’ worth of economic data. Take the economic growth figures: GDP is expected to grow between 2.5 and 3.0% in 2014. On the face of it, this is a return to normal as this is broadly the long-term growth rate since the industrial revolution. But it is not normal, as after a deep recession a significant bounce-back is expected; normality would be a growth rate of between 4 and 5% per annum.

Take the recovery from the Great Depression in the 1930s; from the five years from 1932 to 1937 the economy growth at an annual average rate of 4.2%. But we are not witnessing a big bounce-back now – instead we are in the midst of the worst recovery in more than 200 years. This shows the fundamental weaknesses in an economy with structural flaws.

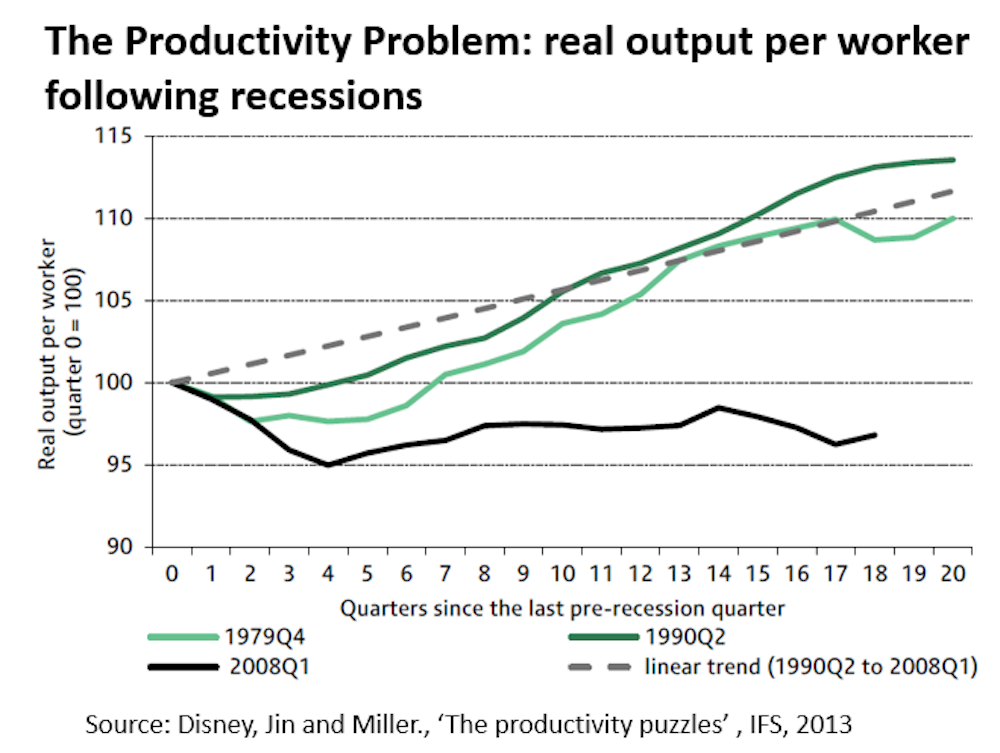

The productivity problem

At least there is good news in the labour market as unemployment is falling and there are now only 2.34m unemployed. Yes, 2.34m – which is 7.2% of the labour force. Times have changed: in the period from 1950 to 1973, unemployment in excess of 3% was considered as an economic failure.

Falling unemployment is good for those who can get a job, but it also reflects a lack of investment in the economy. Falling real wages are encouraging firms to employ more workers, but not to invest in machinery and technology. This has led to a significant decline in productivity – and it is productivity growth that drives long-term prosperity.

Unbalanced Growth

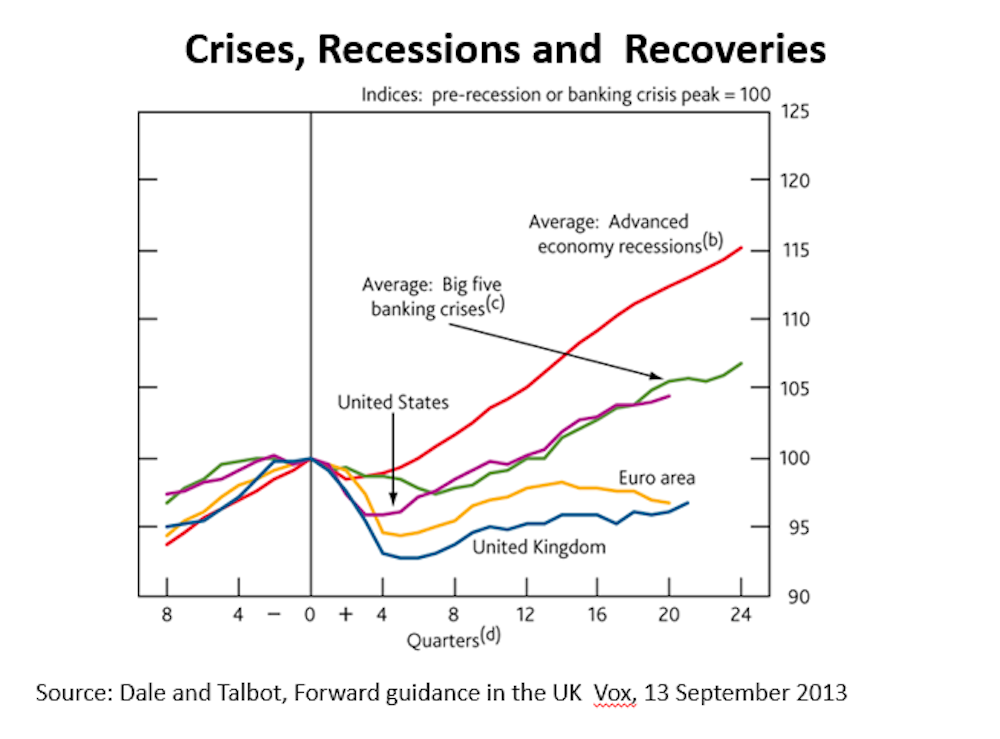

Lack of investment is one indicator of the failure to rebalance the economy. Another is poor export performance, as we do not produce the goods and services that the rest of the world wants. The problem for UK exports in linked to the lack of investment as there is a failure to develop new products and new processes. The current modest recovery is being driven by consumption and household debt. And it is not a sustainable solution to expect long-term growth to depend on those parts of the economy that were integral to causing the financial crisis in the first place.

Policy vacuum

There are two fundamental weaknesses at the heart of economic policy formulation in the UK. First, the focus on the austerity and public sector debts has “crowded out” any significant discussion of a strategy for long-term growth. This does not only apply to the government but also to the opposition. Second, the disparaging rhetoric and propaganda directed at the public sector has distorted understanding of the role of the state in advanced countries.

The lessons of other prosperous countries shows the important role of the public sector in encouraging long-term growth, including: the focus on education and skills in the Nordic countries; and investment in technology and equipment in Germany. Even in the US, the home of free enterprise, the innovation system is managed and controlled by the federal government. Whatever fiscal initiatives emerge from George Osborne’s red box in the Budget, enhancing the role of the state as a driver of growth will not be amongst them.

Has Osborne won? Well, in 2015, the election may show that he has won the political argument. But good politics too often defeats good economics.