The unemployment rate is one of the most closely followed macroeconomic indicators. Of importance in its own right, it tells us about the level of spare capacity in the economy and provides information about likely future developments in inflation.

Recent fluctuations in the unemployment rate have surprised many economists. In July, the unemployment rate jumped by 0.3 percentage points to 6.4% – its highest level in twelve years – only to be unwound in the August release.

The sharp increase in July may partially reflect measurement issues - the Australian Bureau of Statistics (ABS) updated the criteria to be actively searching for a position, although the ABS said the impact of this change was not significant.

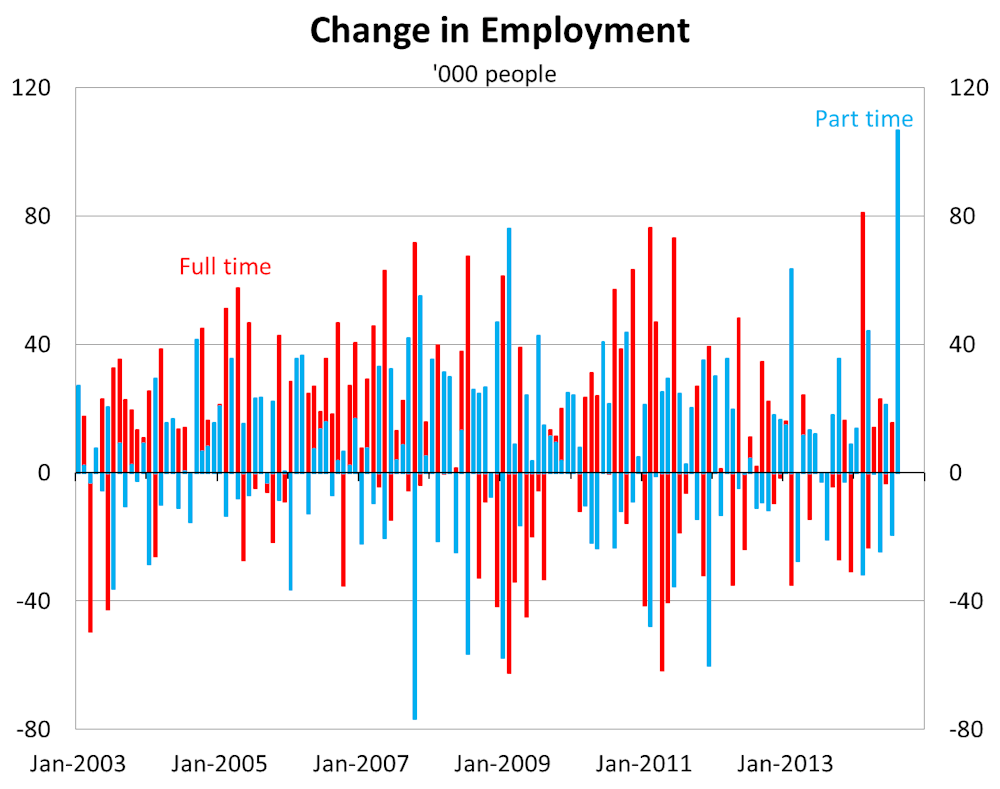

The unwinding of this spike in unemployment in August was due to a surge of part-time employment – in fact the largest growth rate since the mid-1980s. The increase was so large that the ABS extensively checked the figures. However, the lift in part-time employment was evident in many dimensions of the data – it occurred both across the country (with the exception of the Australian Capital Territory) and across many age groups.

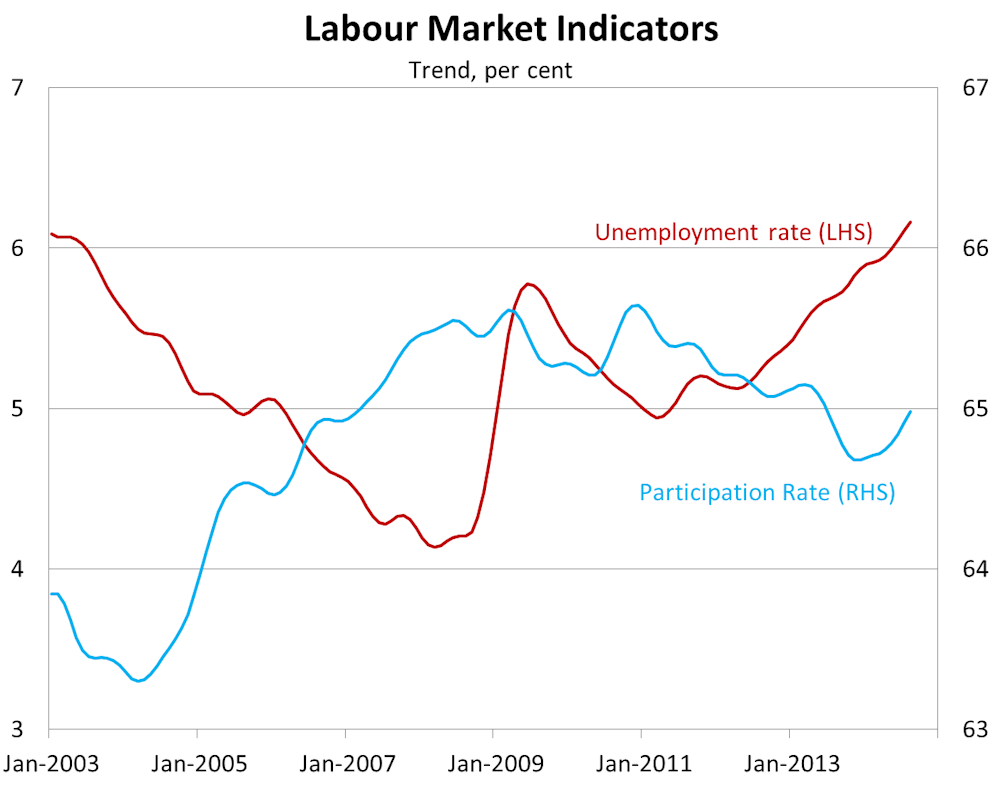

Amidst this considerable volatility, it is probably best to focus on estimates of the “trend” unemployment rate, which is also advocated by the ABS. The trend measure effectively smooths the data, down-weighting the recent observations.

However, trend estimates aren’t perfect – for example, as more data become available they can be revised. Also, by down-weighting the recent data they can miss turning points which policymakers might have otherwise wanted to react to in a timely manner. Bearing these caveats in mind, the trend unemployment rate in recent months has moved higher.

At around 6%, the trend unemployment rate suggests that slack exists in the labour market. Similarly, the trend participation rate – the ratio of people in the labour force (either employed or unemployed) to the population – recently has picked up, but remains below the levels of the late-2000s.

Structural issues

While as discussed in a speech by Reserve Bank of Australia Assistant Governor Christopher Kent part of the decline in the participation rate probably can be explained by structural factors, such as the ageing of the population, a component is likely to be cyclical.

Recent Reserve Bank of Australia model-based estimates also suggest that spare capacity currently exists in the labour market, but much less than occurred during the early-1990s recession. The Reserve Bank study also highlights the considerable uncertainty which surrounds these estimates.

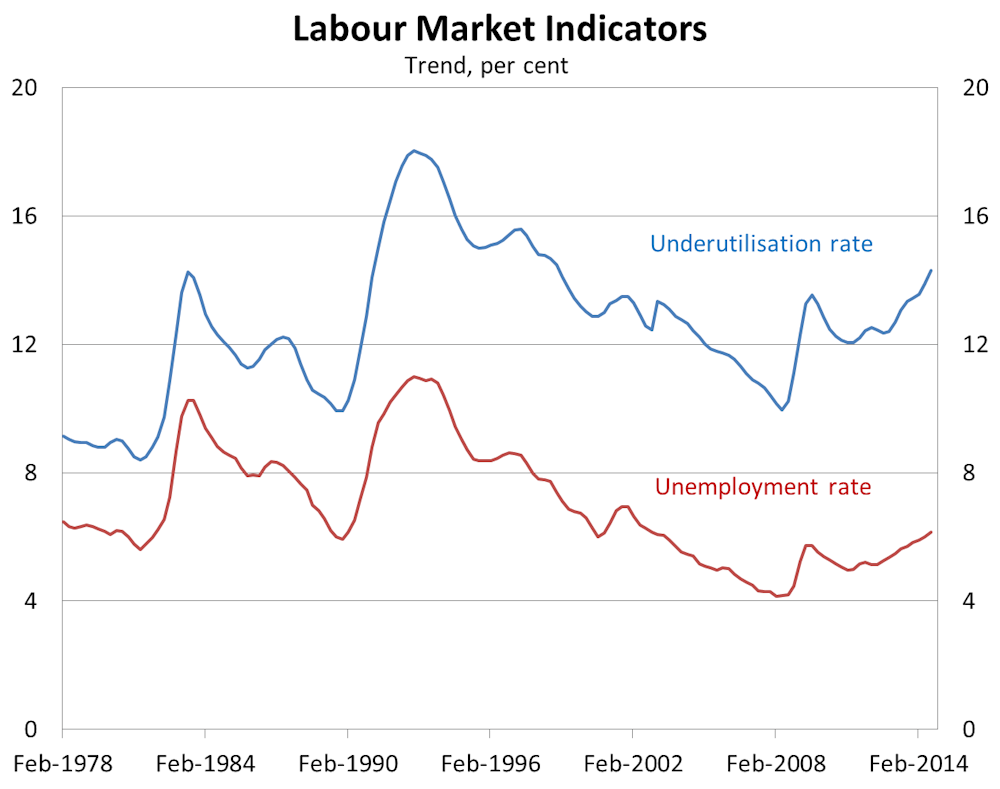

The unemployment rate is a narrow measure of labour market slack – it abstracts both from people working fewer hours than they would like, or in a position that does not fully utilise their skills. The ABS tackles the first aspect in its measure of labour force underutilisation. As it is a broader measure, the labour underutilisation rate is always greater than the unemployment rate, although the wedge between them widened in the early 1990s recession.

We’re getting more ‘flexible’

This wedge widened with the onset of the global financial crisis, unwinding some narrowing in it which had occurred. An important part of the macroeconomic adjustment that occurred in Australia during the GFC was a reduction in average hours worked. This mitigated the rise in the unemployment rate and probably was facilitated by the more flexible nature of the labour market today relative to in the past.

The increase in the labour underutilisation rate over the past eighteen months has outpaced that in the unemployment rate. In the September quarter it exceeded the levels reached during the GFC, although it remains well below the high levels reached during the severe early-1990s recession.

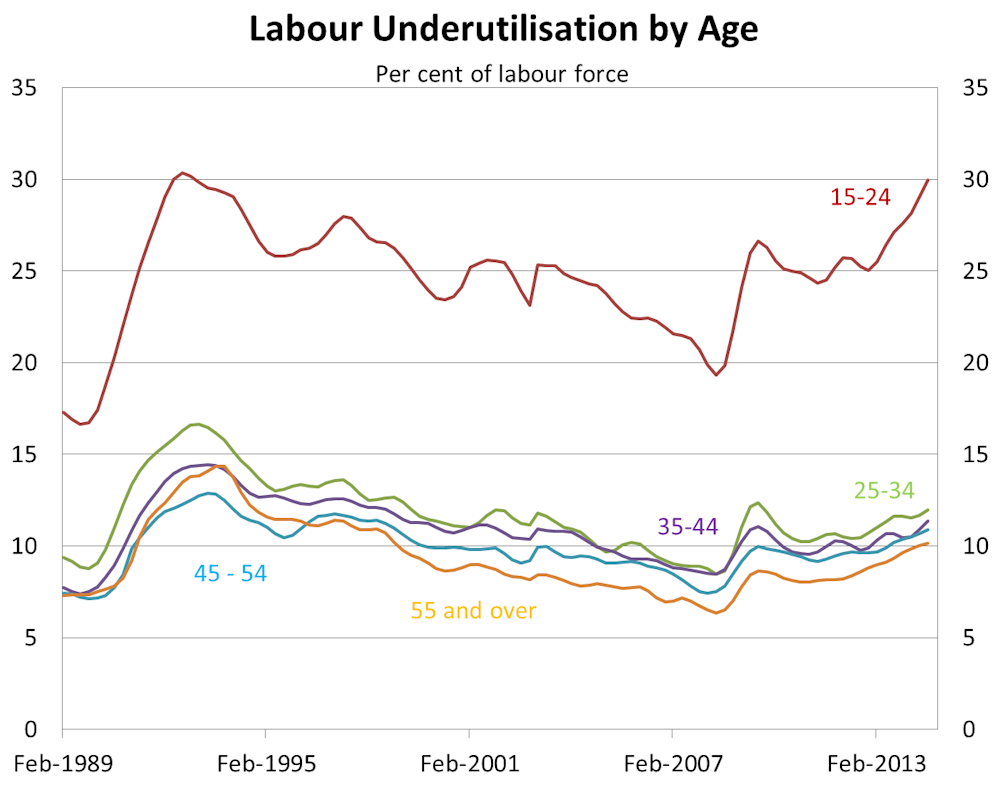

The rise in labour underutilisation has not been uniform across all parts of the labour market. While typically labour underutilisation is much higher for those aged 15-24 compared to those 25 and above, and it increases sharply during either recessions or slowdowns, recently it has risen noticeably.

The unemployment rate and the labour underutilisation measures show slack exists in the labour market, but much less than in the early 1990s. This slack is likely to hold down wages growth.

Private sector wages growth over the year to the June quarter was the lowest rate since the measure preferred by policymakers was introduced in the late 1990s. As wages, together with productivity, are the key factors which influence domestically-based inflationary pressures, these are likely to remain contained in the near term.