The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

The picture of the Australian economy painted by the latest data is murky. The housing market and indicators of sentiment are strengthening but growth remains slightly below trend and the unemployment rate rose to 6.4% in July. Relative to the previous month, the CAMA RBA Shadow Board has become slightly more cautious in its recommendations for interest rates. The Board attaches a 74% probability that the cash rate ought to remain at 2.5% in September. The confidence attached to a required rate cut equals 6%, while the confidence in a required rate hike has dropped to 21%.

Australia’s unemployment rate increased 0.3 percentage points to 6.4% in July 2014, a 12-year high. This rise is largely attributable to an increase in the participation rate — the number of persons in the labour force swelled by 43,000, while total employment fell slightly. Policy makers will be keeping a close eye on the developments in the labour market, in particular whether the additional job seekers are going to succeed in finding employment in the near future.

There is no new inflation data available to guide this month’s policy decision, with headline inflation officially still hugging the top of the 2-3% target band. Business indicators are looking up, with the NAB Business Confidence, the Manufacturing PMI, the Australian PSI, and the capacity utilisation rate all improving in the last month. GDP growth is estimated to lie just below trend.

The construction industry is responding positively to the housing boom, picking up some of the economic slack left behind from the slowdown in mining investment but some Board members remain concerned about inflated asset prices, particularly house prices in Sydney and Melbourne.

Worldwide foreign exchange markets are characterised by exceptionally low volatility. The Australian dollar has moved very little in the past few months, still buying around 93 US cents. There is still some uncertainty about the federal government’s budget and the government’s ability to navigate the Senate remains.

Mixed news also characterises the global economy. The US economy looks more solid, with recent second quarter GDP growth revised up to 4.2% (annualised). The US Federal Reserve’s hints of future tightening of US monetary policy is likely to weaken the Australian dollar and may provide greater scope for a domestic rate increase.

News of the Chinese real estate markets is providing further evidence of considerable excess supply with house prices in some cities, especially at the luxury end, falling sharply. Europe’s recovery is faltering and, most worryingly, there are signs of Germany’s economy slowing significantly. The major geopolitical conflicts (Syria, Ukraine, Middle East) are unlikely to be resolved any time soon.

What the CAMA Shadow Board believes

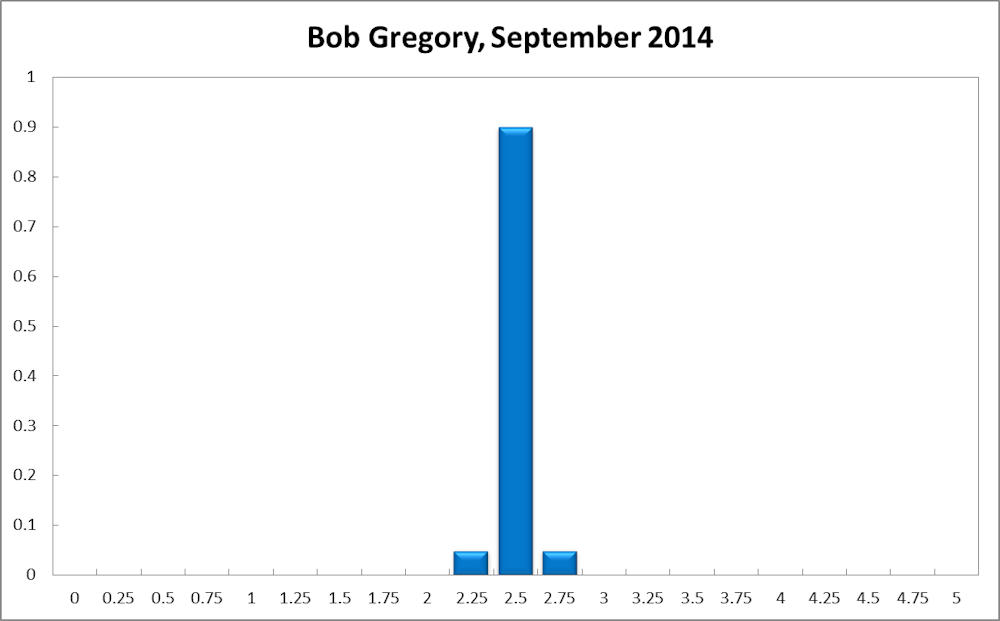

The consensus to keep the cash rate at its current level of 2.5% has strengthened to 74% (up 3 percentage points from August). The probability attached to a required rate cut equals 6% (5% in August) while the probability of a required rate hike has fallen again to 21% (24% in August).

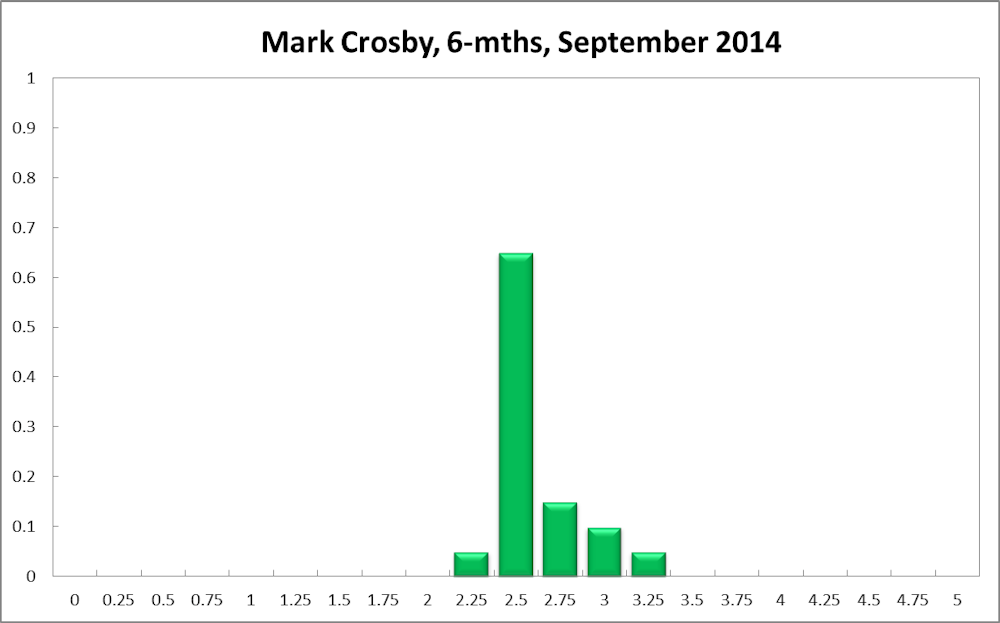

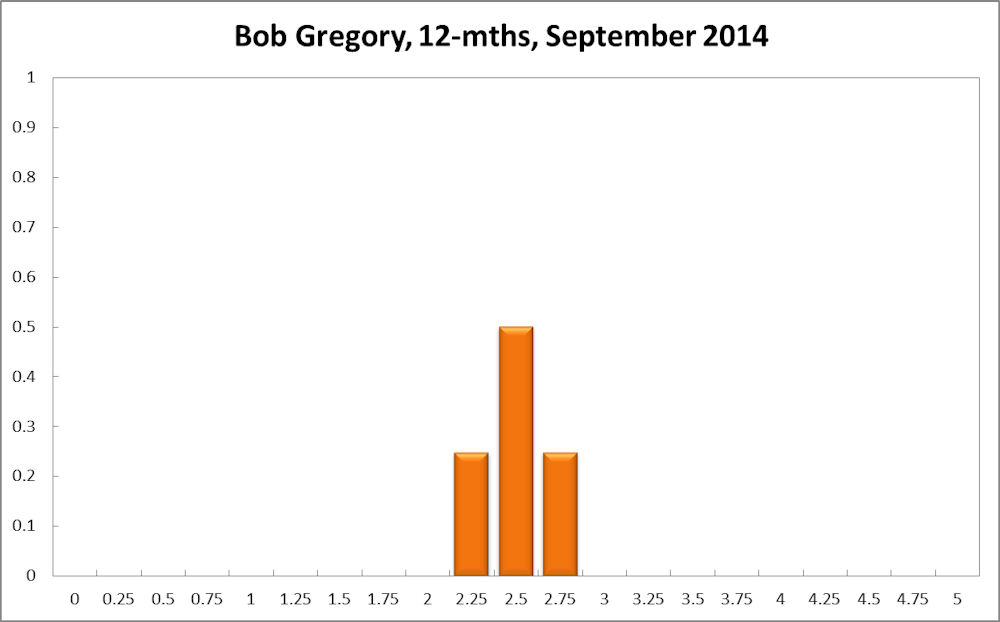

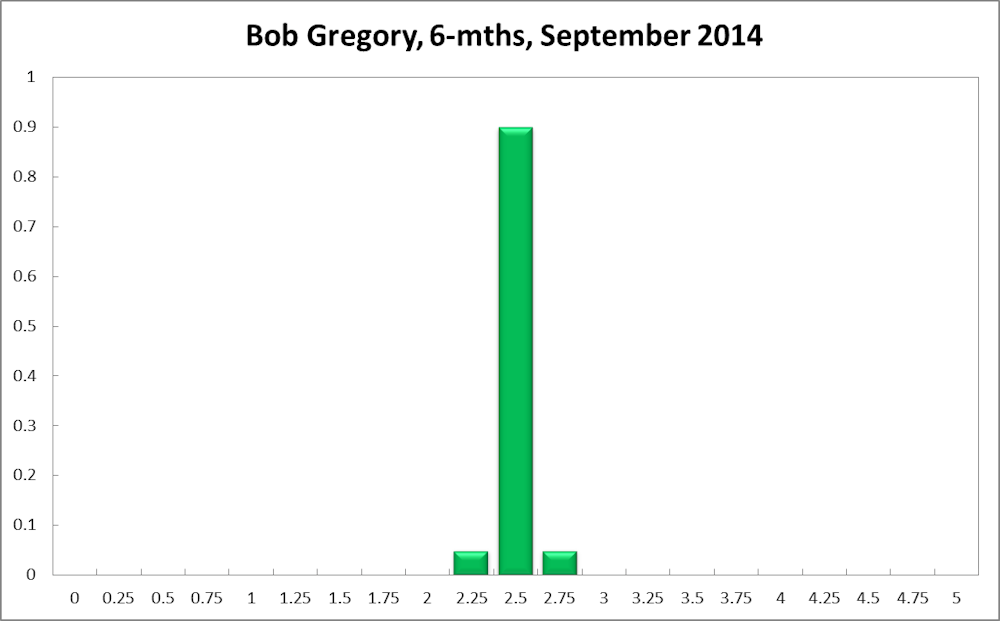

The six month probability that the cash rate should remain at 2.5% edged up two percentage points to 49%. The estimated need for an interest rate increase equals 42% (45% in August), while the need for a decrease equals 9% (8% in August). A year out, the Shadow Board members’ confidence in a required cash rate increase slipped 4 percentage points to 61%, the need for a decrease ticked up to 10%, while the probability for a rate hold strengthened slightly to 29% (26% in August).

Comments from Shadow Reserve bank members

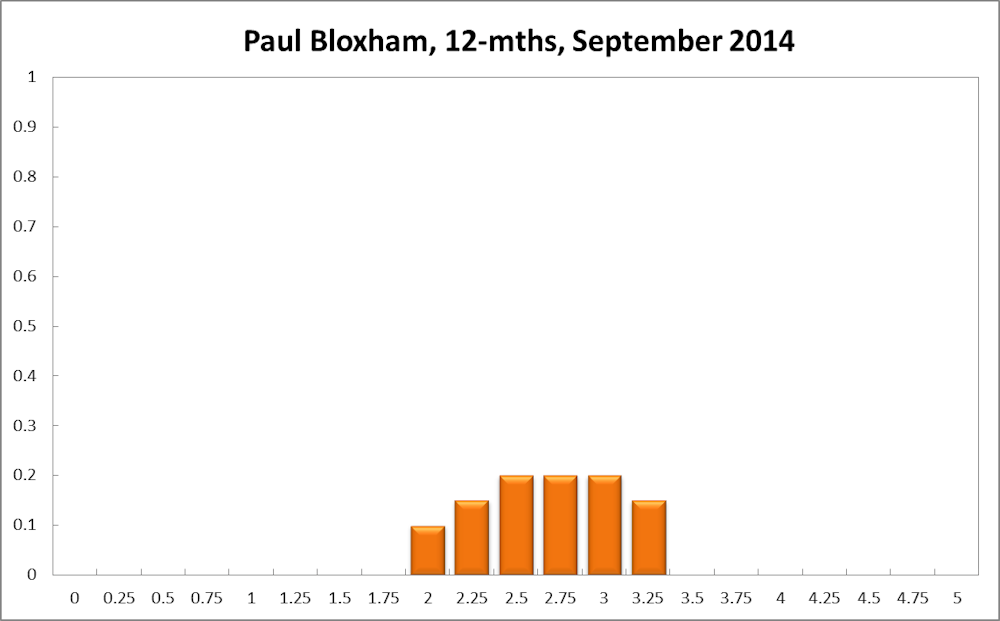

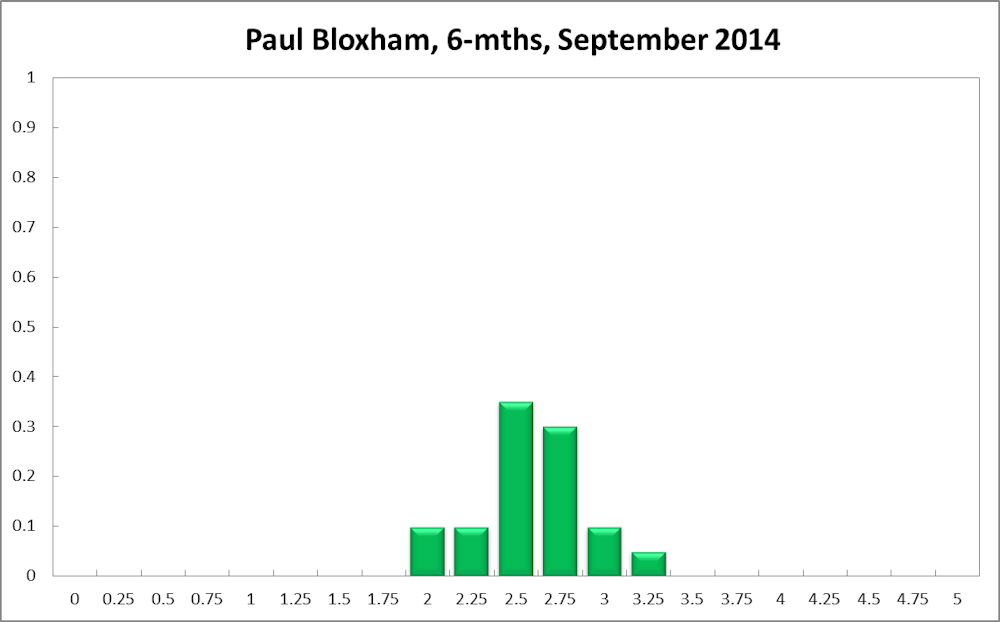

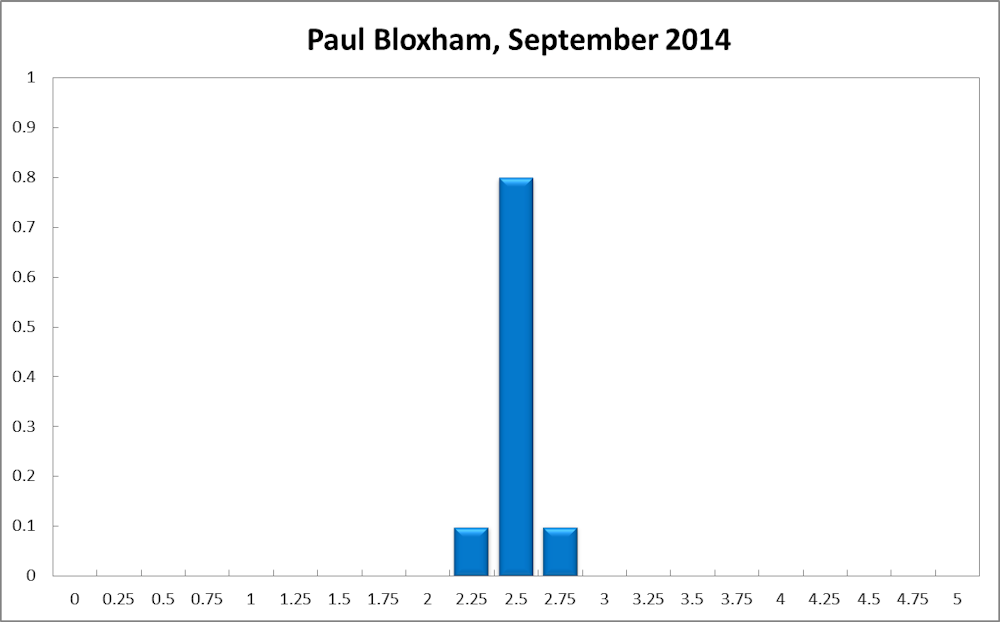

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

“Growth looks to have been below trend.”

Indicators of sentiment have continued to improve over the past month, notwithstanding an uptick in the measured unemployment rate in July. The established housing market has also shown signs of continued exuberance, particularly in Sydney and Melbourne. There have been further signs of a strong upswing in residential construction although, at the same time, mining investment has continued to fall. Overall, growth looks to have been below trend around the middle of the year, although the collection of indicators suggest that domestic conditions appear to have improved in the past month or two.

Given improving momentum in local growth and the booming housing market, the case for a further cash rate cut is weak. A key source of tension for the Australian economy remains the high AUD, particularly in the face of falling iron ore and coal prices and a significant narrowing in the interest rate differential between Australia and the US (the 10-year bond spread is around an 8-year low).

The combination of falling commodity prices and a high AUD is putting downward pressure on local income growth and helps to explain further weakness in the labour market. Australia’s growth prospects could be noticeably improved by a lower AUD, but it remains a significant challenge to orchestrate such as move, with much dependent on international conditions. While a further cut in the cash rate could encourage the AUD to fall, lower rates could also drive excessive risk taking in an already booming housing market and eventually threaten financial stability.

I recommend the cash rate is left unchanged this month. I expect that the cash rate may need to be lifted in the next six-12 months, to prevent a housing bubble from inflating, but the scope to lift rates is somewhat conditional on the direction the Australian dollar takes.

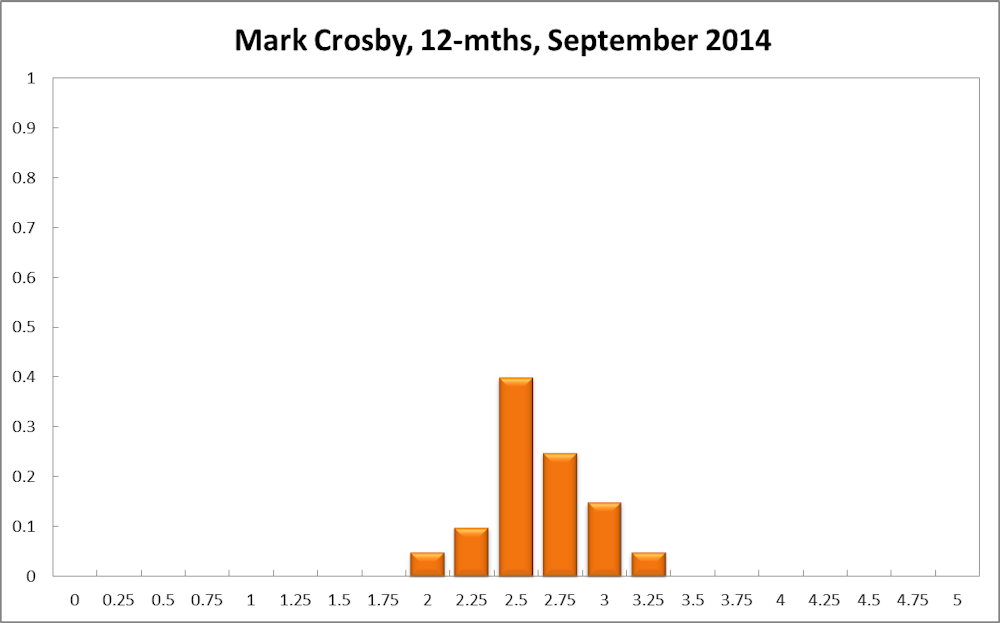

Mark Crosby, Associate Professor, Melbourne Business School:

“Rates may be at the lowest level they will be in our lifetimes.”

With the US continuing on track towards normalisation of monetary policy, the likelihood of the RBA cutting rates is receding. It is quite possible that current rates are at the lowest level they will be in our lifetimes. However, the speed of rate rises is likely to be slow in the next 1-2 years, with weak growth in advanced economies likely to be the norm.

Bob Gregory, Professor of Economics at Australian National University:

“We just have to wait and see for a while.”

This is a very slow time at the moment. We just have to wait and see for a while. Looking forward a year international forces will encourage the Australian rate upwards, but domestic considerations will probably encourage the rate downwards with the likelihood of little change being high.

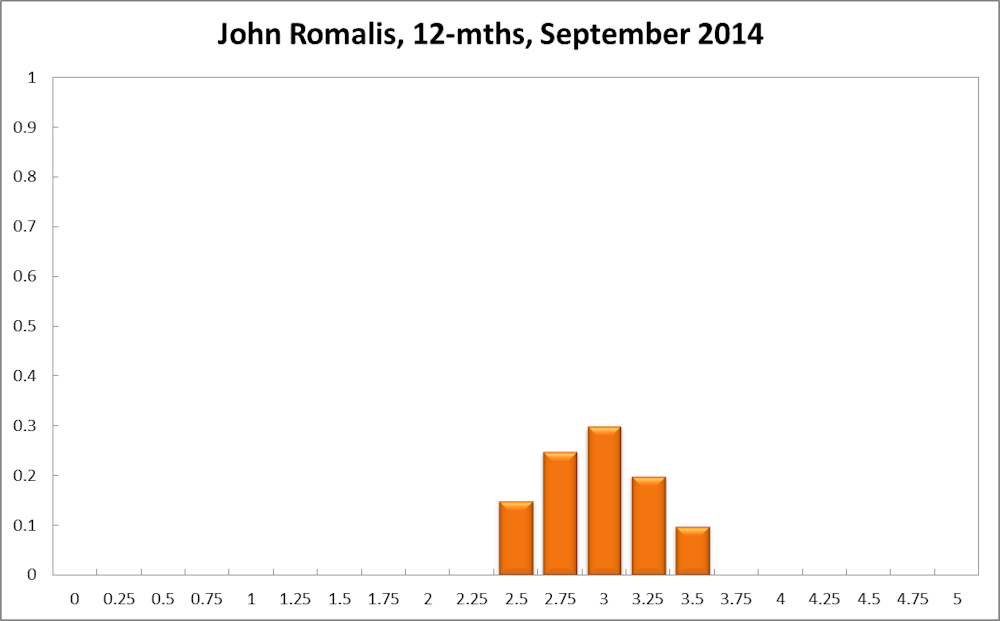

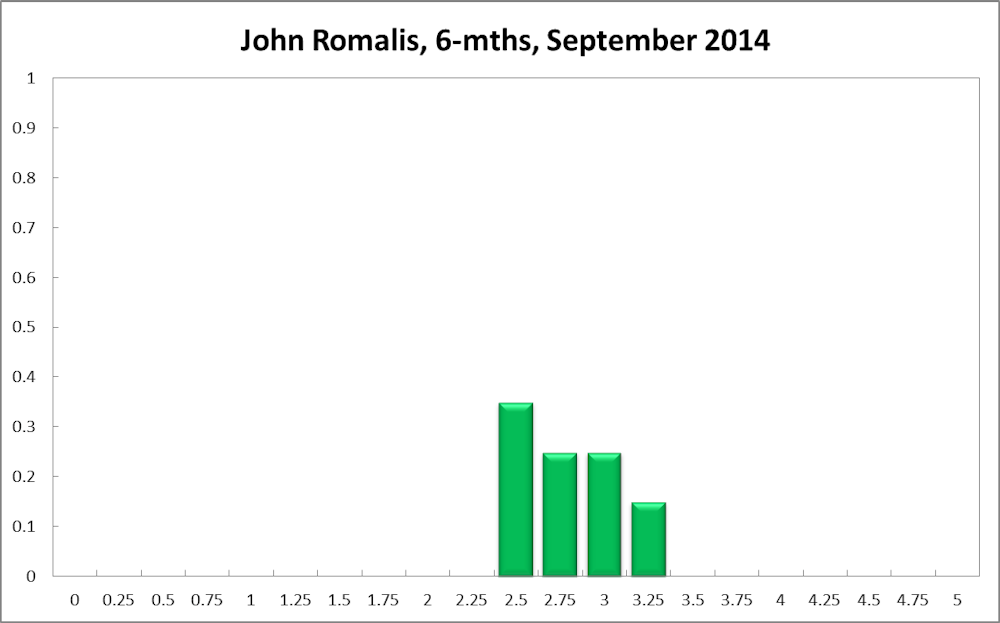

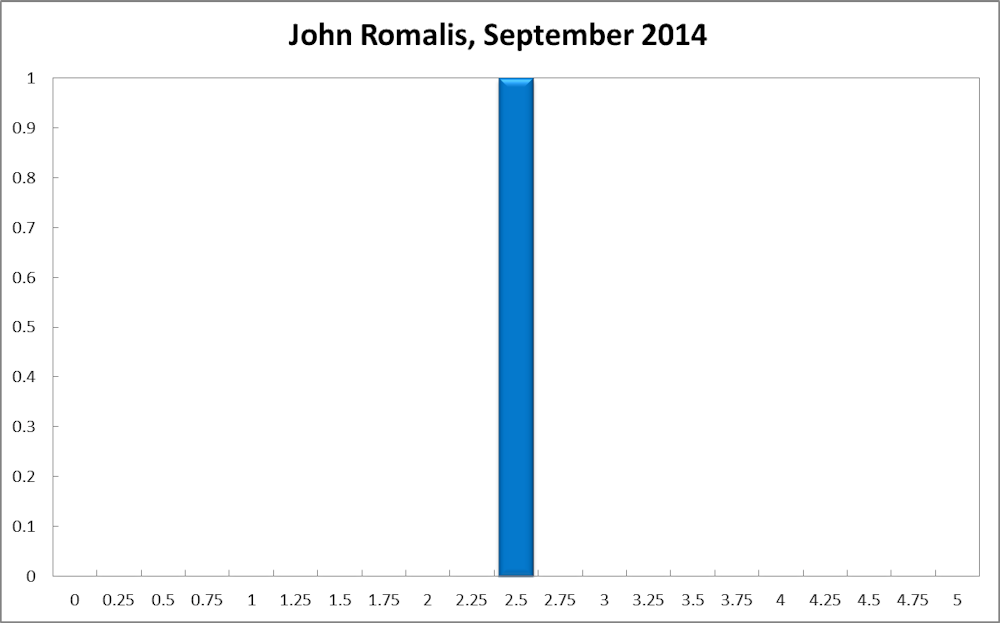

John Romalis, Professor of Economics at the University of Sydney:

“Faster GDP growth from rising commodity exports should be somewhat discounted.”

The Australian economy still seems to be slightly soft, with moderately elevated unemployment levels contributing to low wage growth and moderate inflation rates. Looking forward, rising housing construction should help offset the negative effects of declining mining investment.

Faster GDP growth from rising commodity exports should be somewhat discounted because fewer workers are required to run mines than to build mines and associated infrastructure. Economic and financial conditions in our main trading partners appear to be increasingly robust, which should help restore domestic confidence and keep commodity prices at fairly high levels. So while rates should remain constant for now, there is a greater likelihood that the target cash rate should rise later in the forecast horizon.

Note: John Romalis has replaced Saul Eslake on the CAMA RBA Shadow Board.

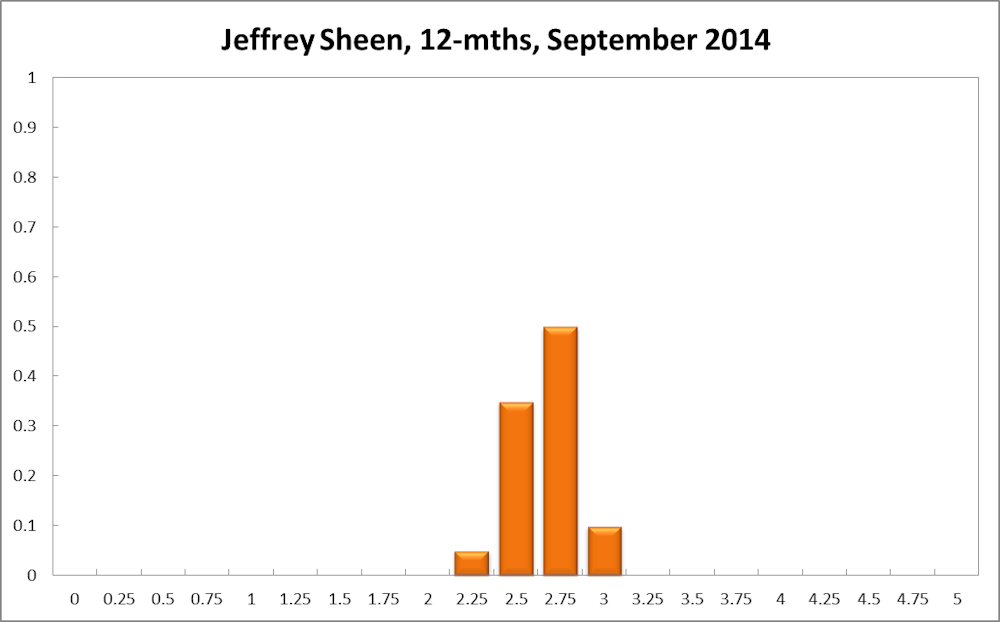

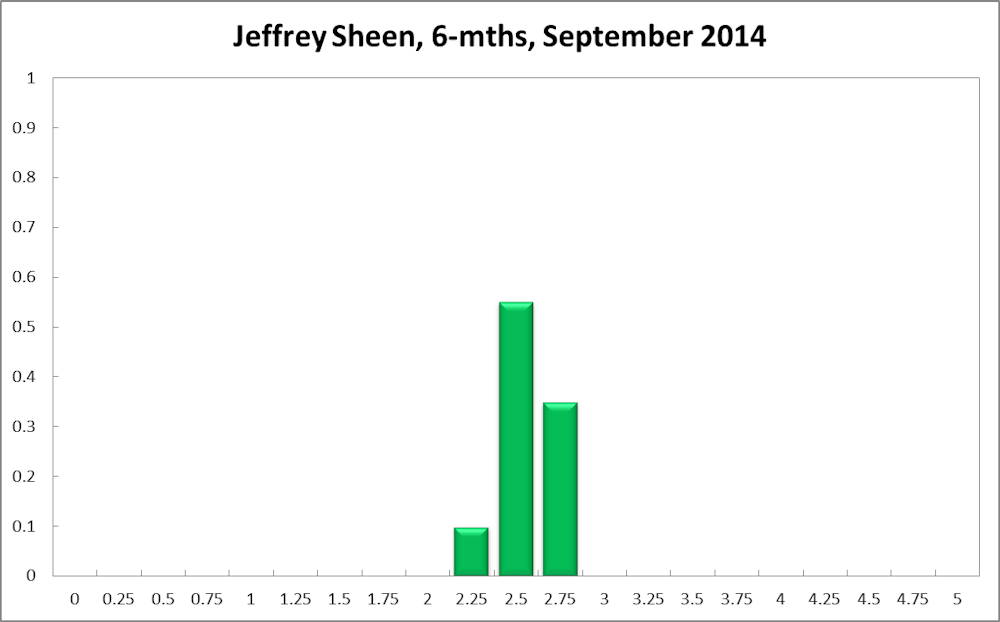

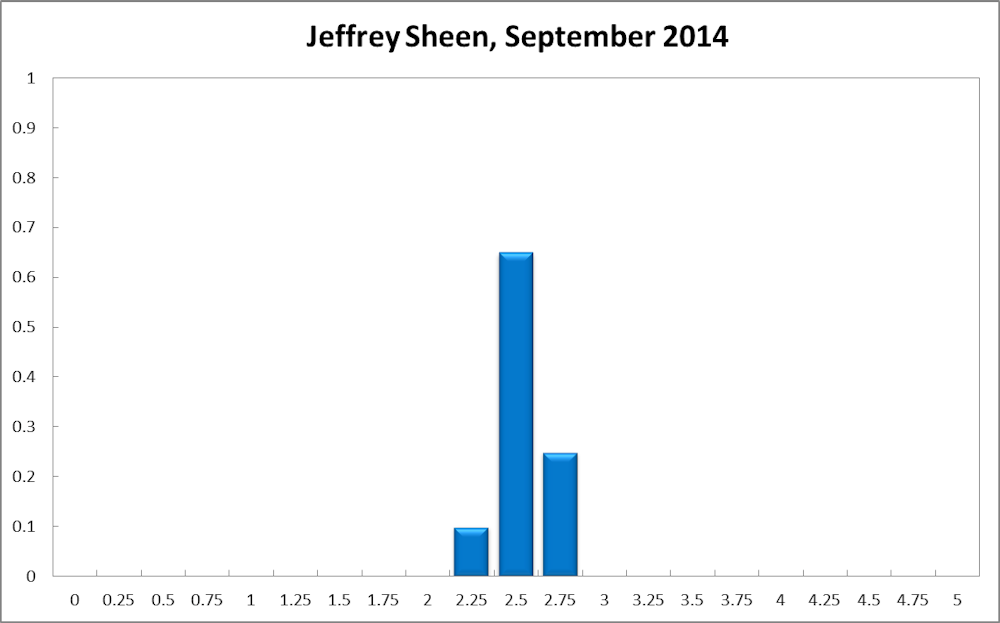

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

The news about the labour market in August suggests that the current accommodative stance of monetary policy needs to continue, along with a marginally higher delay before it needs to begin reversing.

VERDICT FOR SEPTEMBER: cash rate ought to remain at 2.5%.