The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

New inflation and growth data suggest that the RBA’s low interest rate setting ought to come to an end soon. Inflation is close to the upper target band, consumer confidence has bounced back from the temporary drop in May and GDP growth remains solid. Though some weakness in the labour market remains, the majority of Shadow Board members is arguing for an interest rate increase in the foreseeable future.

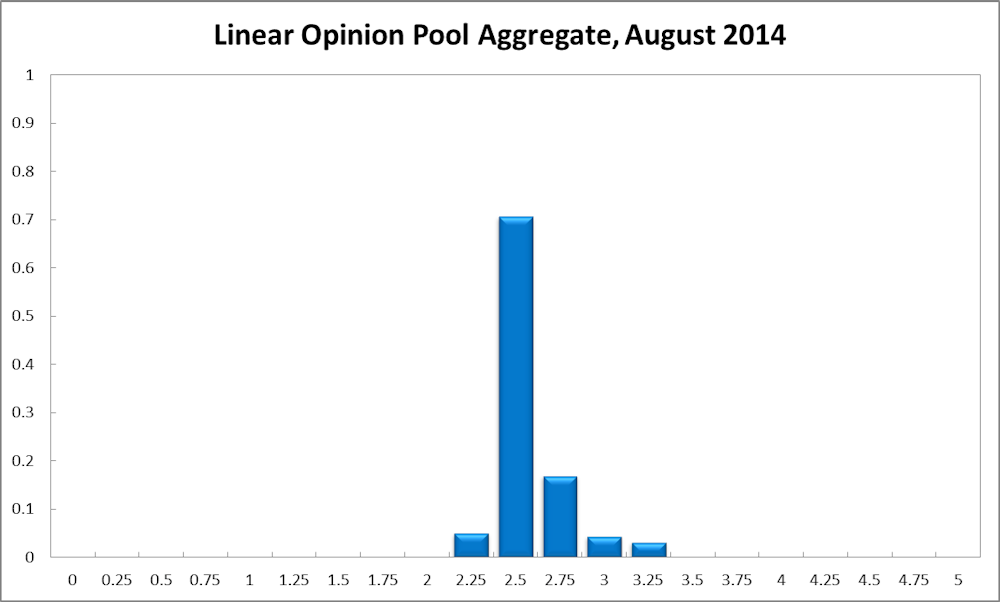

That said, the CAMA RBA Shadow Board’s conviction that the cash rate ought to remain at 2.5% in August remains strong; it attaches a 71% probability that this is the appropriate setting. The confidence attached to a required rate cut has fallen one percentage point to 5%, while the confidence in a required rate hike has risen to 24%.

Headline inflation in Australia rose to 3% (year-on-year) in the second quarter of 2014, hitting the top of the RBA’s inflation target band of 2-3%. Core inflation in the same period has also edged up to 2.81%, suggesting that the increase in prices is broad-based. With domestic growth looking solid and other economic indicators (e.g. consumer confidence, business confidence, inventory stocks, private sector credit) pointing to a continuation of the economic expansion, the case for an increase in the benchmark policy rate is increasing.

Furthermore, among the Board members, concern about inflated asset prices, resulting from low interest rates, is rising. The biggest factor holding interest rates in check appears to be the unemployment rate which currently stands at 6% and is unlikely to improve significantly.

The Australian dollar remains relatively strong, hovering around 93 US cents. Some uncertainty remains about the federal government’s budget, with the Senate unlikely to pass significant sections of the budget announced in May.

The global economy appears to be improving. US second quarter GDP roared back to 4% (annualized), after an unusually weak first quarter. This is supported by a further reduction in the US unemployment rate. The Federal Reserve is continuing with its phase-out of quantitative easing, and financial markets are beginning to price in an interest rate rise in the medium term. China’s economy is steadying; the European economies are still languishing, but not worsening.

Some global risks remain, in particular geopolitical conflicts (such as Syria, Ukraine, and the Israeli/Gaza conflict) but also economic and financial problems including the economic slowdown of BRICS countries and Argentina’s second debt default.

What the CAMA Shadow Board believes

The consensus to keep the cash rate at its current level of 2.5% has fallen 5 percentage points to 71%. The probability attached to a required rate cut is up a percentage point to 5% while the probability of a required rate hike has risen to 24% (20% in July).

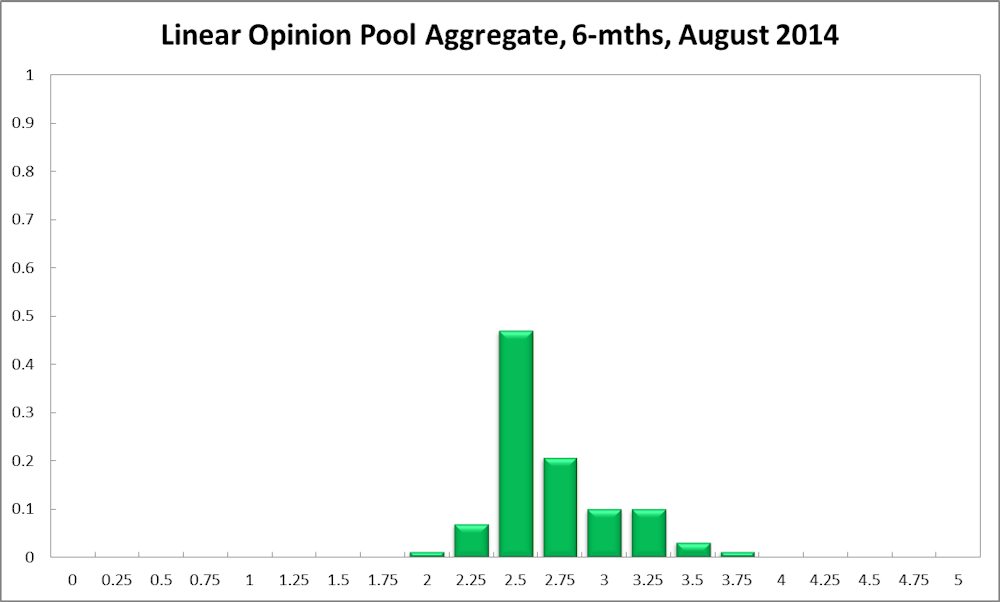

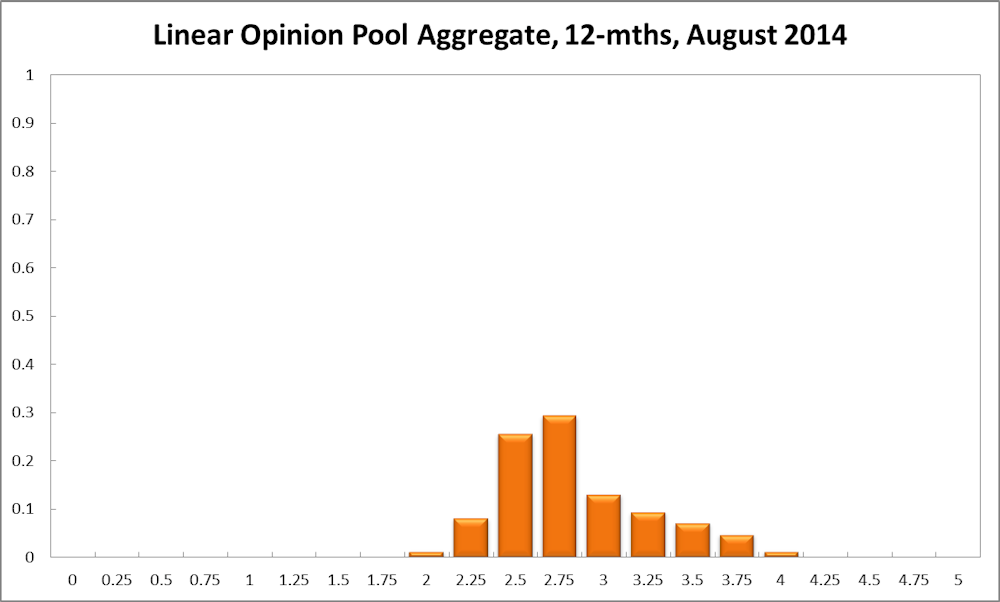

Six months out, the probability that the cash rate should remain at 2.5% is unchanged at 47%. The estimated need for an interest rate increase equals 45% (41% in July), while the need for a decrease equals 8%. A year out, the Shadow Board members’ confidence in a required cash rate increase has risen further to 65% (61% in July), the need for a decrease fell to 9% (11% in July), while the probability for a rate hold slipped two percentage points to 26% (28% in July).

Comments from Shadow Reserve bank members

“Prevent a housing bubble from inflating.”

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Timely indicators of economic conditions have generally improved in the past month. Consumer sentiment has bounced back, after having fallen sharply in response to the May Federal budget. Activity in the housing market has picked up, after having slowed around May. Business sentiment remains positive and a recent lift in business credit growth provides an early sign that corporate sector investment may be starting to lift. China’s growth has also lifted, which is providing some support for iron ore prices in the past month, following significant falls earlier in the year.

The labour market remained broadly steady, with the unemployment rate around the same level as at the beginning of the year. At the same time, the Q2 CPI print showed that underlying inflation remains solidly in the upper half of the 2-3% target band. Very accommodative monetary policy appears to be working and inflation is in the upper half of the target band, which provides little scope or necessity for the board to consider cutting rates further.

Indeed, in my view, the risk that low rates may start to drive excessive risk taking in the housing market is building, which could eventually threaten financial stability. I recommend the cash rate is left unchanged this month, but expect that the cash rate may need to be lifted in the next 6-12 months partly to prevent a housing bubble from inflating.

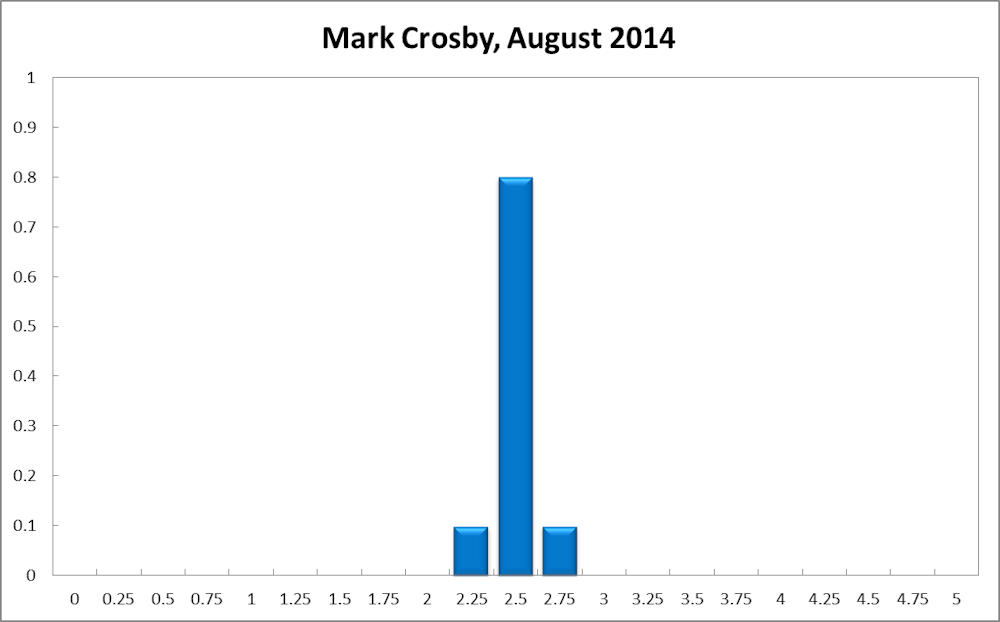

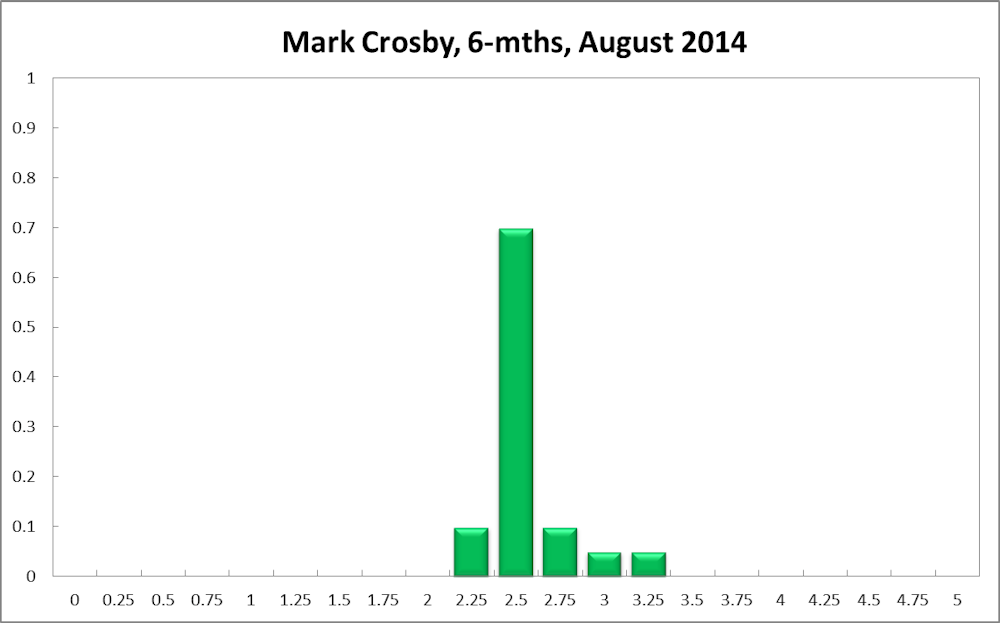

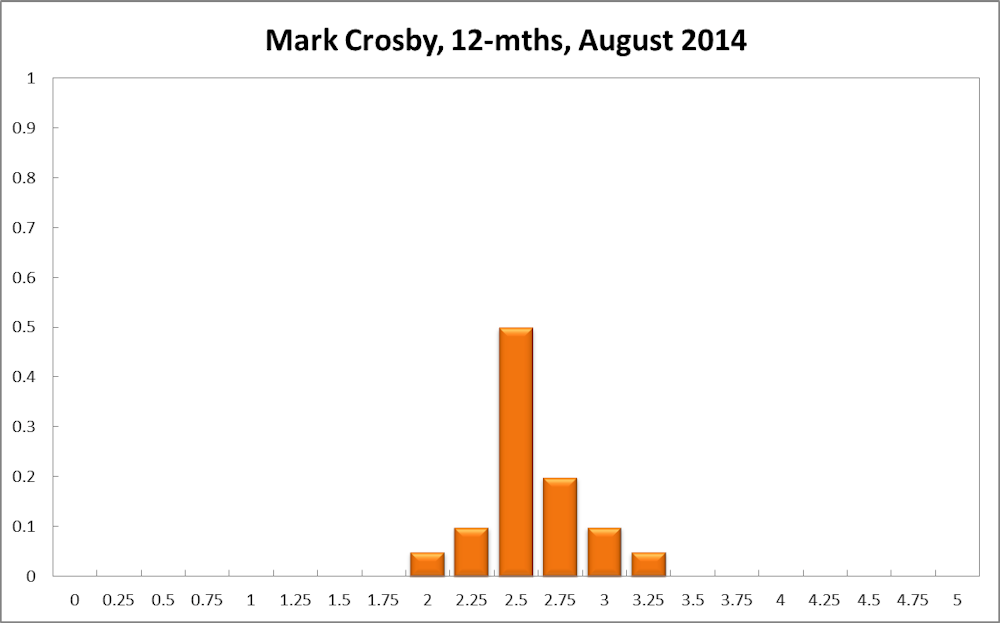

Mark Crosby, Associate Professor, Melbourne Business School:

“Hopes for US and Europe to edge closer to normalising monetary policy.”

There is little in the current environment to suggest anything other than sitting on one’s hands for the moment. In the six to 12 month horizon we can hope that the US and Europe continue to edge closer to normalising monetary policy, freeing up the RBA to also move rates closer to a more usual neutral rate.

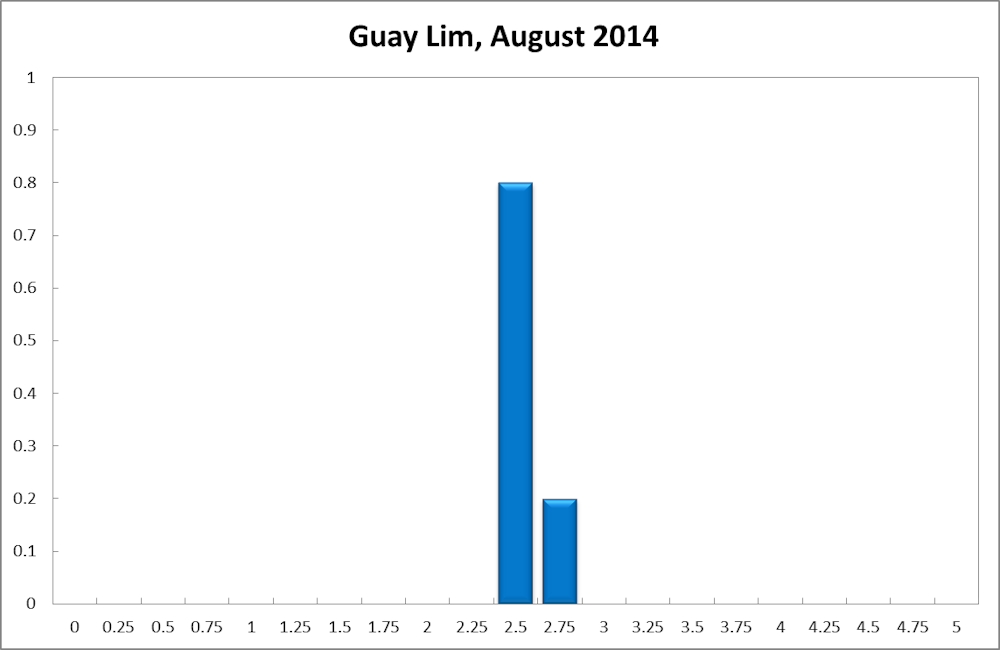

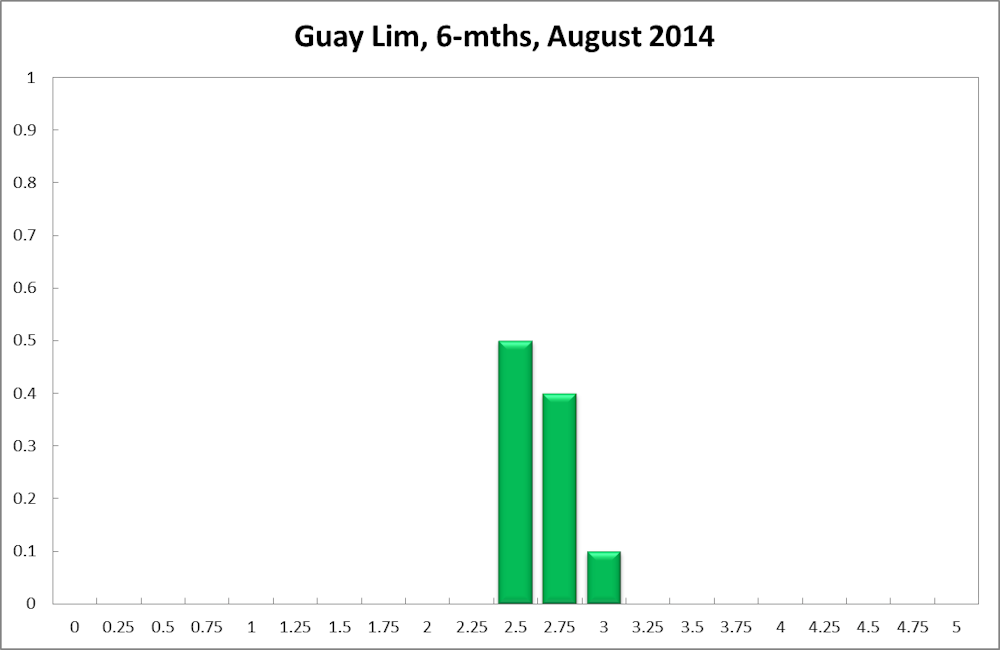

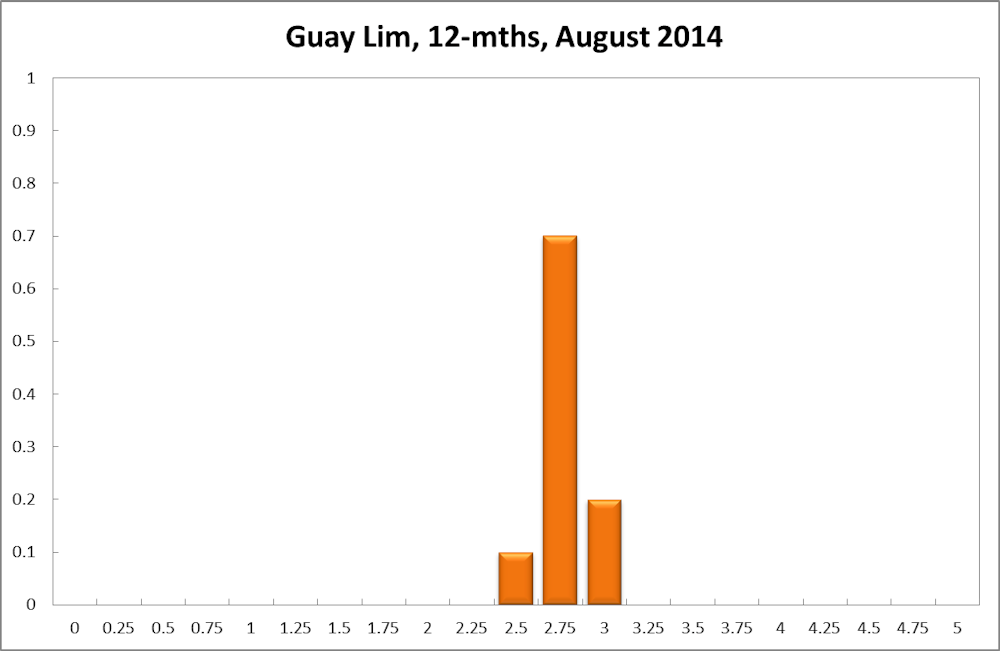

Guay Lim, Professorial Research Fellow and Deputy Director, at the Melbourne Institute of Applied Economic and Social Research, Melbourne University:

“Inflation is edging up, but the case for an immediate hike is not strong.”

The case for tighter monetary policy has strengthened as inflation is edging up along with a pick-up in the growth of credit. However, the case for an immediate hike in the cash rate is not strong as growth in activity and employment remain tentative.

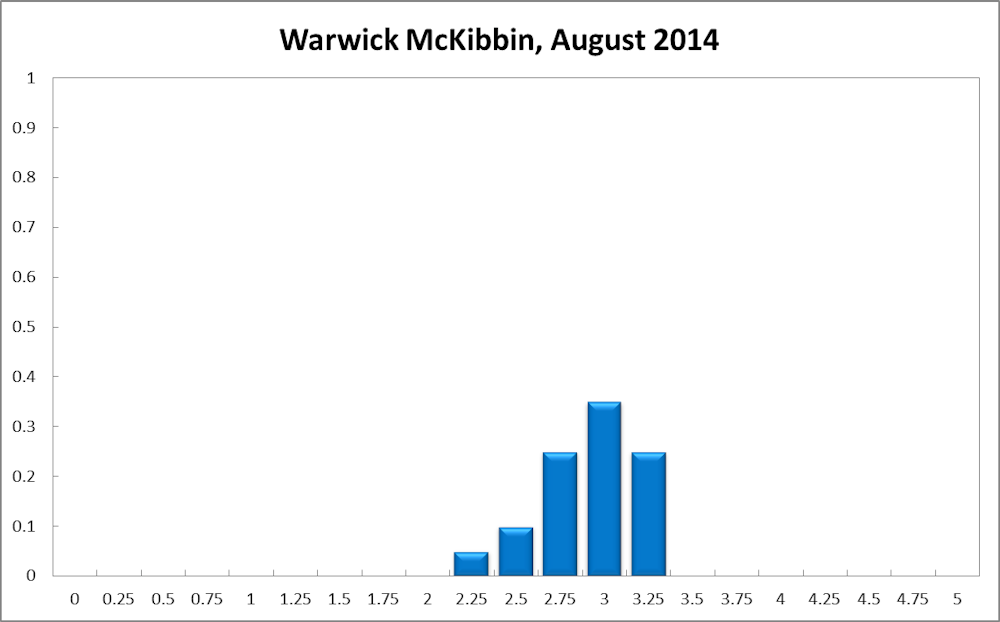

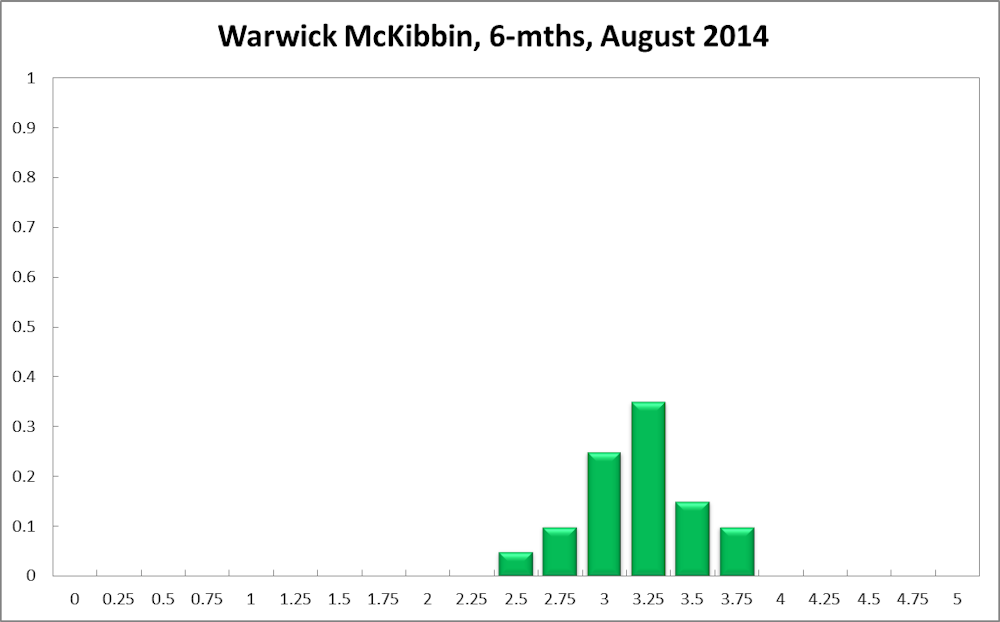

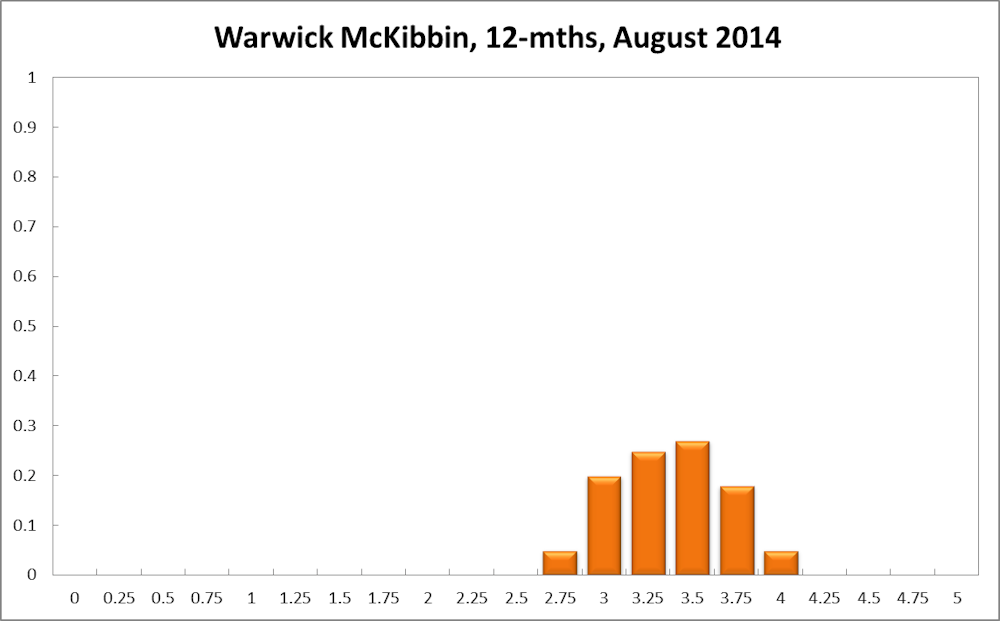

Warwick McKibbin, Professor, Australian National University, CAMA:

“The blocking of policy reform by the Australian Senate is making a bad situation worse.”

With domestic goods price inflation rising to the top of the RBA’s inflation target band and asset price inflation clearly rising to uncomfortable levels the current policy interest rate in Australia is too low. Monetary policy is too expansionary. The dilemma for the RBA is how to get back to a more neutral interest rate given global policy settings. The strong Australian dollar will continue while foreign investors search for yield and the international adjustment of monetary policies continue to drive global currencies. Clearly the policy answer lies outside the domain of monetary policy.

The current problem in Australia is in the settings of fiscal policy and the lack of appropriate structural adjustment policies. In a world of significant geo-political risks and economic uncertainty the blocking of policy reform by the Australian Senate is making a bad situation worse by hurting consumer confidence. There is little that monetary policy can do to negate the near term and more serious long term economic damage caused by the current political standoff.

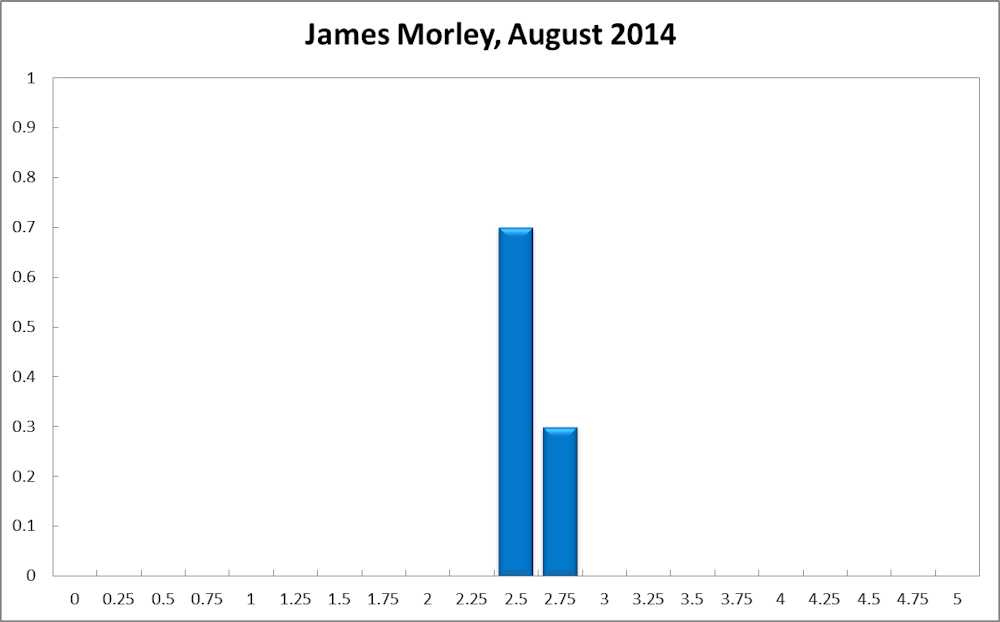

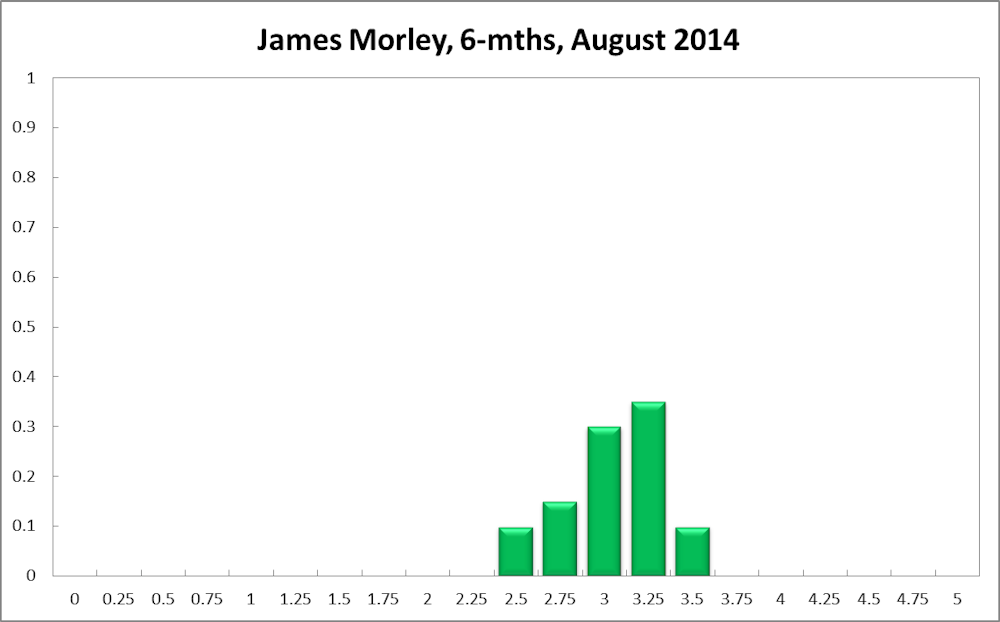

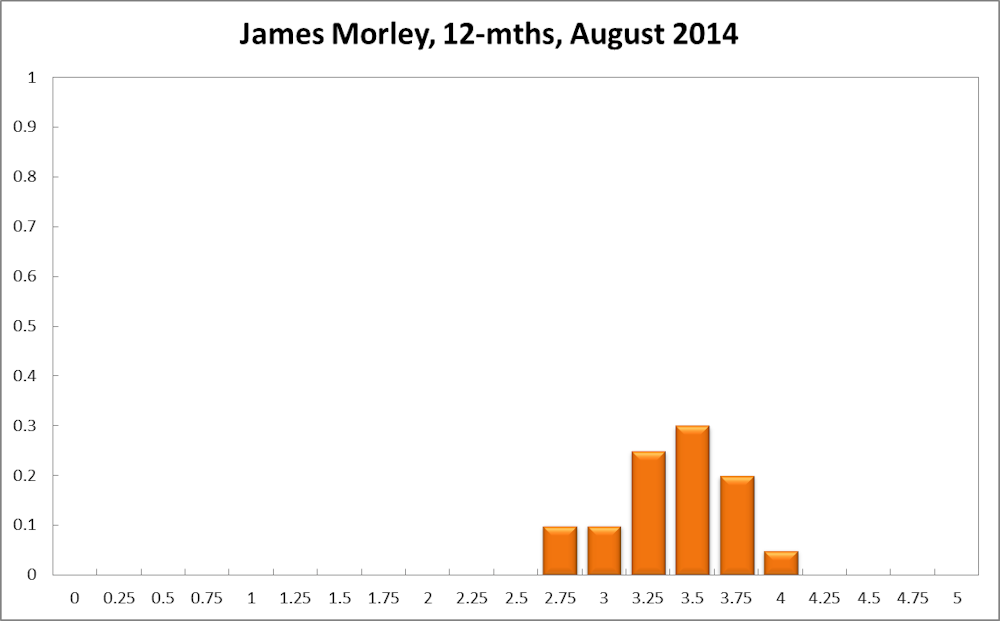

James Morley, Professor, University of New South Wales, CAMA:

“Ongoing weakness in the labour market may see the RBA hold steady.”

Inflation is running at the high end of the RBA’s target range of 2-3%, with year-on-year headline inflation in June of 3.0% and underlying inflation (excluding volatile items) of 2.8%. Given these inflation numbers, the RBA needs to consider raising the policy rate in the medium term. However, unless inflation looks to actually fall outside the target range, ongoing weakness in the labour market suggests that the RBA can hold the policy rate steady in the immediate future.

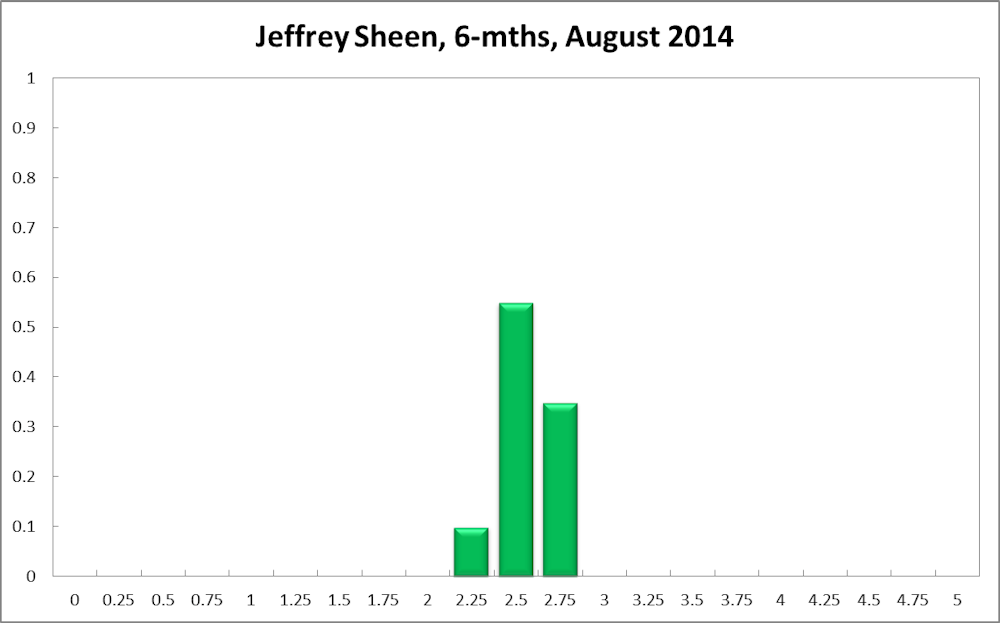

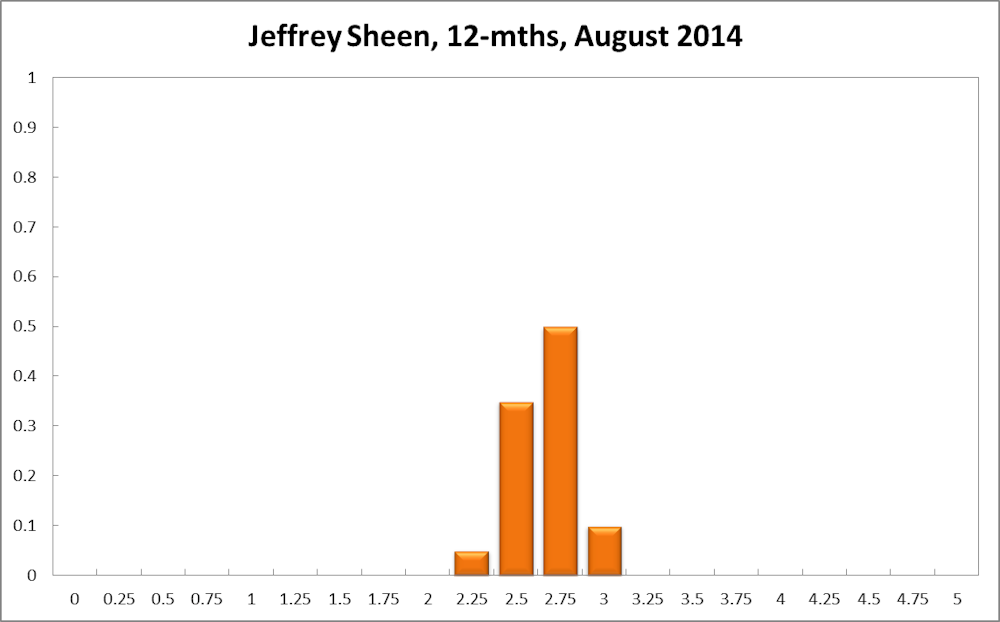

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“The pressure to raise interest rates sometime next year continues to increase.”

The pressure to raise interest rates sometime next year continues to increase given Australia’s inflation rate in the second quarter reached the upper limit of the RBA’s target band of 3%, that hours worked increased 0.9% despite the unemployment rate rising to 6% in June, and that output growth in the first quarter was a little above normal at 3.8%.

This future recommendation is supported by the fact that the US economy growth has recovered significantly in quarter 2 to 4% following its temporary weather-related drop in the previous quarter. However, as a counter-weight, the IMF has lowered its prediction a little for China ‘s growth in 2015.

Click here to view the full charts of all CAMA board members. Saul Eslake has resigned from the CAMA RBA Shadow Board and did not vote in this round.

VERDICT FOR AUGUST: cash rate ought to remain at 2.5%.