Financial markets around the world are responding to current political uncertainty in both Australia and the UK by sending stocks, bonds and currencies on a rollercoaster ride.

The far-reaching implications of Brexit caused the S&P/ASX 200 volatility index (A-VIX) to spike to the highest level since the start of 2016. Similarly, the A-VIX jumped 5% in the opening minutes of trading on Monday after it became clear the federal election would remain unresolved.

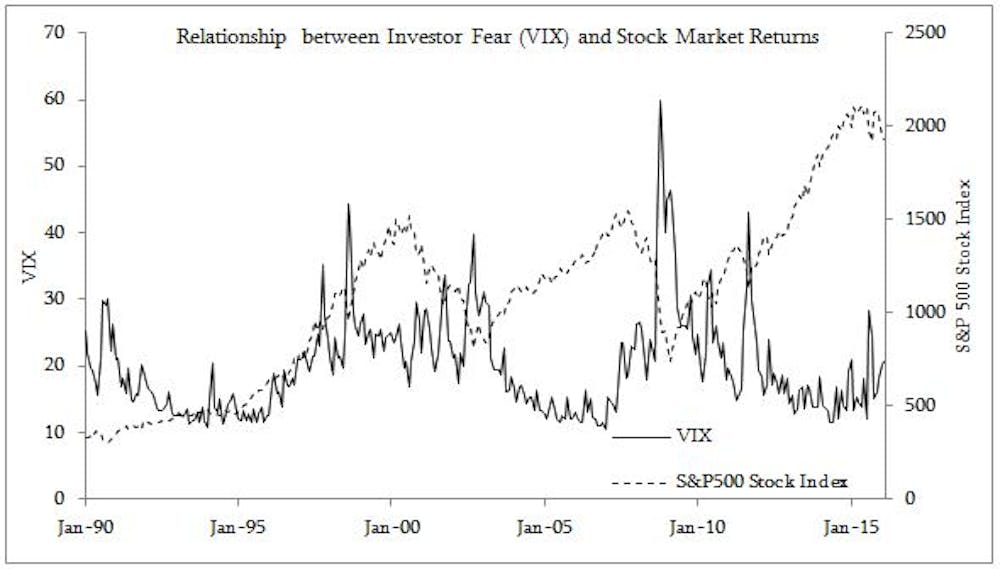

The VIX essentially gives an indication as to the market expectation of price volatility over the next 30 days. Since the main participants in the option market tend to be investors seeking protection against declining prices, the VIX tends to rise when investors are anxious about falling markets – giving rise to the colloquial term of the “fear gauge”.

Why investor sentiment is important

In theory, asset values should be determined by competition among rational investors. Such competition makes for prices that reflect “fundamental” values - basically the discounted value of expected cash flows. But in reality we know this is not always the case. For instance, based on the discounted value of rental income, the Australian housing market is currently far above fundamental value. Essentially, “sentiment” reflects the irrational behaviour that pushes prices away from the underlying fundamentals.

The uninformed traders who exhibit this irrationality are often called “noise” traders, and theory suggests that over time they will lose sufficient capital to be forced out of the market. The trouble is, constraints can mean that even the most informed trader could become insolvent before the market reflects fundamental values. With this in mind, it is important to understand what sentiment is, how we can measure it, and how it might impact asset prices.

The theory on investor sentiment suggests that positive sentiment will drive prices above fundamental value and provide above average returns in one period. In the next period, the misvaluation will be corrected. So periods of positive sentiment are followed by periods of below average returns, and vice-versa. That is the theory, but how can we empirically test it?

A self-fulfilling prophecy

A major issue that we have is that sentiment cannot be directly observed, and so we have to use alternate measures as a proxy. A number of alternatives have been suggested, these are often based on surveys (such as consumer confidence) or market variables (such as trading positions) with varying degrees of success in explaining market movements.

A further complication in researching the effect of sentiment is that it is often difficult to disentangle sentiment from market movements as they are often self-reinforcing. To think of why this may be, consider media reporting of movements in the stock market. If the stock market goes up, then the media writes glowing reports and this entices additional “noise” traders into the market. More shares are bought, pushing prices higher, and producing further positive media commentary. This can often continue until we are in bubble territory.

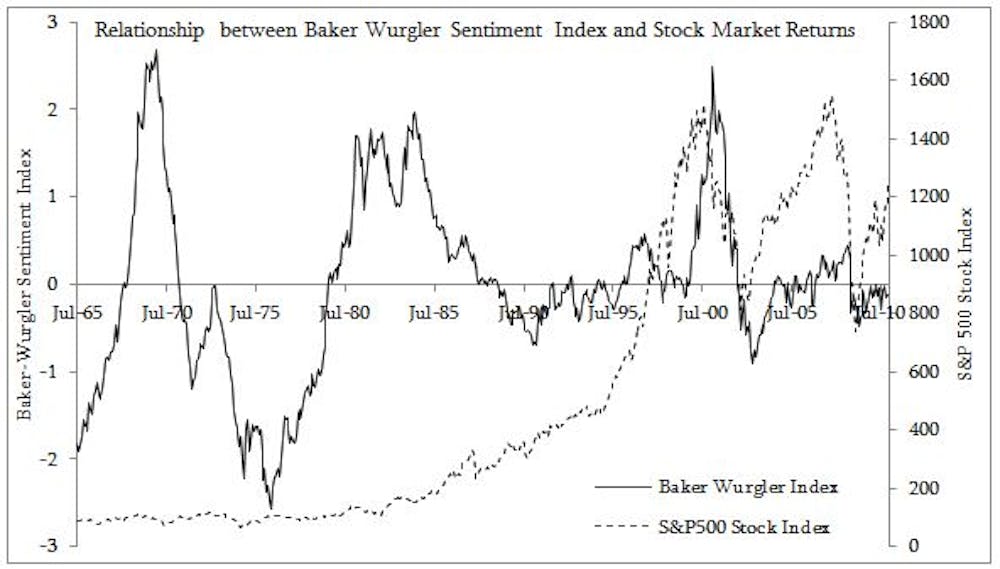

Two important proxies for investor sentiment

Aside from volatility indices like the VIX, there is also a composite index that uses the principal components of six individual proxies related to market activity (this includes share turnover and the number of IPOs).

The researchers that developed this index used it to explain stock returns over a lengthy period running from 1963. They found that investor sentiment had a greater effect on stocks in small, young, and high-growth firms. The index data is available here, but ends in 2010.

What the research says about sentiment and returns

Research has shown that VIX and stock prices have a strong contemporaneous relationship, where VIX increases as stock prices fall. Perhaps more importantly, VIX is also useful in forecasting price movements in future periods.

When investor fear is high, stock prices are pushed below fundamental values. In the next period, when the level of risk aversion reverts to some norm, stock prices move back towards the equilibrium level and generate above average returns. This fits well with the underlying theory of investor sentiment.

Interestingly, investor fear in the stock market is also informative for returns in currency markets and bond markets, suggesting that the effect of sentiment is pervasive across asset classes. And sentiment also effects the way in which markets respond to news events, such as economic data releases, with stronger, more volatile responses tending to occur when investor sentiment is low (alternatively, fear is high).

Political uncertainty can drive sentiment

Right now many investors are unsure about how government policy will impact them directly, via taxation and superannuation reform, and indirectly through the effect of policy (or lack of policy) on business investment decisions.

For many investors, this remains a time to be cautious. However, history has shown that the best returns are often to be found by buying when investor fear is at its highest.