A choice that football coaches have to make after every touchdown – whether to get the relatively easy point or risk it by going for two – offers helpful insights into why Federal Reserve Chair Janet Yellen (the economy’s coach) decided to raise interest rates this week.

In the world of football, the offensive team has two options after scoring a touchdown. The team can either 1) kick a point-after-touchdown (PAT) for a single point or 2) run or pass the ball over the goal line for a two-point conversion.

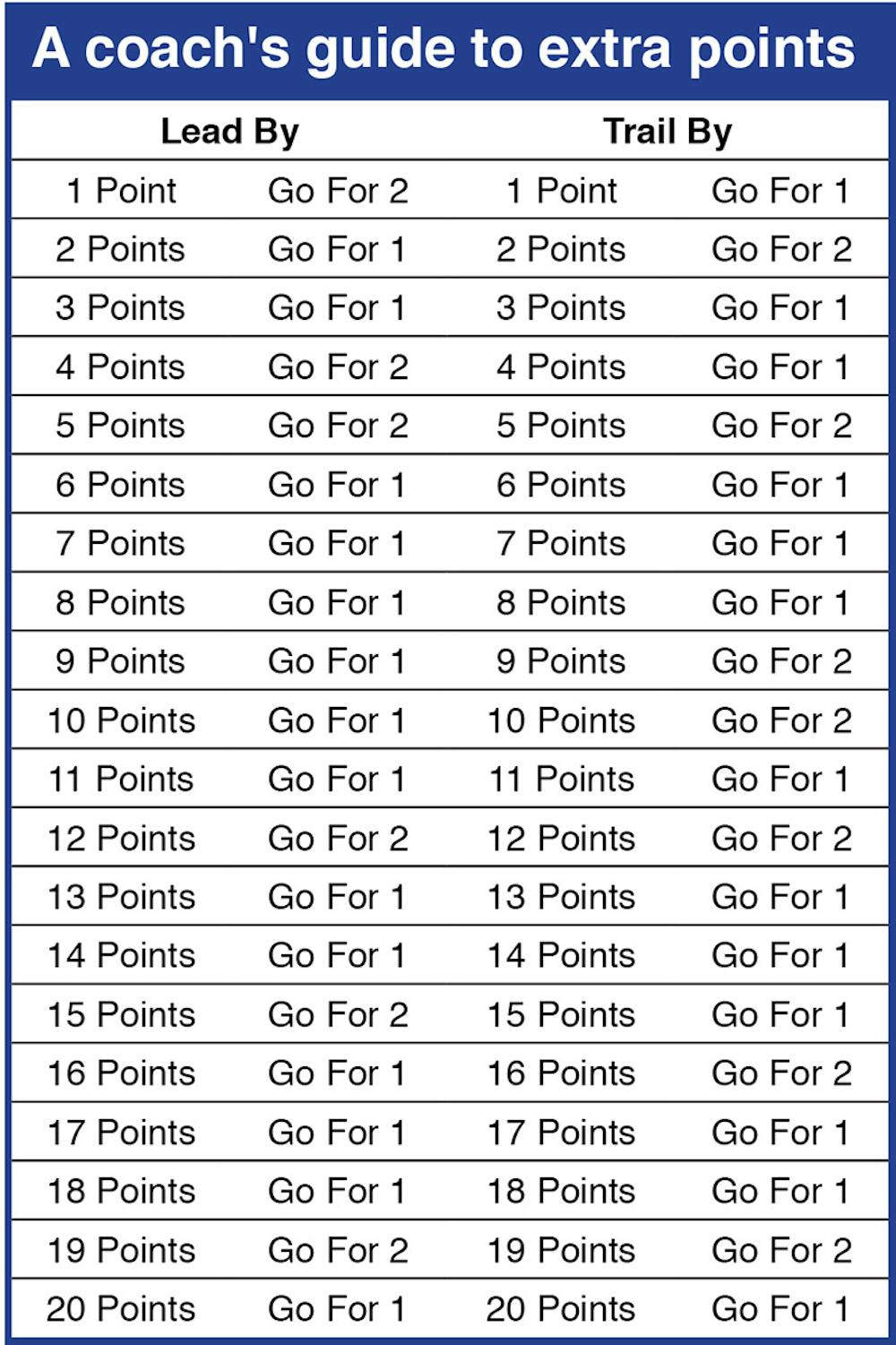

The line of scrimmage for the PAT for the National Football League is now the 15-yard line, while two-point conversions begin from the two-yard line. Based on the score of the game after the touchdown, the chart at right provides a “rule of thumb” for coaches when making this decision.

Of course, a coach is likely to deviate from this chart depending on the feeling of the game, if a kicker is “cold” or “hot,” if the defense is looking shabby, if its windy, raining, sunny, humid, etc. The chart, championed by Dick Vermeil in 1973 (when the PAT was positioned at the 3-yard line), is a standard rule and generally holds true when the two-point conversion has a success rate below 40%.

So why are we talking about the two-point conversion? I spoke to numerous radio and television stations within hours of the Fed’s announcement about interest rates on December 16. During the interviews, most of my hosts asked me about the 2% inflation target of the Fed. And, within hours of the decision, there were a number of articles written about how the Fed’s move to lift rates was wrong or mistimed, also mentioning the central bank’s 2% inflation target, as if the inflation target was set in stone and the only metric that matters.

These discussion are missing, to some extent, the context for the 2% “target” and what it really means.

Let me explain.

The Taylor Rule

The 2% target analysts are throwing around has to do with the Taylor Rule, named after Stanford economist John Taylor and presented in an 1992 article examining the policy of the Fed.

Within this paper, Taylor examined the trend of the Fed’s policies and derived a “rule” that maps out the policy the Fed generally follows in regards to targeting the Federal funds rate, which is the benchmark the central bank lifted about a quarter point this week. The rule for setting the interest rate, r, if you’ll forgive the wonky-looking math, is as such:

r = inflation + (0.5 x (% real GDP deviation From potential GDP)) + (0.5 x (inflation – 2)) + 2

So, for example, suppose that the economy is experiencing 2% inflation and the GDP is exactly where it is expected to be (there is no deviation from potential, or how much economists thing GDP should be). The rule would suggest the following:

r = 2 + (0.5 x (0)) + (0.5 x (2-2)) + 2 = 4

Thus, under such conditions, interest rates (specifically the Fed funds rate) should be targeted at 4%. Suppose GDP was 1% below its potential, and inflation was at 0.5% annually. The rule would suggest:

r = 0.5 + (0.5 x (-1)) + (0.5 x (0.5-2)) + 2 = 1.25

That is, the Fed should target a rate of 1.25%. But, if the economy was really deep in trouble and GDP was 3% below potential and was experiencing deflation of 1%, the math would be this:

r = -1 + (0.5 x (-3)) + (0.5 x (-1-2)) + 2 = -2

In this last example, the target would be at -2%. Of course, the Fed can’t target a negative nominal interest rate (you can’t pay banks to borrow your money!), the interest rate has to be set to zero. When the Fed sees a situation such as this (as in the last recession), the Fed is forced to engage in unorthodox policies, such as quantitative easing, in order to keep liquidity high.

Applying the 2% ‘rule’

So if the Fed were to strictly adhere to the Taylor Rule, what would rates have looked like over the past few decades?

Using data from the Federal Reserve Bank of St Louis, I show the actual Fed funds rate as well as the rate predicted by the Taylor Rule.

According to the Taylor rule, the Fed did lower its target at just about the right time during the housing recession in 2008 but was bound by a zero interest rate (the Taylor rule suggests a negative interest rate during that period). However, the Taylor rule suggests that the Fed should have increased the target rate to 1% by the middle of 2010.

This implies that the Fed was late to the party (by more than five years) in its rate hike this week. Specifically, the Taylor Rule implies the Fed should be currently targeting a rate of about 1%, based on inflation of 1.5% to 1.8% and GDP underperformance of about 2.5% to 3%. That contrasts with the new Fed funds range of 0.25% to 0.5%.

Fed flexibility

Of course, there is a fair amount of discussion between policymakers regarding how the rule plays out in practice and whether this rule is too narrow in focus.

And, there is also a debate regarding whether the rule should have an interest rate target closer to 1%, or if the “weights” in front of the GDP and inflation terms should be a full 1% rather than 0.5%. In all, there is plenty of competing ideas surrounding the exact rule and how (or whether) the Fed should actually follow the rule or use it more as a guide.

I would argue this as well – the Fed has to follow its gut as much as an actual rule when the economy is lacking momentum and traction (as it was during the recovery.)

Taylor himself explicitly states in his paper the following: “the policy rule is not a simple price rule.” That is, the policy is not just about inflation (or deviation from GDP) and shouldn’t be seen as so prescriptive or exclusionary. In fact, Taylor writes about how the Fed can and does transition into new rules based on new economic conditions, and that the central bank most probably learns by doing and, as such, adopts new rules to guide its rate-setting policies.

This, I suggest, is what the Fed is doing and has been doing for some time – the severity of the Great Recession and the measures it took to combat the crisis (including buying trillions of dollars in bonds through policies like quantitative easing) required new rules to guide its decisions.

Time for a change?

And this takes us back to football and the coach’s post-touchdown dilemma.

I referenced the two-point conversion in the introduction. Last year the NFL moved the PAT to the 15 yard-line (from the two-yard line), making the point-after-touchdown kick harder and thus less than automatic. As such, changing circumstances calls for a new approach – more teams are “going for two” than even a year ago.

Do changing economic circumstances call for a different approach to monetary policy? Should the Fed move away from the Taylor Rule and conduct monetary policy based on other criteria and other metrics, such as the labor force participation rate or the type of unemployment?

Again, I would argue that this is exactly what we have seen and what we are seeing. It is not useful to keep beating the 2%-inflation-target drum when evaluating the policies of the current Federal Reserve.

The economy is changing, it’s time for us to start evaluating the Fed’s actions through a new lens.