Australia is allegedly in the midst of a “green building revolution”, powered by the awarding of ratings to developers who build sustainable buildings.

But this brave new world is only a reality in the high-end office blocks of Australia’s central business districts (CBDs). Everywhere else, the pace of progress is much slower. At least, that is what my research into more than 70 sustainability tools, both in Australia and overseas, tells me. Let me explain this through one example.

In 2002, the Green Building Council of Australia (GBCA) was established to “drive the adoption of green building practices through market-based solutions”.

This week it is hosting the Green Cities Conference, bringing together the construction industry, policy makers and academics to discuss the way forward in improving the environmental and resource sustainability of buildings and cities in Australia and elsewhere.

The GBCA is particularly proud of its Green Star system, which rates the environmental performance of buildings.

A Green Star revolution in Australia?

The ratings help the construction industry to showcase the environmental credentials of its buildings. In this respect, Green Star is a simple and elegant idea: it allows a building’s environmental performance (in terms of energy, water and material use) to be easily compared with that of other buildings – rather like the energy performance stickers you find on new fridges or cars.

This easy comparability makes these assessment tools very attractive. For developers, investors, owners and occupants alike, it is easy to grasp that a six-star building is somehow better than a four-star one.

The numbers the GBCA presents about its Green Star program are impressive. More than 7 million square metres of Australia’s built-up space is rated as having high levels of environmental performance. This includes 18% of all office space in the CBDs of major cities. But what do these numbers actually mean, and are these successes found everywhere, or are they concentrated in certain locations?

Central focus

Green Star is mainly used to label office space in the CBDs of Australia’s cities (those with populations of at least 20,000). Here it has indeed achieved considerable success.

Since the introduction of Green Star in 2003, some 5.3 million square metres of office space was added to the CBDs of Australia’s major cities. Of this, about 2.9 million square metres are now Green Star labelled. That is a success rate of about 50%, which may be considered a very successful outcome.

But what is labelled, exactly?

Green Star awards three levels of labels: “Best Practice” (4 stars), “Australian Excellence” (5 stars), and “World Leadership” (6 stars). Green Star does not report on how many buildings or square metres fit into each category, but some other labelling tools may give some insight. The partly mandatory National Australian Built Environment Rating System awards its highest labelling category to just 8% of buildings. Meanwhile, Green Star’s counterpart in the United States, LEED (Leadership in Energy and Environmental Design), only awards 6% of its labels in its highest category.

If the vast majority of buildings are not hitting the highest sustainability standards, then are we really witnessing a revolution?

A levelling-out of growth

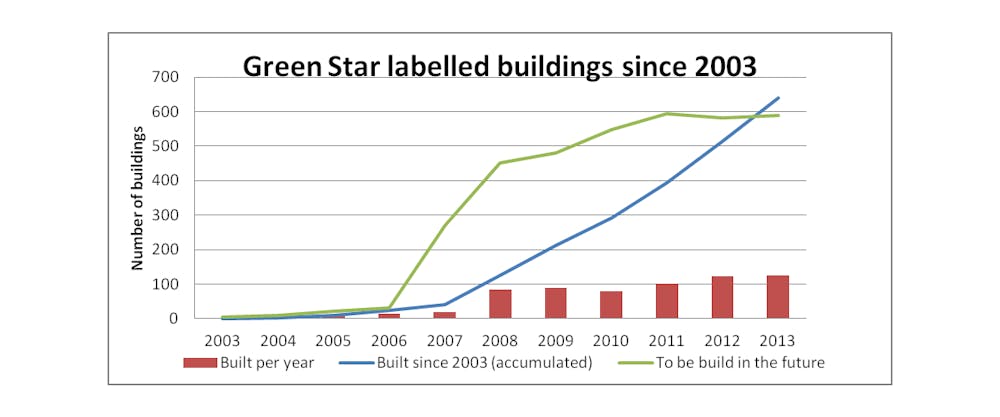

It should also be kept in mind that these are accumulated numbers. If they are unpacked as yearly “successes”, the picture presented by the GBCA changes a little more. The below figure gives some insight.

Since 2008, the uptake of Green Star labelling has levelled out. Before then, it was increasingly sought by developers for buildings they would develop in the future, but this no longer seems to be happening.

This is not that surprising. With the introduction of a tool such as Green Star it is to be expected that many early adopters try it out in the first years when they can be pioneers, and be rewarded as such. It is much harder to get the later adopters on board.

If 18% of the office market represents the Green Star system’s saturation point, then this does not bode well for the revolution’s future. On the current trend we can expect the levelling-out of actually built Green Star buildings to begin in 2016.

This will leave more than 80% of the Australian office market untouched by well over a decade of “Green Star revolution”.

Outside the office

Australia, of course, has more than just office buildings. The total residential building stock is estimated at about 1.5 billion square metres, based on 9 million dwellings at an average for new builds of around 220 square metres (historical averages were lower, which brings down the total). This dwarfs the total commercial space, which is about 27 million square metres.

In this context, Green Star’s impact has been marginal at best. The 7 million square metres of Green Star labelled space represents less than 0.5% of the total.

In other words, outside Australia’s major business districts, green building labelling has not caught on, despite the GBCA’s attempts to move into these markets. The much-touted revolution has not spilled over from the CBDs to the rest of the country.

What makes a revolution?

Green Star is but one of the many tools that I have studied through which the construction industry seeks to foster more sustainable practice. This is a revolution in itself. Like Green Star, these tools have achieved some successes in niche markets, but have not achieved overall sweeping results.

Also like Green Star, these tools have received both accolades and criticisms. The 7 million square metres of labelled office space undoubtedly represents a success for Green Star. But has it caused the revolution in the Australian construction industry that the GBCA claims?

It depends, of course, on your definition of “revolution”. In 2007 Apple introduced the iPhone, which clearly revolutionised communication. More than half of all Australians now own a smartphone. In 2003, the GBCA introduced Green Star, which now covers 0.5% of Australia’s built environment. Clearly some revolutions happen faster than others.

To really kickstart the green building revolution in Australia, other market segments need their own tools like Green Star. This will require more leadership in the industry, in figuring out how to tempt the developers and owners of other building types to join in.

I hope that the Green Cities Conference inspires its participants to move the green building revolution beyond Australia’s CBDs, and past the commercially attractive top end of the construction market.