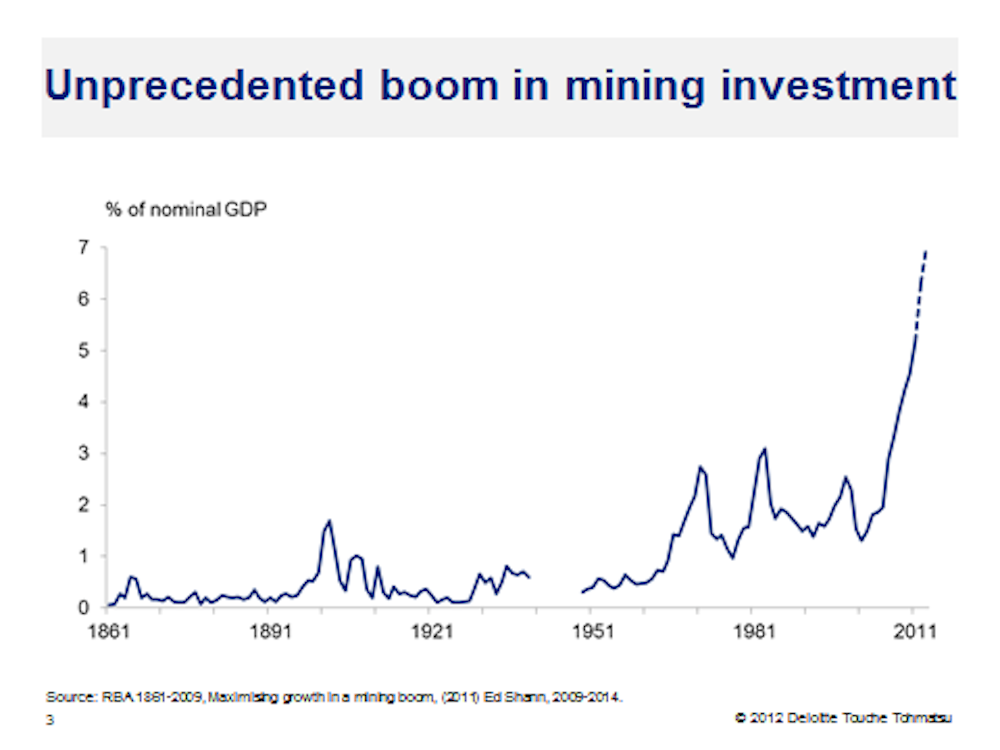

A simple line graph of the share of mining investment in Australia’s GDP reveals the scale of what our economy is going through.

It shows that mining investment is now twice as large relative to GDP as it has ever been, and is forecast to reach at least three times its previous peak in the early 1980s over the next five years.

It is impossible to avoid investment on this scale distorting the overall pattern of economic activity. We have a raging case of “Dutch Disease” or more accurately a “booming sector problem” of unprecedented proportions.

Run-away growth in one sector would create tension enough without the added dimension of geographic dispersion. Essentially the boom in mining activity is occurring north-west of a line drawn from Brisbane to Adelaide. Coincidentally (perhaps not?) this also marks off an area where a minority of Australians live and work.

At best, mining and mining-related activities account for around 20% of aggregate economic activity in Australia. The remaining 80% employs the lion’s share of Australian workers in industries and occupations located overwhelmingly in the south-east of the continent.

Yet the 20% of national economic activity driven by mining and its related industries is growing faster than the Chinese economy—around 8.5% per annum on current estimates — while the remainder is growing at 2% per annum or less.

The economy at large is growing at its trend rate of around 3.25% per annum (or perhaps a bit faster given last week’s national accounts figures) yet the sectoral and geographic composition of this growth is disparate and increasingly so.

In aggregate terms, the Australian economy is in rude health. Not only is aggregate economic growth at trend but unemployment is essentially at its full employment or “natural” level of 5% of the labour force, and average CPI inflation is tracking around the mid-point of the Reserve Bank’s target range of 2-3% per annum.

No wonder Treasurer Wayne Swan and Reserve Bank Governor Glenn Stevens puzzle over the downbeat commentary they read in newspapers and the downcast faces they encounter among members of the public.

How can such stellar economic performance elicit only scowls and grumbles of discontent? Why do foreigners marvel at the rise and rise of the Lucky Country while its denizens cower in fear of imminent economic disaster?

The answer lies in the scale of the economic transformation and its unique conjunction of sectoral and geographic dispersion. Most Australians have little direct or even indirect experience of the growth being generated by the mining boom. It seems remote and, indeed, touches comparatively few people in their everyday lives.

On the contrary, for most Australians, living in the south-east and working in non-mining-related industries, the talk at work is of lay-offs, redundancies and closures. Shop windows advertise a seemingly endless stream of “pre-season”, “mid-season” and “end of season” sales with massive discounts to listed prices. And this is before the nightly dose of fear-mongering on the European financial crisis and the all-too-evident woes of the stock market are added to the mix.

It’s hard to keep your head when all about you are losing theirs - but neither are people’s fears completely groundless. The rapid growth of mining and its related industries drags resources from other less-productive parts of the economy, and attracts foreign investors whose purchases bid up the value of the Australian dollar.

Both of these forces sift the non-mining sectors of the economy to isolate those whose productivity can justify retaining their place in the economic firmament.

Businesses and even whole industries that fail this test will yield up their capital and labour to the expanding sector. While reallocating the economy’s resources is not without pain, neither is it without gain.

Indeed, the whole transformation raises Australian living standards, as did the resource reallocation that followed the tariff reform, privatisation and deregulation of the 1980s.

The Australian economy is being transformed by the historic emergence of China and India, and to a lesser extent Russia and Brazil, from the global economic background to the foreground. This process will not be short-lived and so there is little point in mothballing our industrial structure until the wave passes.

But there is a clear need to explain the process to those who find it hard to see the wood for the trees. Paul Keating captured the 1980s transformation in a brilliant riposte about the risk of Australia becoming a “banana republic”. We need another catch-phrase to focus our minds on the opportunities before us rather than the threats.