China’s exceptional economic growth performance in the last three decades has coincided with equally remarkable demographic change. There is now plenty of evidence to suggest the potential demographic “dividend” associated with a country’s transition towards slower fertility and population growth, and therefore a growing share of the population engaged in – rather than depending on – the workforce, can be quite substantial.

In China’s case, according to some estimates, this demographic dividend can explain as much as one quarter of its economic growth since the 1980s. As the world’s fastest growing economy, this has amounted to a substantial gift indeed.

Not all gifts are given freely, however. The demographic transition to slower population growth has been profoundly affected by China’s family planning policies, culminating in the one-child policy. Fertility rates would have been expected to follow declines seen in China’s Asian neighbours as the effects of urbanisation, female education, increases in labour force participation rates, improved life-expectancy of new-born children, and a myriad of other socio-economic factors become apparent.

Yet this should not detract from cost of the loss of freedom to choose the size of one’s own family, a choice that most of us take for granted and one that is impossible to place a value on.

A further cost of China’s rapid demographic transition is the onset of population ageing at a relatively low level of per capita income, giving rise to the uniquely Chinese phenomenon of “getting old before getting rich” (wei fu xian lao未富先老).

With a per capita income of just over $5,000 in 2010, 8% of China’s population was aged 65 or older, a percentage that will increase to 12% in 2020 and 23% in 2040. So just how serious is China’s pending demographic doom?

A few numerical comparisons can help to illustrate why this question is difficult to answer. The percentage of China’s population aged over 65 in 2040 is projected by the United Nations to be almost identical to that of Australia’s in 2010. So China has thirty more years to get rich before getting as old as Australia is now.

Would you rather face that challenge or that of Japan, nearly ten times wealthier than China in per capita terms, but with two decades of snail-paced economic growth behind it and close to 40% of its population already older than 65? Or would you prefer the wealth-age structure of India, with just $1400 per capita income and 6% of its population aged 65+ in 2010, a percentage that will increase to 12% by 2040, some two decades after China’s does? Placed in this context, China’s demographic change seems to be less of a “time bomb” than some have suggested.

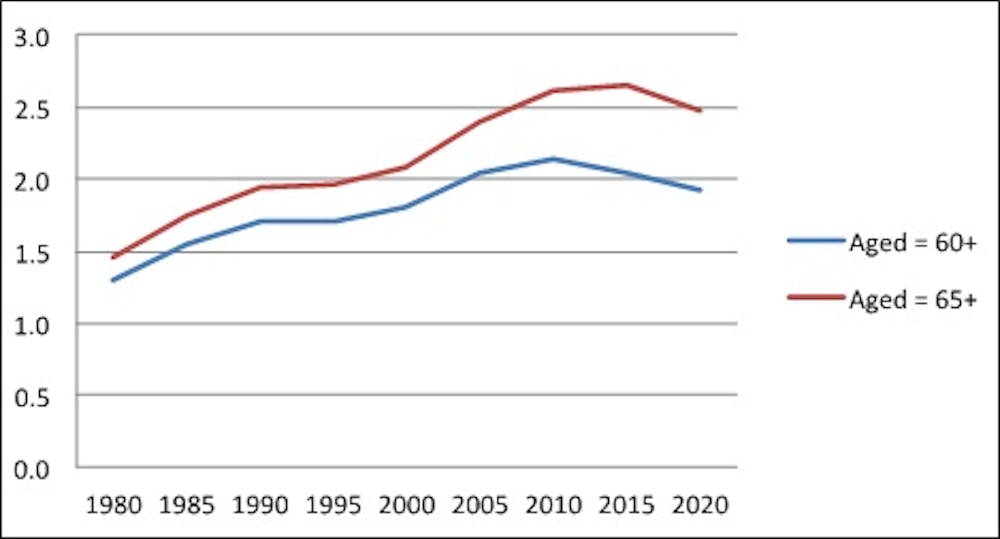

Consider also that the percentage of “old” people in China, as elsewhere, depends on the definition of “old”. As shown in the figure above, if anyone aged 60 or older is classified as “old”, then China’s working-age population as a share of its total population peaked in 2010 (at 2.1 workers for every non-worker, young and old combined).

If you have to be 65 to be “old” then this peak doesn’t happen until 2015 (at which point there will still be 2.7 workers for every non-worker). Changes in the retirement age (currently at 60 years for Chinese men, 55 years for women) therefore provide just one example of how easy it would be to alter the economic impact of ageing, although by an amount that would depend on whether older employees remained willing and able to work, and on whether their younger employers remained willing and able to employ them.

Improvements in the “quality” of the workforce – in terms of education, skills and productivity – would also reduce the negative impact of ageing on the country’s economic performance. Whether ageing itself brings with it continuous improvements in “quality” is a question that young and old will continue to debate for some time to come, and one of many that will affect the pace of change in this realm.

In a recent journal article, Professor Rod Tyers and I examined a range of factors that will impact on the duration and magnitude of China’s and India’s demographic dividends through to 2030. This research shows how changes in fertility and labour force participation rates could extend China’s demographic dividend by at least another decade, thereby reducing the negative impact of population ageing.

This suggests that the policy choices of the new Chinese leadership will be critical in determining just how gloomy China’s demographic future is, which in turn injects more uncertainty into the mix. There are rumours in Beijing that a further relaxation of the one-child policy is just around the corner, for example, but whether this materialises remains to be seen.

Further uncertainty surrounds the use of Chinese official numbers for doing any kind of future projections. Following the release of the Sixth National Population Census in 2010, ANU demographer Zhongwei Zhao did some careful calculations to show that China’s actual fertility rate is around 1.45, compared with an official rate (which is used by the United Nations in its population projections) that has barely moved from 1.8 for the last 20 years.

As Zhao notes, “Differences of nearly 20% in estimated fertility levels and of [over] 100 million people in projected population size are by no means negligible.” If actual fertility rates are as low as Zhao and many others now believe, China’s population is in fact ageing more rapidly than the official figures suggest.

So how serious is China’s pending demographic change? Seriously, it is really hard to say.