No need to beat about the bush. There is another tech bubble in the United States. The relationship between the share prices and profits of US tech companies like Facebook, Twitter and LinkedIn is at unsustainable levels and something has to give.

These companies use a business model based heavily on advertising revenue, either user numbers or price per ad will have to grow many times over to justify current stock prices. Neither outcome seems likely. User growth has plateaued and advertisers aren’t willing to pay much at all for online advertising space. Over the coming two years a huge correction in stock prices will have to take place, likely triggered by an end to low interest rates that have inflated this bubble with cheap money.

Eye watering

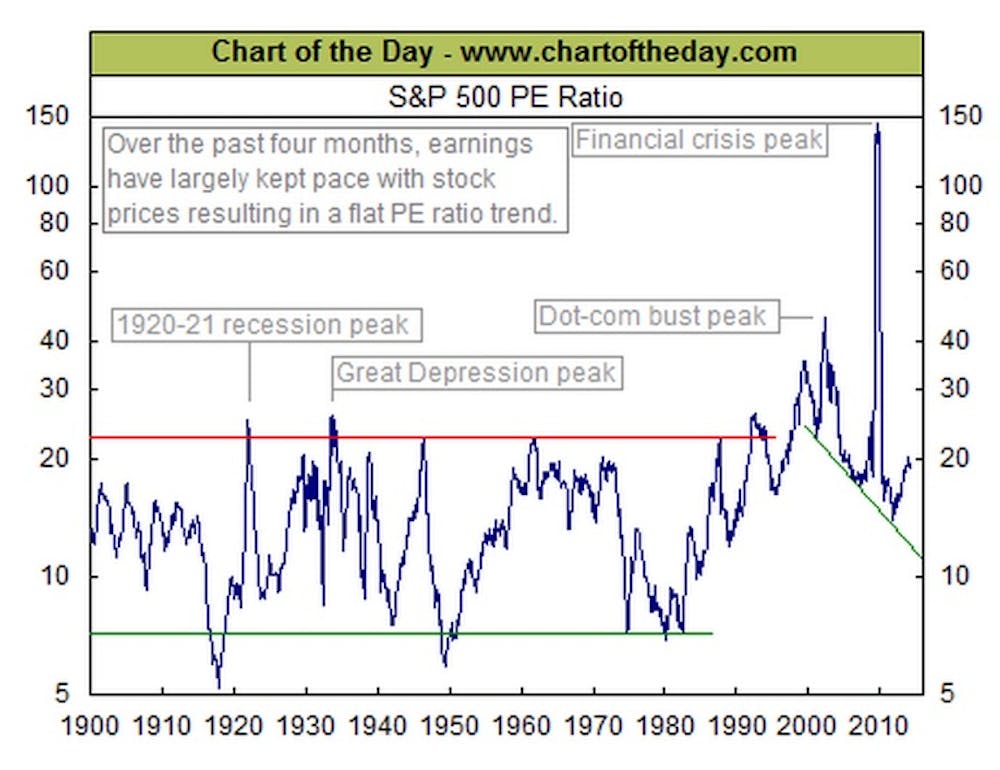

The warning signs are there. Consider the graph below, which plots out the price-to-earnings ratios (P/E ratios) of the S&P 500 over the past century. It is a simple measure of how the stock price compares to the earnings per share, either reported or predicted by analysts. What should be clear from this graph is that P/E ratios greater than 25 are typically the precursors to a financial crisis.

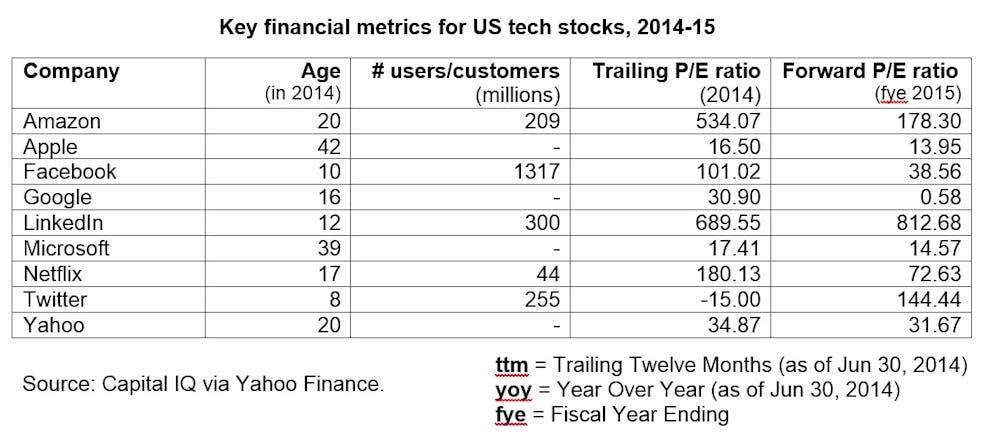

Now let’s consider the P/E ratios of many US tech companies right now. A high P/E ratio is typically considered to be 25+. Many of the current ratios are in excess of 100. This indicates one of three things:

- High expected future growth in earnings.

- This current year’s earnings may be considered exceptionally low.

- The stock may be the subject of a speculative bubble.

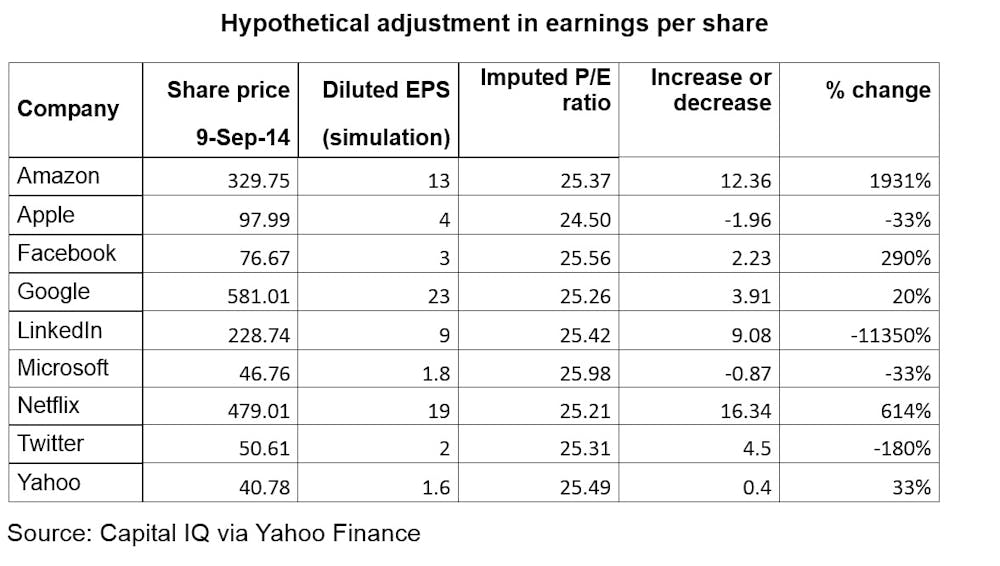

The companies with the highest P/E ratios are the social media tech empires built over the past decade such as Facebook, LinkedIn and Twitter. As it stands, these companies have got to multiply earnings many times over to warrant their current stock prices. In a hypothetical scenario (see table below), where the current stock price is held constant and the earnings per share adjusted to reach a P/E ratio of 25 (still high but not unusual for tech stocks), Facebook would have to triple earnings per share to warrant its current valuation.

The woes of online advertising

What these tech companies have in common is an advertising-based business model. Under this business model, there are two main ways to boost revenues: attract more users or attract a higher price from advertisers for each ad.

The problem for these companies is that user growth has plateaued in recent years. Facebook’s user numbers grew 450% between 2004-2005. Last year, the growth rate was in the mid-teens. Twitter’s story is similar. The growth rate has fallen from around 50% in the year preceding the first quarter of 2013 to 24% prior to the second quarter of 2014. At the beginning of 2010, LinkedIn’s user numbers were growing 73% annually. By 2014, the rate was 32% annually. Sure, a smaller growth rate with a larger base still means many more additional users each year. However, not enough new user numbers are being added to meet revenue targets.

All this means that US tech companies are being forced to boost earnings by extracting higher rates from their targeted advertising. Back of the envelope calculations suggest that advertisers are willing to pay, on average, $7.60 for access to a Facebook user over the course of a year. If we divide this by the 365 days in the year, advertisers are willing to pay an average of $0.02 per day for access to one Facebook user. Don Marti has estimated this to be a quarter of the rate paid for untargeted print ads. The figure for Twitter users is roughly half this amount: about 1 cent per day per user. Advertisers on LinkedIn pay half of a cent each day for access to each LinkedIn user. It’s clear that advertisers aren’t willing to pay much for these supposedly superior, targeted ads.

The only way left to boost revenues is to more finely tune the targeted ads. This requires more and more invasive methods to extract users’ personal data. There’s a hitch though. In 2013, according to Pew, half of Americans said they were “worried about the amount of personal information about them that is online”. In 2009, only a third of the population felt that way.

A casual glance in the media last week told the story of Ello, the social network that doesn’t track user data because it isn’t ad-based. At its peak, it was attracting 50,000 new users an hour. DuckDuckGo, the private search engine, has quadrupled its daily search queries over the past year. Even Facebook has realised the gig is up and is rumoured to be planning a new, anonymous mobile messaging app. US tech companies appear trapped. They cannot boost ad earnings without causing an exodus of the users they so desperately need to retain. Facebook, LinkedIn and Twitter are unlikely to be able to boost profits enough to justify their current, lofty stock prices. The only conclusion that can be drawn is that we are in the midst of another tech bubble.

History repeating

This phenomenon isn’t new and shouldn’t be surprising. The Economist gave an account of past financial crises this year. The parallels between today and the events preceding prior crises are striking. Railway companies boomed before the 1857 crisis, and referring to the lead-up to the Great Depression:

Markets were booming, with the shares of firms exploiting new technologies –radios, aluminium and aeroplanes – particularly popular. But few of these new outfits had any record of dividend payments, and investors piled into their shares in the hope that they would continue to increase in value.

We are simply witnessing the latest chapter in a story of tech booms and busts that traces itself back to the 1800s.

Sustainable revenues = sustainable business

We are left with a simple lesson from all this: sustainable businesses are built on business models with sustainable revenue streams. Social network companies are not exempt from this rule and only when sustainable revenue streams can be found – by providing products and services that someone will actually pay for (end-users or advertisers) – can sustainable tech businesses be built.

The only way out is for the tech companies like Facebook, Twitter and LinkedIn to show that they can indeed attract sustainable revenues, which means abandoning the online advertising business model. If they can’t, an enormous correction in these US tech stock prices will have to happen eventually.

A full version of this paper is available for pre-publication comments and discussion