For many years Western Australia enjoyed solid economic growth, matched by business investment and an unemployment rate lower than the national average. But it’s been a couple of years since investment in the mining industry peaked, and it’s time to take stock.

The WA economy has performed well, considering the downturn that arose as the mining industry moved from a capital construction phase to a production phase. But this has soured recently, and unless something is done to address increasing unemployment, and decreasing participation rates and economic growth, tough times are ahead.

Declining fortunes

Most commentators remember the exceptional growth WA has seen over the last 10 years though the more recent news has not been so great. Indeed, WA has stood out among the Australian states with 10 year average compound growth in Gross State Product (GSP) of 5% to 2015-16. The next ranked state was the Northern Territory with growth rate of 3.9%.

But the memory of these strong growth numbers masks recent poor performance. The Western Australian economy posted a dismal 0.7% growth in GSP per capita in the year 2015-16, a number shared only with Queensland.

Further, WA’s Real Gross State Income - a measure that also includes adjustment for purchasing power, was actually negative in the year 2015-16, at -6.4%. The next worst performing state was again Queensland, although it at least achieved a 1.1% growth rate.

The impact of decreasing capital expenditure is particularly evident in the State Final Demand figures - a measure of domestic demand. Demand in Western Australia actually shrunk, declining 4%. Only the Northern Territory performed worse, declining by 12.5%. New South Wales managed to grow 3.9% and Victoria 3.8%.

The government perspective

WA’s latest budget includes around A$7.7billion in infrastructure development. But despite this, state government expenditures are contracting with considerable downward pressure on wages and other expenditures over the last two years. Expenditure growth is presently running at 2.4%, which is the second lowest rate of growth in more than 20 years.

The government has also continued with its asset sales program which stands at A$2.2 billion dollars at present. These reductions in government expenditures and increases in asset sales occurred during a period of declining royalties, declining GST allocation and declining collections from taxes like payroll tax, which saw the first decline in more than 20 years.

Indeed, the only real good news with royalty collection was with gold, where royalties increased from A$229 million to A$250 million in the 2015-16 year. Overall, the cuts in expenditure and asset sales have certainly reigned in the growth in debt, though the state is still indebted to the amount of A$27.3 billion.

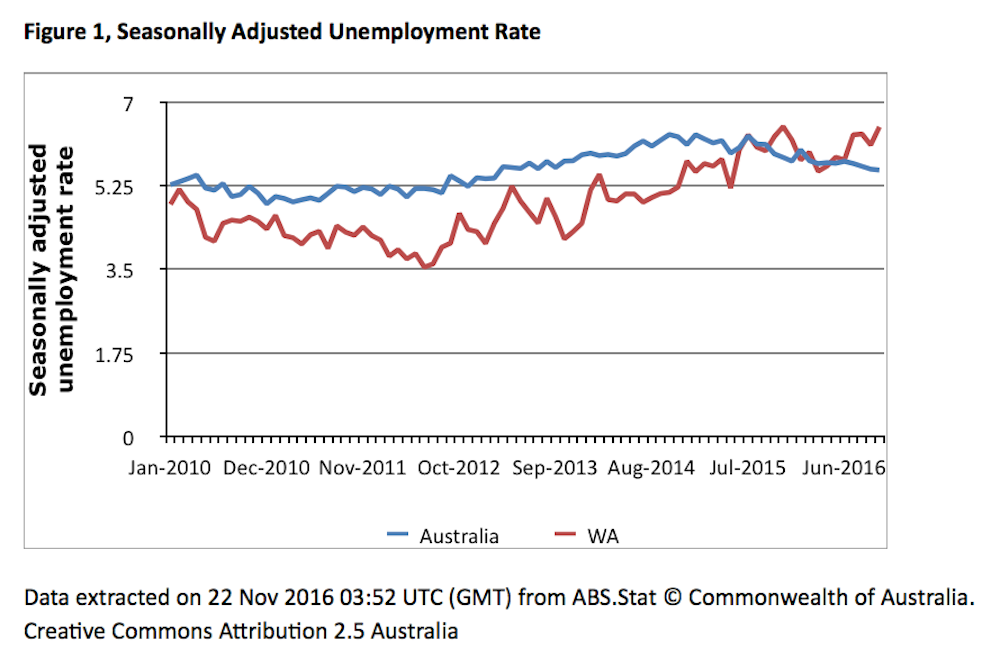

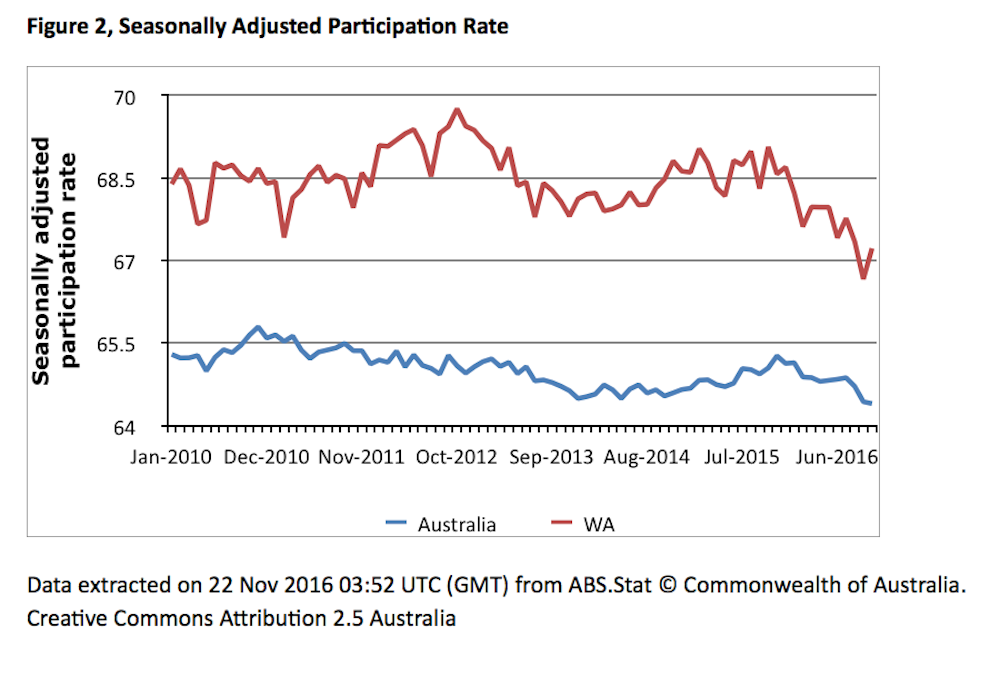

Increasing unemployment and declining participation

Job cuts are widely reported in the WA press. The unemployment rate has increased fairly consistently since 2012 and this has continued regardless of the Australian unemployment rate falls that have taken place since early 2015.

The WA labour force participation rate has also seen dramatic change since 2015 with a fall from 69% in February 2015 to 67% in October 2016. An increasing population coupled with increasing unemployment rate and decreasing participation rate is not good news for the citizens of WA.

Western Australia needs to do something

In short, WA has been doing exceptionally well until quite recently. Western Australian Treasurer Mike Nahan expects the economy to pick up once the massive natural gas projects start to produce in earnest. Recent increases in iron ore and crude oil prices and the continuing strength of the gold price can only further support this contention. Although it is difficult to know how these projects will benefit the ordinary voter who could be facing prolonged periods of unemployment.

The Western Australian government could do more, drawing on fiscal policy and monetary policy to stem the adverse movements in employment and growth, though there is a limit to what a state government can do.

Increases in government investment in infrastructure projects could help to stem increases in unemployment. Lower unemployment levels will help to raise consumer demand in the state. But new infrastructure projects will require financing and this will either come at the cost of increased taxes or increased borrowing.

Private companies could also step in, but the appetite for foreign private investment in state infrastructure does not appear strong at present, particularly given the reaction to the lease of Darwin’s harbour. The federal government has a role to play here as well, particularly with funding key infrastructure projects in the state.

Unless something happens soon to turn the tide, increasing unemployment rates, lower participation rates and decreasing economic growth suggest the state is heading for some rather difficult times.