Russia’s Central Bank has raised its key interest rate from 10.5% to 17% in an emergency move that is designed to halt the ongoing collapse of the rouble, which has accelerated in recent weeks. The dramatic intervention comes after the rouble suffered its worst one-day fall since the August 1998 financial crisis.

The interest rate hike briefly prompted a sharp jump in the Russian currency – it rose by almost 10% in early trading on the morning following the hike on Monday December 15. But by midday in Moscow, the rouble had already lost all its early gains and was weakening further.

Close to panic

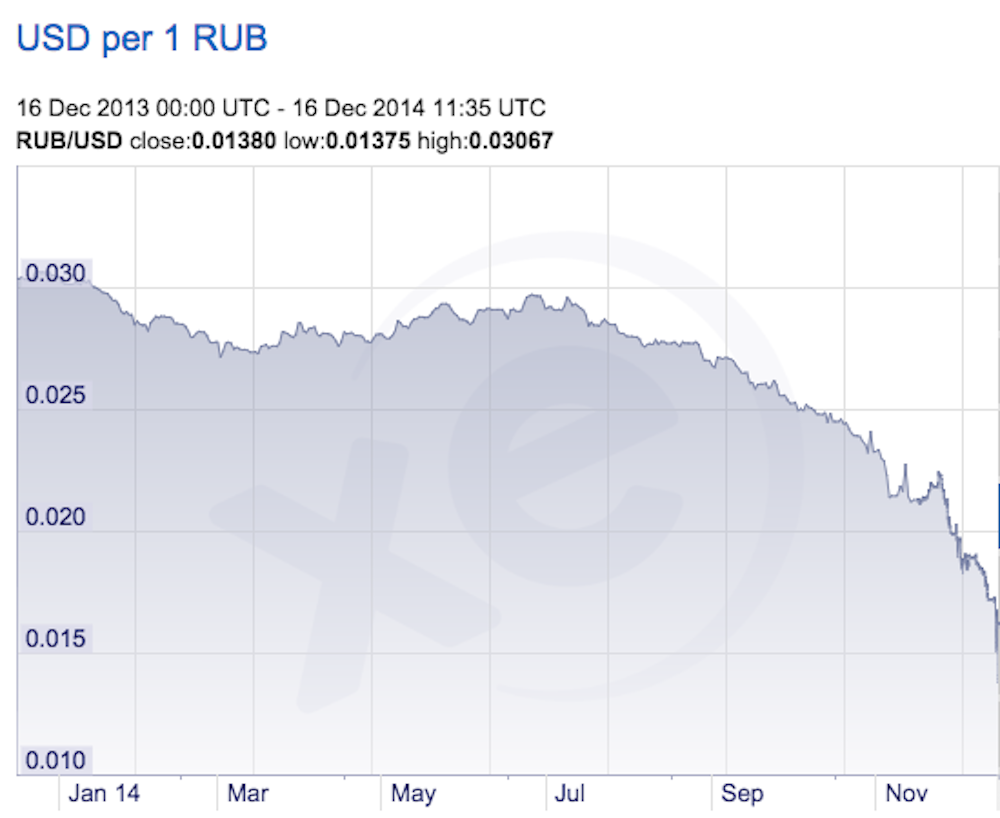

The rouble has now lost well over 50% of its dollar value since the year began. Most of this precipitous decline can be explained by the steep fall in oil prices since the summer. Oil is now close to US$60 per barrel, a shock to oil producers used to prices closer to US$110 per barrel in recent years. But the rouble is depreciating at a faster rate than oil, which means that other factors are at play.

The imposition of Western sanctions hasn’t helped. International capital markets are now largely closed to Russian firms, with net private capital outflows increasing as firms pay back their external debt. However, even this fails to explain the pace of the rouble’s decline in recent weeks, with the trajectory of the rouble suggesting that the value of the currency is becoming disconnected from any of these fundamental, underlying issues.

Instead, what we are now seeing is close to panic – no doubt fuelled by speculators from within Russia’s banking sector. This near panic has emerged as policy makers look increasingly unable to manage the rapid deterioration of many economic indicators. As former Finance Minister, Alexei Kudrin, remarked early Tuesday morning on Twitter: “The fall of the rouble and the equity market is not only a reaction to the low price of oil and sanctions but to a distrust of the government’s economic measures.”

Not an inordinately high rate

On the face of it, a hike of 6.5% in one day is an extraordinary measure. However, it is worth bearing in mind that the rate of inflation in Russia is currently close to 10%, itself exacerbated by the recent decline in the value of the rouble. This means that Russia currently has a real interest rate of around 7%.

This is high, but not inordinately so. Central bank officials will also hope that by boosting their own credibility, the rate hike will deter speculators from betting against the rouble in the future, allowing the bank to reduce interest rates soon. Quite simply, the measures are about the Russian Central Bank restoring credibility and showing that it is in control of the rouble’s destiny.

Should interest rates stay at this level or rise even further, the extent of the damage that this will cause to the wider Russian economy is unclear. It is plausible that high interest rates may not be as damaging as some might expect. In Western markets, we’re used to highly active banks, set up to funnel lending into businesses to fund growth. In Russia however, the financial sector has been far less aggressive, and companies have tended to rely on cash reserves to a far greater extent.

As a result, the non-financial corporate sector may not suffer as much as some might expect as they will not see a dramatic increase in borrowing costs. Plus, the financial sector may benefit from extra liquidity should the CBR’s gamble pay off and capital flows return to Russia. The consumer credit boom that Russia has experienced in recent years, however, may leave many Russian consumers and homeowners, especially in larger cities, vulnerable to an extended period of high interest rates.

{kind=link}

Massive gamble

The actions are a massive gamble by Elvira Nabiullina, the Chair of Russia’s Central Bank, and one of Russia’s leading liberal policy makers. She and her team have come under massive pressure in recent weeks, and have been accused of losing control over monetary policy. If the rate hike works, it should begin to restore the central bank’s credibility, which may in turn arrest the decline of the rouble and restore order to currency markets.

But if Nabiullina’s gamble doesn’t pay off, there is a danger that the Russian Central Bank will have exhausted all its remaining credibility. In this case, Nabiullina’s position will come under threat, and the imposition of capital controls of some description will become much more likely.

This would see much tighter regulation of the flow of capital markets in and out of the country. It’s a measure that hard-liners from within the Russian elite have been calling for for much of the year. They are seen as a way to reassert central control over economic activity in Russia, and of insulating Russia from the outside world.

This kind of move would form part of a wider reassessment of Russia’s relationship with the global economy and the balance between state and market in Russia’s economy. Thus, the actions are of great importance, not just for the trajectory of the rouble, but for the future direction of economic policy in Russia