The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set. Timo Henckel is the non-voting chair of the board.

Gyrations in global financial markets make Australia’s economic outlook very uncertain. The US economy is expanding, whereas other regions are flirting with recession. Domestic growth remains slightly below trend and headline inflation is below the official target band of 2-3%. The collapse in oil prices, the weakened Aussie dollar and renewed doubt about the viability of the eurozone add uncertainty to the global economic outlook.

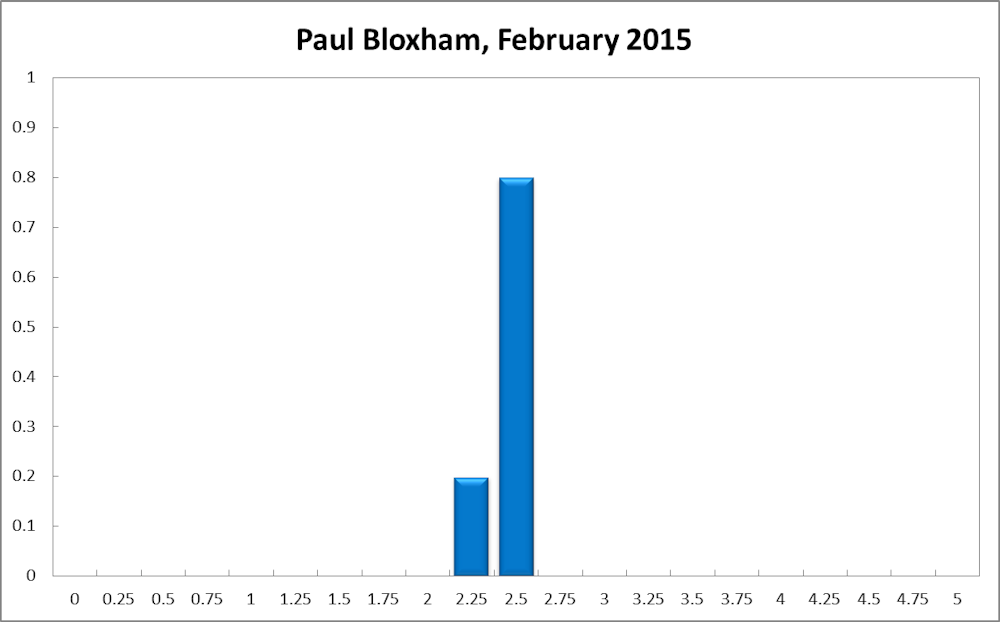

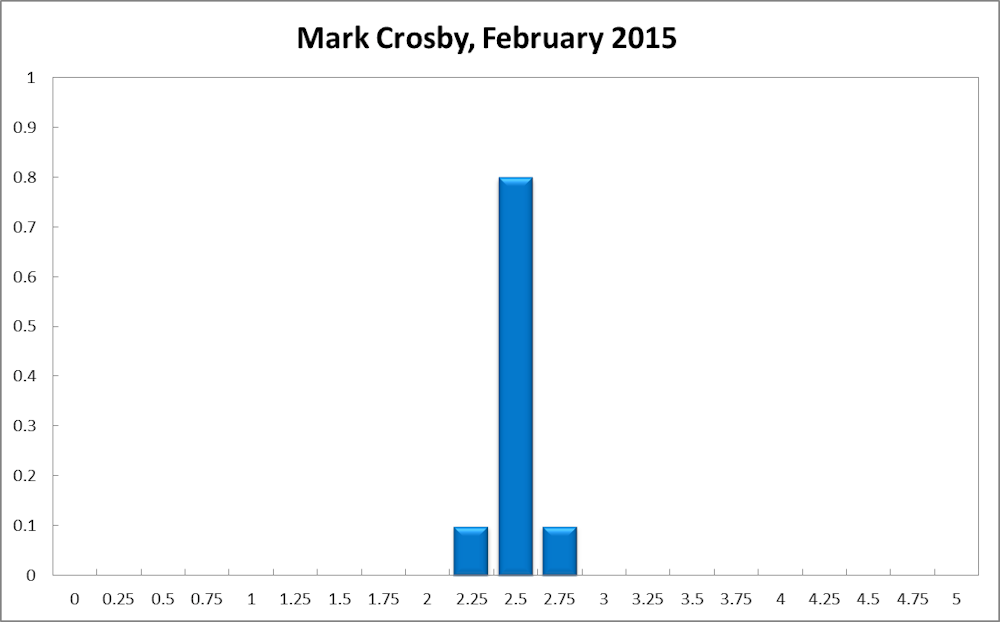

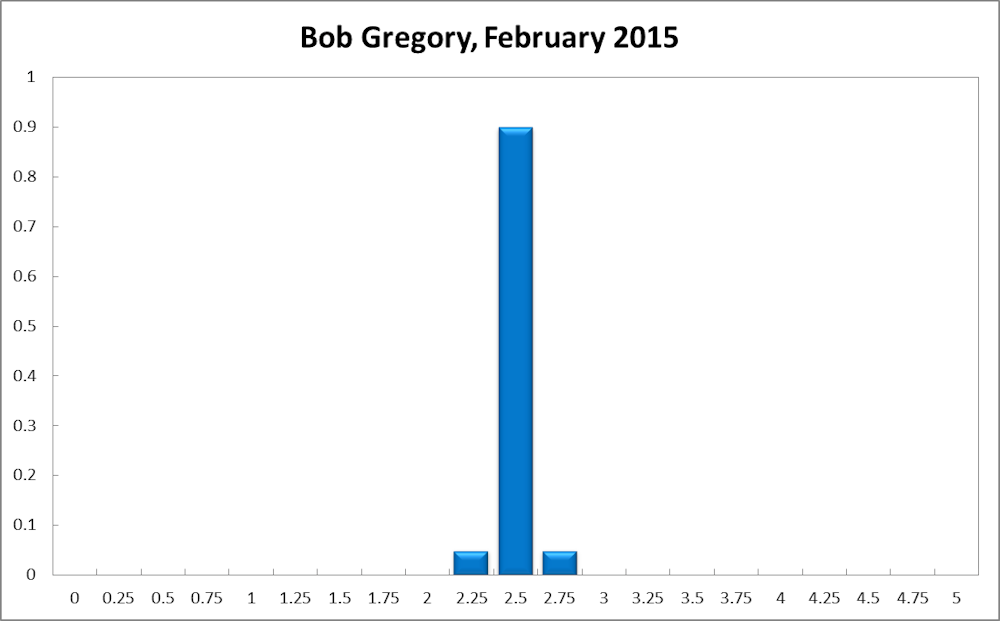

The CAMA RBA Shadow Board continues to recommend with confidence that the cash rate be held at its current level of 2.5%; the board attaches a 68% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 13%, while the confidence in a required rate hike has decreased to 19%.

According to the Australian Bureau of Statistics, headline inflation has fallen to 1.7%, below the official target band of 2-3%. Much of this can be attributed to the fall in energy prices. The implications of this are unclear, as the drop in oil prices is the result of reduced demand as well as increased supply. In the medium term the latter can be expected to be expansionary for the Australian economy.

Core inflation, a measure of inflation that excludes volatile items such as energy and food, currently lies at 2.1% – within the official inflation target band – and is a better gauge for setting interest rates. It suggests that the drop in energy prices does not call for an immediate reduction in the cash rate.

After an extended period of low volatility, during which the Australian dollar hovered around the 85 US¢ mark, the currency has fallen another 8 US¢. If the dollar remains below 80 US¢ for some time, exports, in particular the tourism and education sectors, should expand appreciably and boost domestic production.

Some slack remains in the Australian labour market, with the Australian Bureau of Statistics’ most recent estimate of the unemployment rate being 6.1%. The labour force participation rate has picked up a little to 64.72%, while the change in employment, at around 40,000 per month, has been solid for the past two months.

These figures suggest that the rebalancing of the Australian economy, away from the resources sector, is reaching the labour market. However, wages growth remains muted and a growing share of employment is part-time.

Commodities and currencies volatile

The key headlines during the past weeks have centred on events in financial markets. WTI crude oil has fallen from over US$100 a barrel to under US$45 a barrel in less than a year. Prices for other energy goods have fallen significantly also, as well as the price for iron ore.

Global currency markets were in turmoil when the Swiss National Bank unexpectedly abandoned its cheap Swiss Franc policy and let the currency float freely. The outcome of the Greek election once again places question marks over the viability of the eurozone as Greece will need to borrow additional funds to service its existing debt.

These uncertainties, along with promising signs coming from the US economy, have made global investors favour the US dollar. In trade-weighted terms the US dollar has appreciated approximately 10% during the past six months.

Confidence subdued

Consumer confidence remains subdued, with the Westpac Consumer Sentiment Index coming in at 93.2 this month (91.1 in the previous month, 98.47 six months ago). Capacity utilisation remains virtually unchanged at 80.48% in December, while the manufacturing PMI has fallen considerably (from 50.08 in November to 46.91 in December).

Conversely, the Services PMI jumped from 43.80 to 47.50 in December and the NAB monthly survey of business confidence remains weak at 2 (1 in November, 10 in August 2014). The Westpac-Melbourne Institute Leading Index of Economic Activity remained steady.

The outlook for the global economy remains uncertain, though attention has shifted from geopolitical factors to financial factors. Europe is still looking weak – the European Central Bank recently announced a large-scale sovereign bond purchasing program to avoid deflation and boost growth in the eurozone, and Germany is considering another Euro 20 billion bailout package for Greece.

No further economic impulses are to be expected from China, nor from Japan. The US economy is faring better but growth continues to be highly unequal. A sustained upturn in the US economy needs to rely on significant wages growth for the middle class.

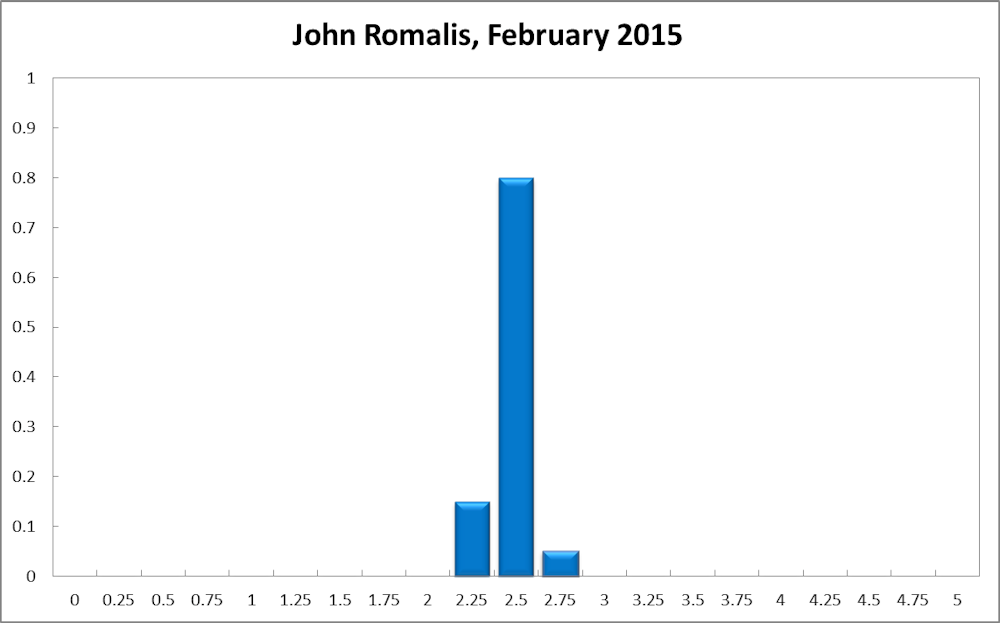

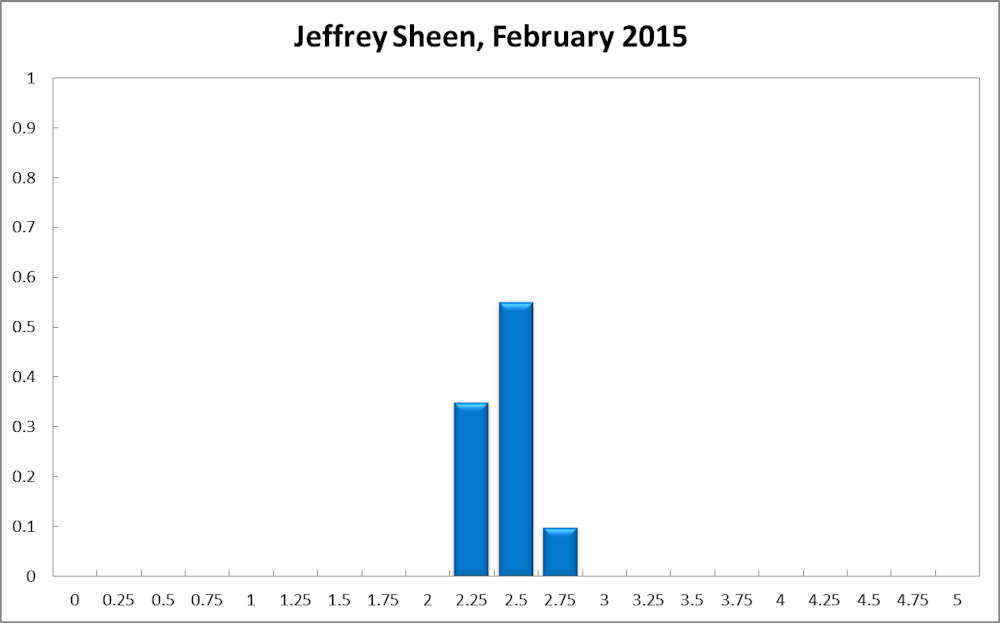

The consensus to keep the cash rate at its current level of 2.5% slipped two percentage points to 68%. The probability attached to a required rate cut increased noticeably to 13% (5% in December) while the probability of a required rate hike has fallen to 19% (25% in December).

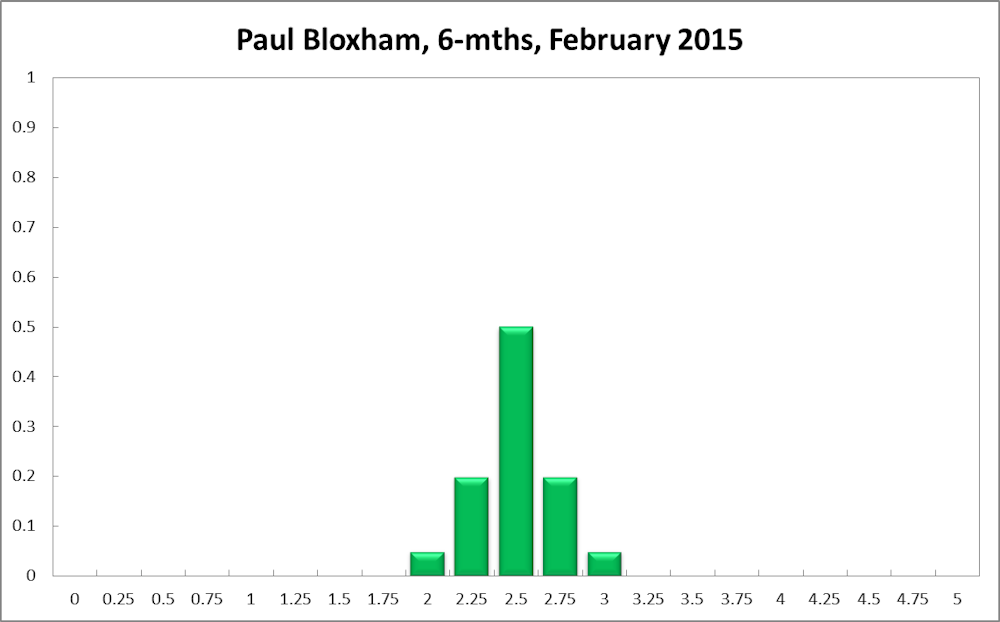

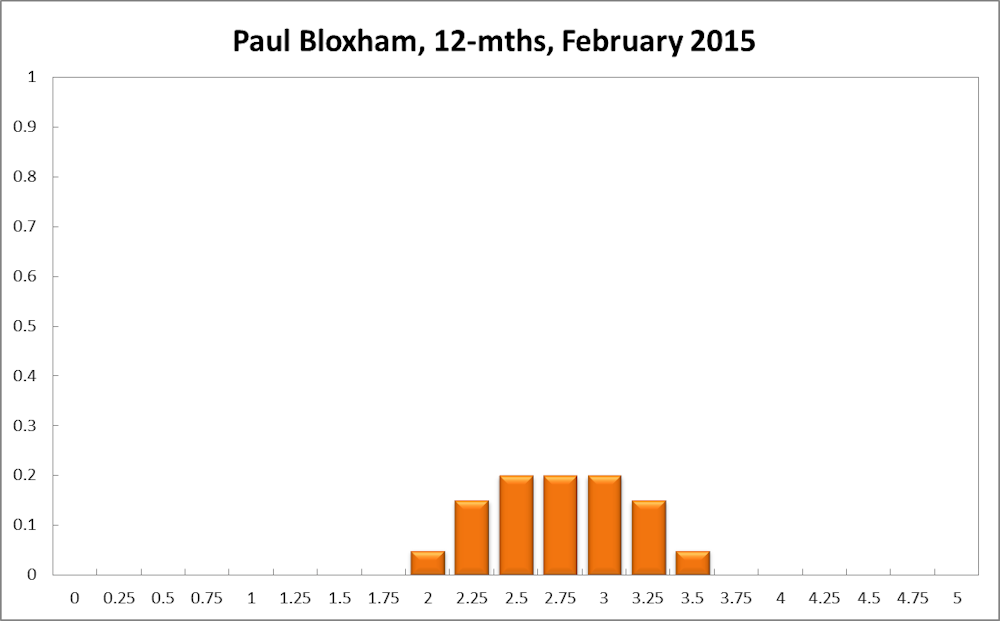

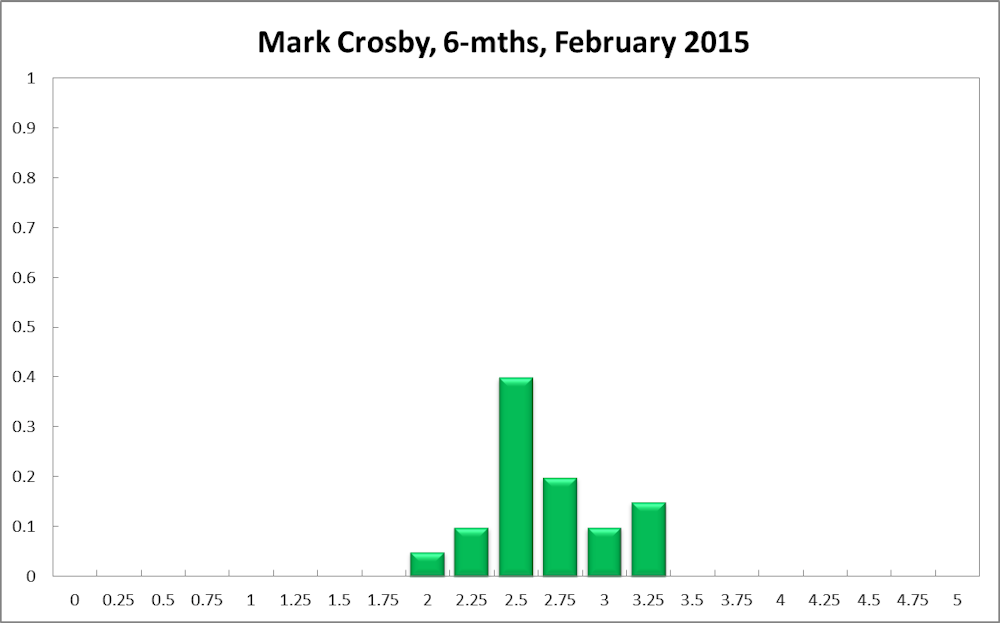

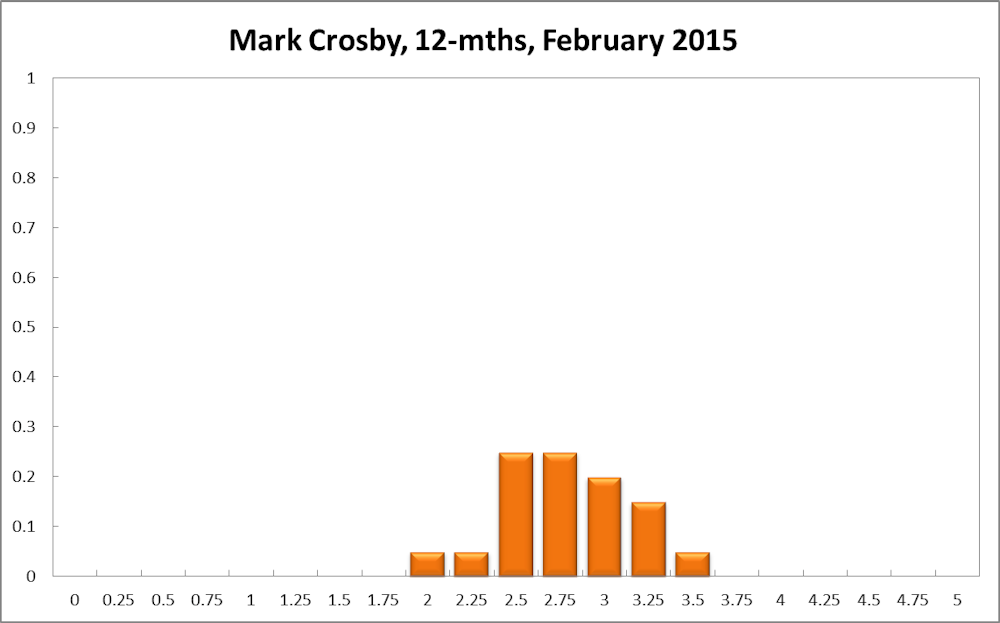

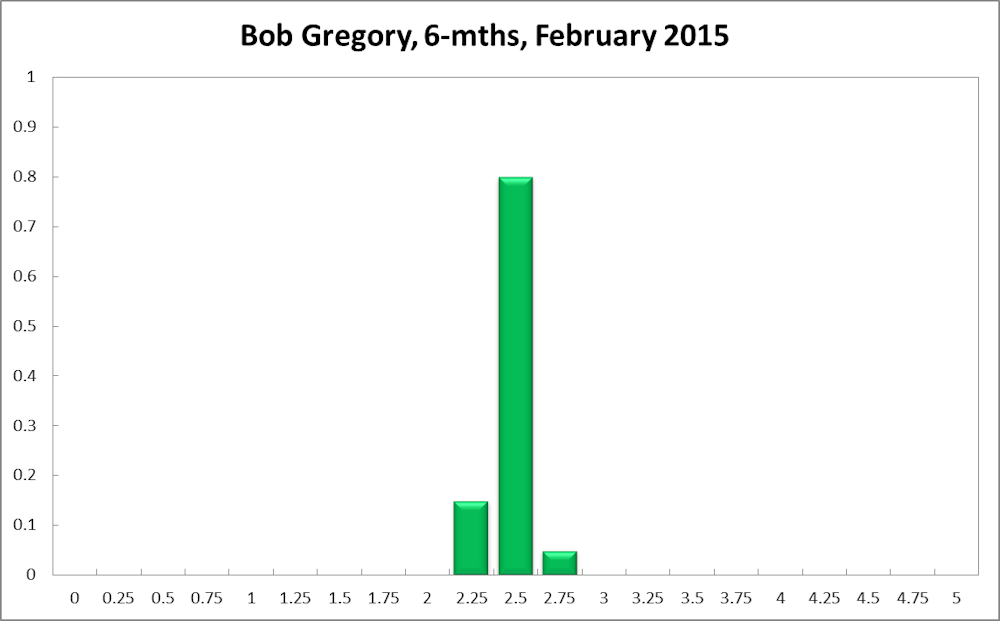

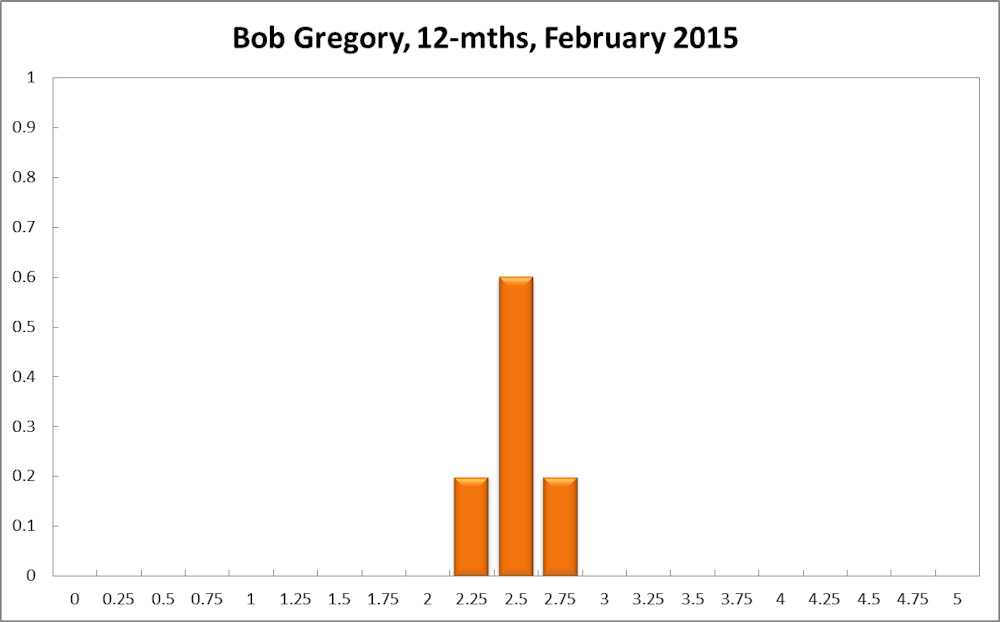

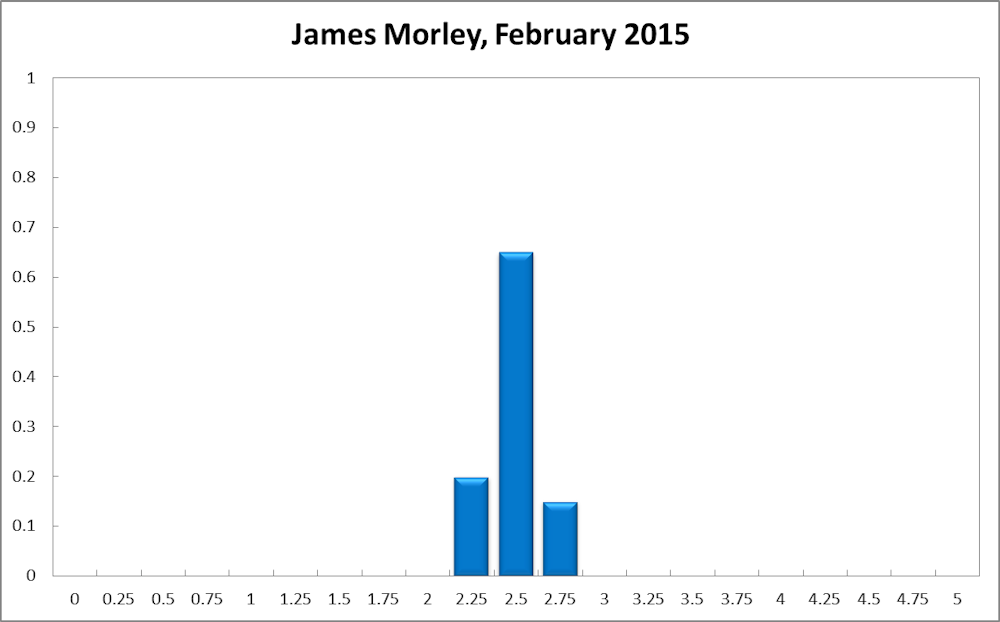

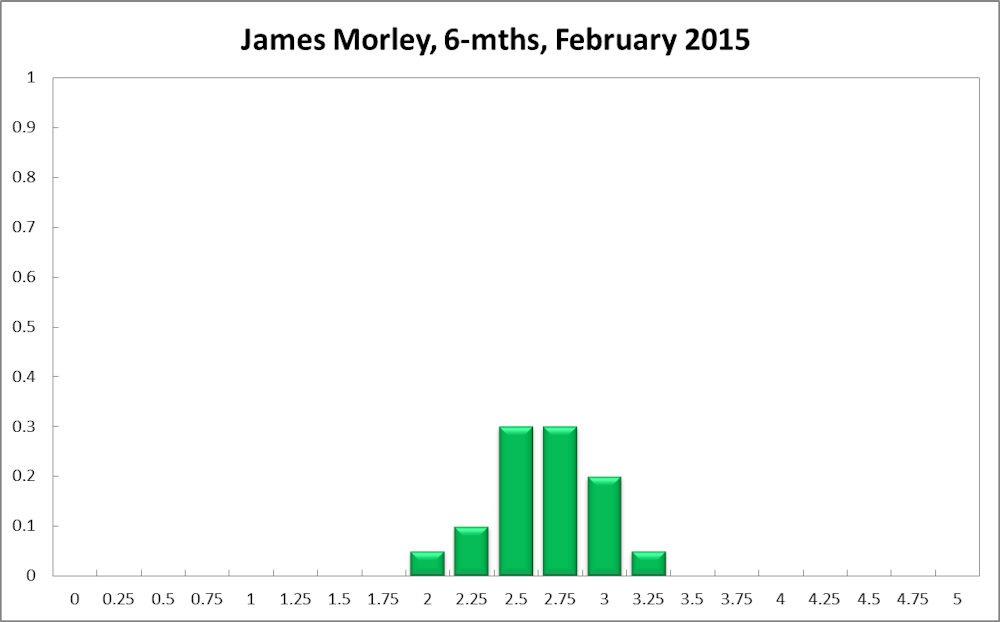

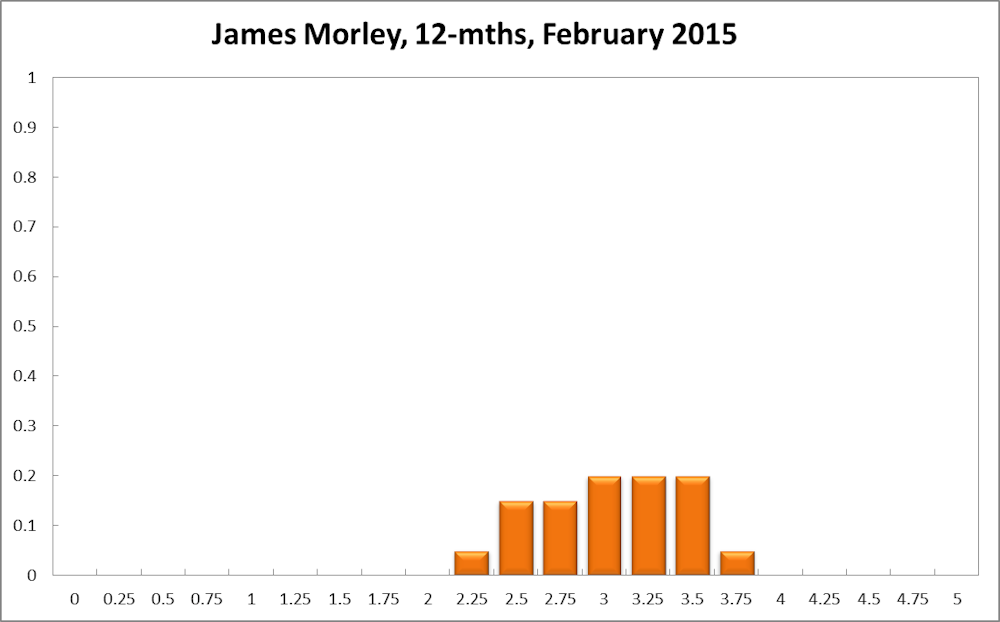

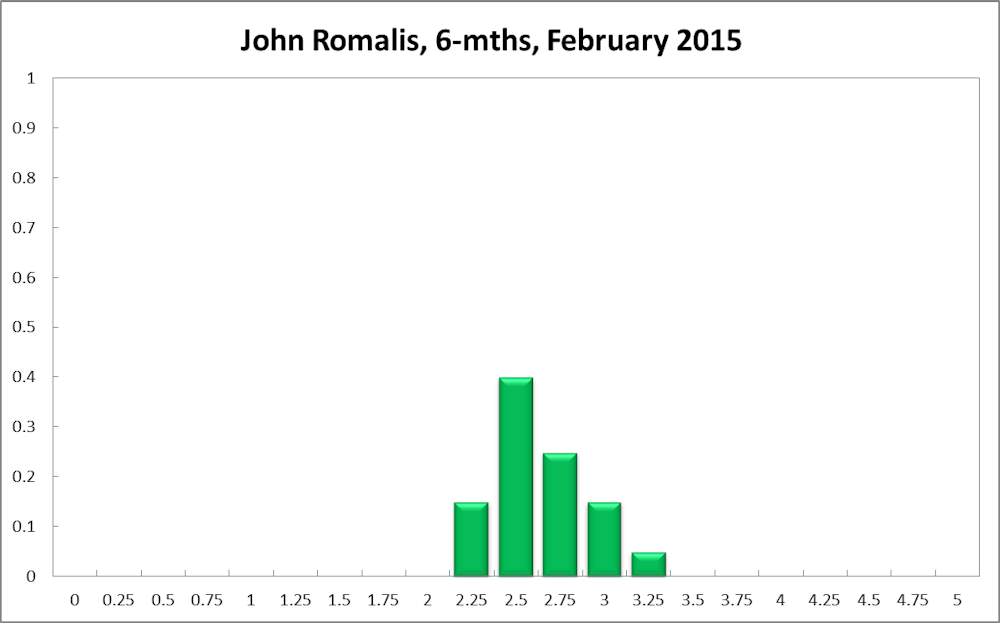

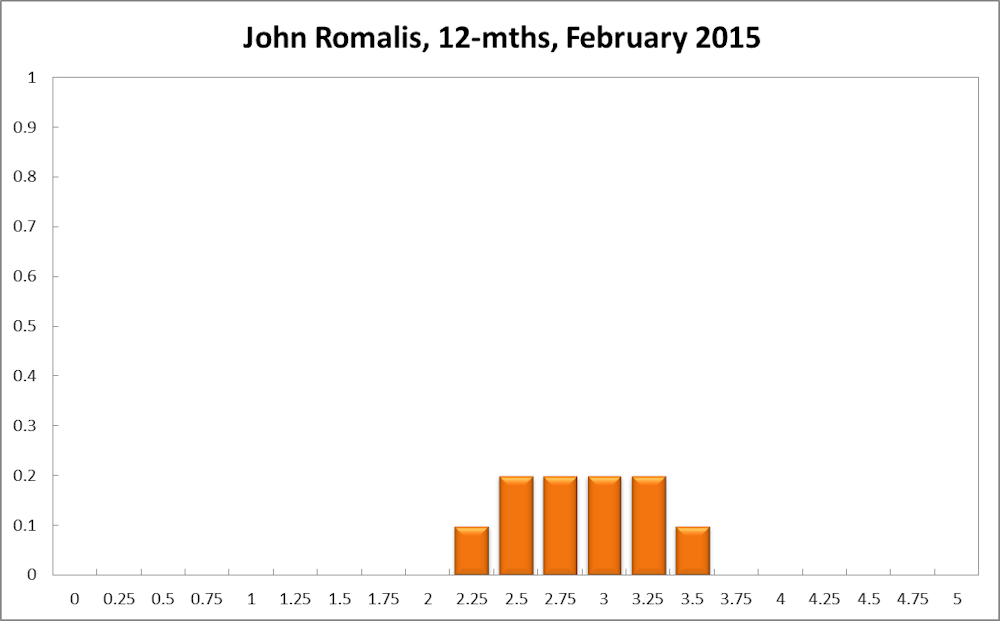

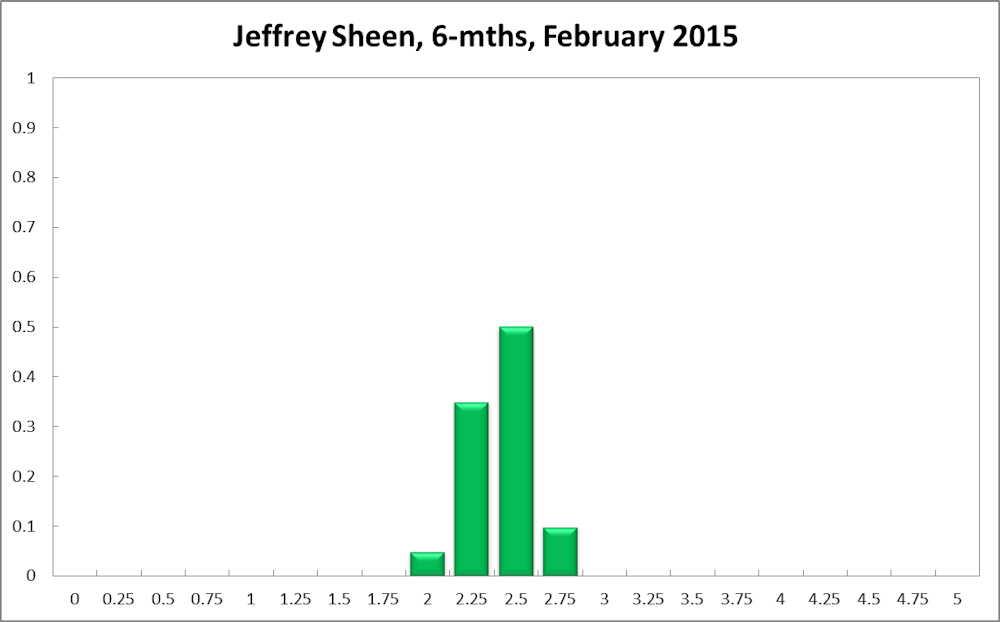

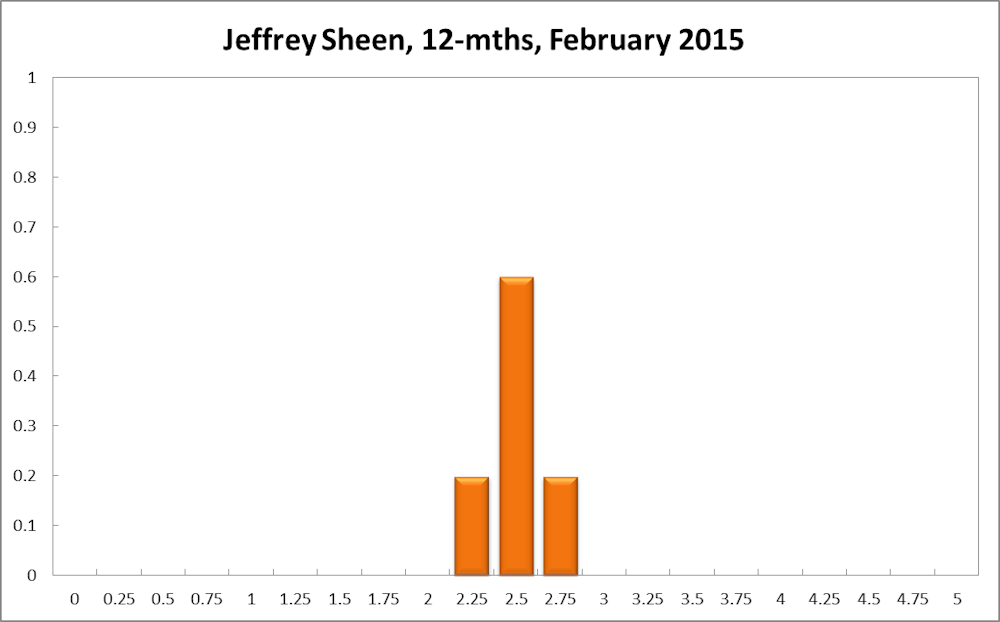

The probabilities at longer horizons are as follows: six months out, the probability that the cash rate should remain at 2.5% rose ten percentage points, to 46%. The estimated need for an interest rate increase plummeted to 38% (56% in December), while the need for a decrease rose to 16%. A year out, the Shadow Board members’ confidence in a required cash rate increase is down ten percentage points to 61%, the need for a decrease edged up to 11% (10% in December), while the probability for a rate hold is 29% (22% in December).

Comments from Shadow Reserve bank members

Paul Bloxham, Professor of Economics at Australian National University:

“In principle, the fall in oil prices should be a net positive for local growth.”

Since the last board meeting there have been a number of global developments with local relevance. The most significant has been the continued dramatic fall in global oil prices, which are now 60% lower than in the middle of last year.

The fall in oil prices reflects both weaker global demand and a boost to supply. It is still too early to tell which of these forces is the most significant. Markets have generally interpreted the fall as at least partly due to weaker demand, with global bond yields falling, as inflation is expected to be lower.

Consumer price inflation is falling across many countries, with a number of central banks already responding by lowering interest rates. Europe has also seen significant financial developments in the past month, with the ECB beginning a sovereign bond purchasing programme, the Swiss abandoning their exchange-rate ceiling and the election of a new government in Greece once again raising concerns about the possibility of that country exiting the eurozone. This has generally seen a flight to quality assets, further pushing government bond yields lower in a number of countries.

For Australia, the economic indicators have continued to show signs that low interest rates are supporting a pick-up in activity. Housing prices and construction activity have continued to pick up and retail sales have been growing solidly. Surveys suggest business conditions have generally been trending higher, although business confidence remains weak.

Working in the other direction, mining investment is falling, although this is being largely offset by a ramp-up in resources exports, as new capacity comes on line. The net effect of these divergent forces on local demand is difficult to assess, but the solid underlying inflation numbers for the fourth quarter of 2014 (0.7% quarter-on-quarter) give some indication that demand is holding up. The 8% fall in the Australian dollar since the last board meeting should further help to support the rebalancing of growth and local demand.

The fall in oil prices, combined with the repeal of the carbon tax last year, has seen headline CPI inflation fall below the bottom edge of the target band (1.7%). As a result of lower petrol prices it is likely to fall further in Q1.

However, for the setting of monetary policy it is the outlook for underlying inflation and inflation expectations that matter most. In principle, the fall in oil prices should be a net positive for local growth, as Australia is a net petroleum importer, and lower petrol prices should boost household disposable incomes and business profits.

Although there is some scope to consider cutting the cash rate in the short run, as headline inflation will be lower than previously expected due to lower oil prices, it is the medium-term outlook for inflation that matters most. In the medium term, the effect of lower oil prices is somewhat ambiguous, but I view it as more likely to be an upside risk than downside risk to underlying inflation, as I expect the boost to demand from lower petrol prices to more than offset the negative impact on the domestic economy of lower oil prices on energy exporters. In addition, there is the ongoing risk that further interest rate cuts could risk over-inflating an already booming housing market. I recommend that the cash rate is left unchanged.

Mark Crosby, Associate Professor, Melbourne Business School:

“With underlying inflation in the desired range, waiting would seem to be a better approach.”

Despite recent headline inflation below 2%, there is little reason for the RBA to take other than a wait-and-see approach to the cash rate. International developments remain highly uncertain, with Europe and Japan remaining weak, while the US continues to recover.

With underlying inflation in the desired range, waiting would seem to be a better approach than using up ammunition, given fragility in the global economy.

Bob Gregory, Professor of Economics at Australian National University:

This is becoming very difficult because although the Australian economy is going down in my view, I have no idea what will happen to world rates – except that the US and Europe will diverge – and no idea at this time as to how we will or should respond to this.

The increased uncertainty about world interest rates has encouraged me to essentially sit tight on our interest rates until I get a clearer fix on what is happening. Obviously, not expecting a large change in either direction.

James Morley, Professor of Economics and Associate Dean (Research) at UNSW Australia Business School:

“Lower oil prices are more of a net positive for the Australian economy than for Canada.”

Headline inflation, currently at 1.7%, should be expected to remain below the 2-3% target range in the near term given the dramatic recent decline in oil prices. This provides considerable scope for the RBA to delay any increases in the policy rate until at least the second half of the year.

The continued collapse of iron ore prices and the decline in oil prices has prompted some speculation that the RBA will lower rather than raise rates in the near term, especially after the Bank of Canada recently lowered its policy rate in response to the decline in oil prices. It is possible that the RBA will do so.

However, it should be noted that lower oil prices are more of a net positive for the Australian economy than for Canada. And the lower Australian dollar has meant that there will be a broader compensation for the end of the mining boom than just strong growth in interest-sensitive sectors (e.g. construction). In particular, non-mining exports (e.g. higher education and tourism) can be expected to perform well. A robust recovery in the United States also provides some offset for the weaker-than-normal (but still fast) growth in China.

Overall, then, I would recommend the RBA maintain, but not lower, its already low policy rate and monitor how effectively the lower dollar stimulates non-mining exports. Any change in policy direction should be signalled by public communications (i.e. moving away from a reference to “a period of stability in interest rates” in policy statements) rather than trying to surprise markets, as was recently done by the Swiss National Bank in terms of its unconventional monetary policies.

John Romalis, Professor of Economics at the University of Sydney:

There seems to be insufficient reason to change the current target cash rate. Inflation still seems likely to remain at moderate levels. Below-trend GDP growth and no obvious indicators of rapid expansion suggest that a low cash rate is still appropriate.

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“There is significant potential for destabilisation of asset markets within Europe.”

In the last two months, observed indicators of the Australian economy have weakened marginally. Aggregate hours worked declined by an annualised 3.7%, though the unemployment rate has fallen slightly to 6.1%. Inflation is at the bottom end of the RBA’s target range, helped down by the fall in energy and transport costs, which are likely to remain low for some time.

The trade-weighted index has depreciated significantly in the last half-year (by 15% annualised), which should eventually boost net exports. However, more depreciation is needed to seriously stimulate the below-normal growth of the Australian economy.

External risks have increased as a result of the recent election in Greece. There is significant potential for destabilisation of asset markets within Europe. The ECB will surely conduct large quantitative easing, helping to keep interest rates low.

The strengthening US economy is a major positive influence for the global economy, but not enough to prevent the IMF from predicting weakening global growth in 2015.

Overall, this indicates that the RBA should be delaying any plans to raise the cash rate in the future, and increases the probability of a cut in the next few months. I recommend no change this month.