The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set. Timo Henckel is the non-voting chair of the Board.

The RBA’s decision to cut the cash rate to 2% last month went against the recommendation of the CAMA RBA Shadow Board. Since then economic data continues to show signs of weakness. Unemployment is up slightly, investment down, and consumer and business confidence remain fragile.

The international economy continues to pose a threat to the Australian economy and inflation remains comfortably within the RBA’s target band. But asset prices, Sydney house prices in particular, continue to post high gains.

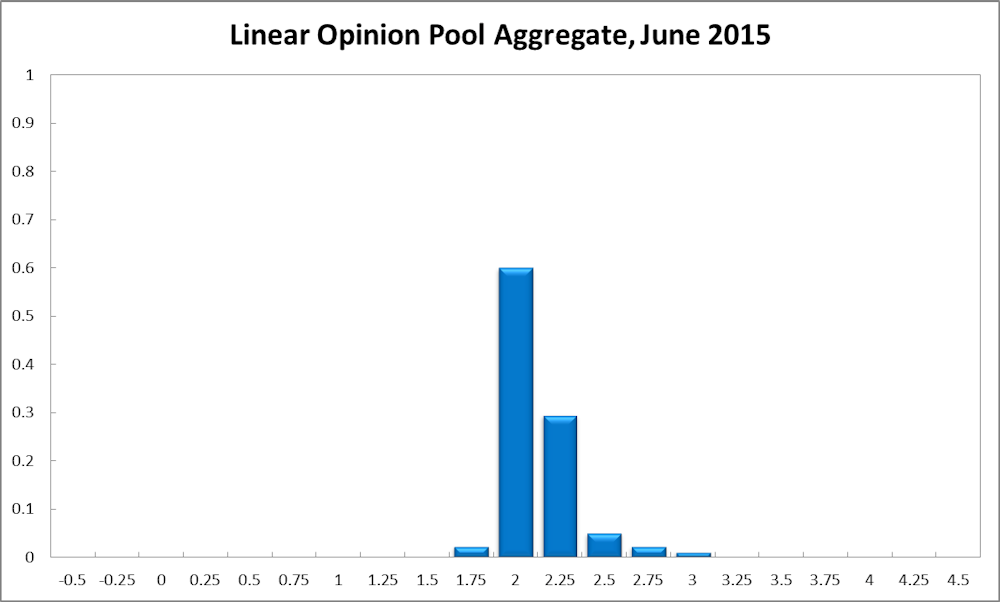

The CAMA RBA Shadow Board on balance prefers to hold firm but believes the cash rate has bottomed and an increase is due in the near future. In particular, the Shadow Board recommends the cash rate be held at its current level of 2%; it attaches a 60% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals a mere 2%, while the confidence in a required rate hike stands at 38%.

According to the Australian Bureau of Statistics, Australia’s jobless rate edged up to 6.2% in April. Worryingly, in the same month full-time employment, total employment and the participation rate have fallen. Wage growth remains at a record low: the Australian wage price index increased by 2.3% in the last quarter, well below the average of 3.5% for the period 1998-2015.

The Australian dollar remains range-bound between US76¢ and US80¢. Yields on Australian 10-year government bonds have increased further, to 2.84%, from its recent low of 2.59%, implying a steepening of the yield curve, normally a bullish sign.

Regional housing markets, particularly Sydney and Melbourne, and domestic share prices remain buoyant. This remains a primary concern for many Shadow Board members as the asset price increases coincide with an increase in private sector leverage, leading to misallocated investment and opening up the possibility of a costly price correction. According to the Reserve Bank of Australia total housing credit grew by 7.2% (year-ended) in April 2015, compared to 6% in April 2014.

The international economy remains subdued. For Europe, a noticeable pickup in growth is not on the horizon, at least not until the Greek debt crisis is resolved. Recent revisions of US data indicate that US growth this year has been slower than initially thought, with some analysts suggesting the US economy actually contracted in the first quarter. Without a string of good news about the US economy, the Federal Reserve Bank’s increase of the cash rate is likely to be pushed back ever more. Commodity prices are likely to remain soft and possibly fall further.

Consumer and producer confidence measures continue to be mixed. However, of particular concern is the outlook for domestic investment. The ABS survey of chief financial officers conducted in April and May of this year reveals that total capital expenditure is still expected to fall significantly, with the current estimate for fiscal year 2015-16 being 24% less than the corresponding estimate for fiscal year 2014-15. The trend volume estimate for total new capital expenditure fell 2.3% in the March quarter 2015 while the seasonally adjusted estimate fell 4.4%.

What the Shadow Board believes

The Shadow Board’s confidence that the cash rate should remain at its current level of 2% equals 60%. The confidence that a rate cut is appropriate is a mere 2%, whereas the Shadow Board considers it much more likely (38%) that a rate increase, to 2.25% or higher, is the appropriate policy decision for this month.

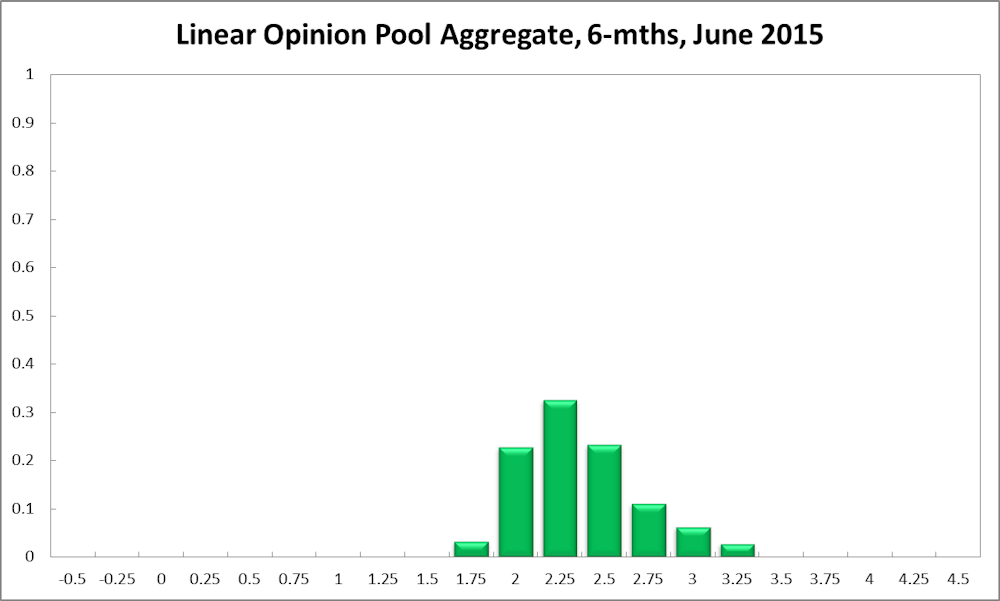

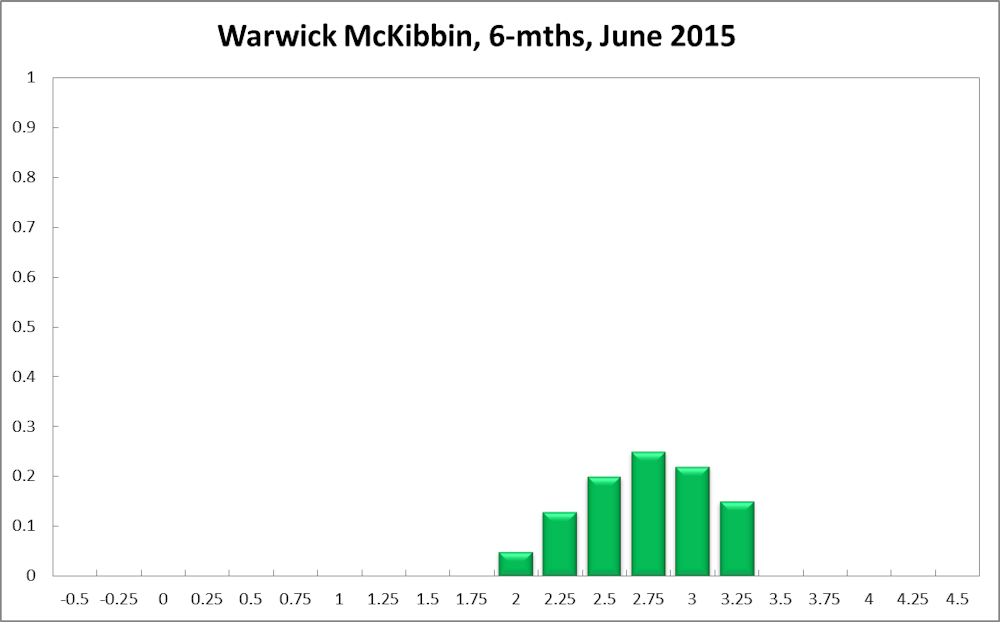

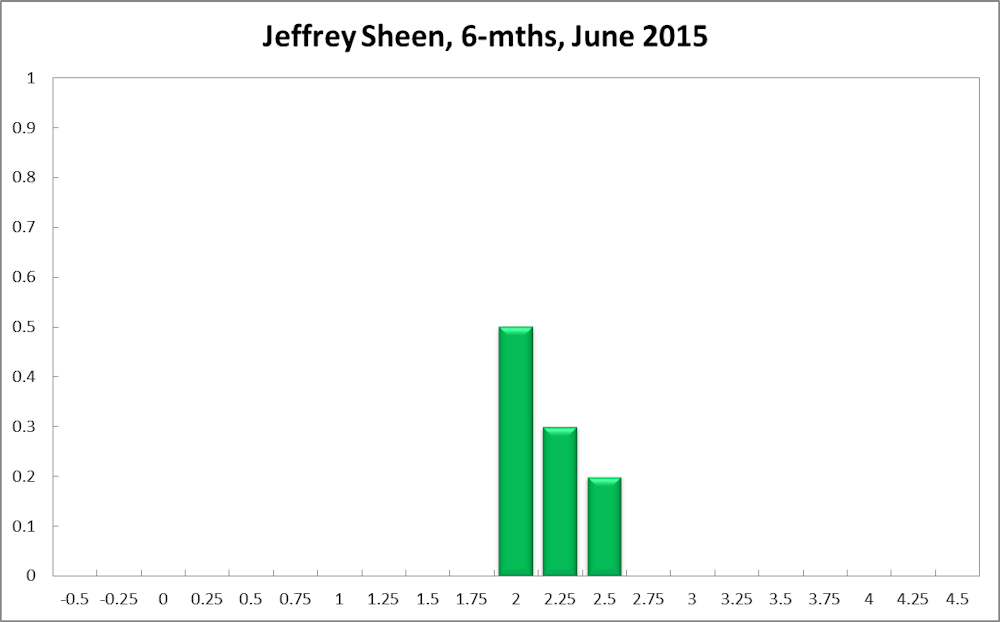

The probabilities at longer horizons are as follows: six months out, the estimated probability that the cash rate should remain at 2% equals 23%. The estimated need for an interest rate increase lies at 76%, while the need for a rate decrease is estimated at 3%.

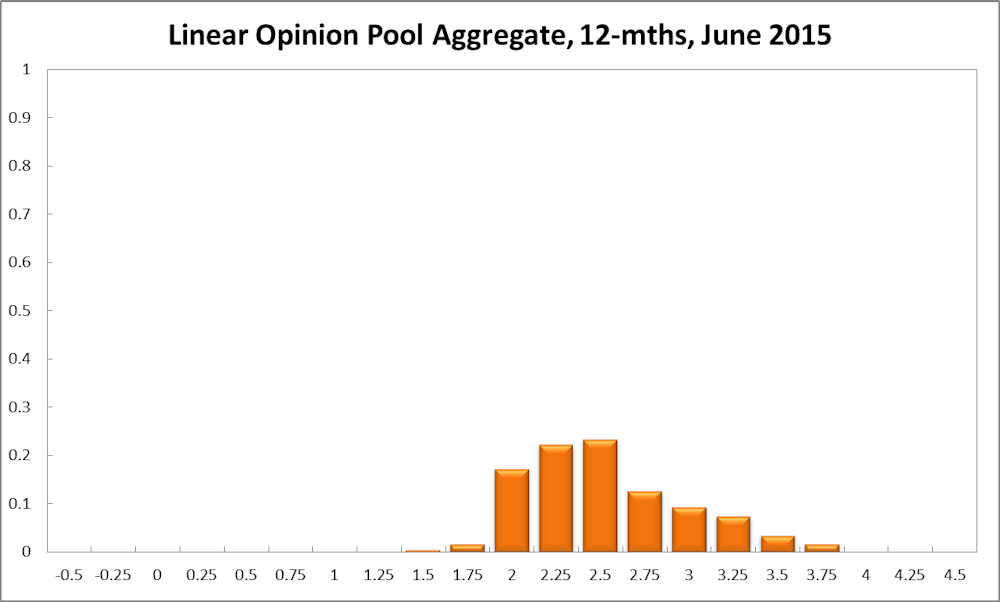

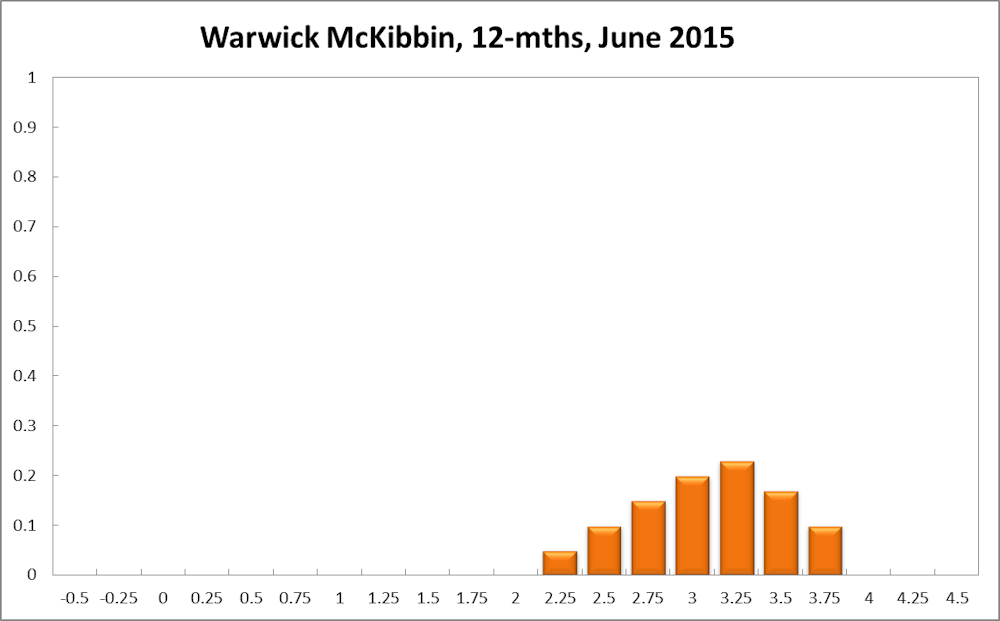

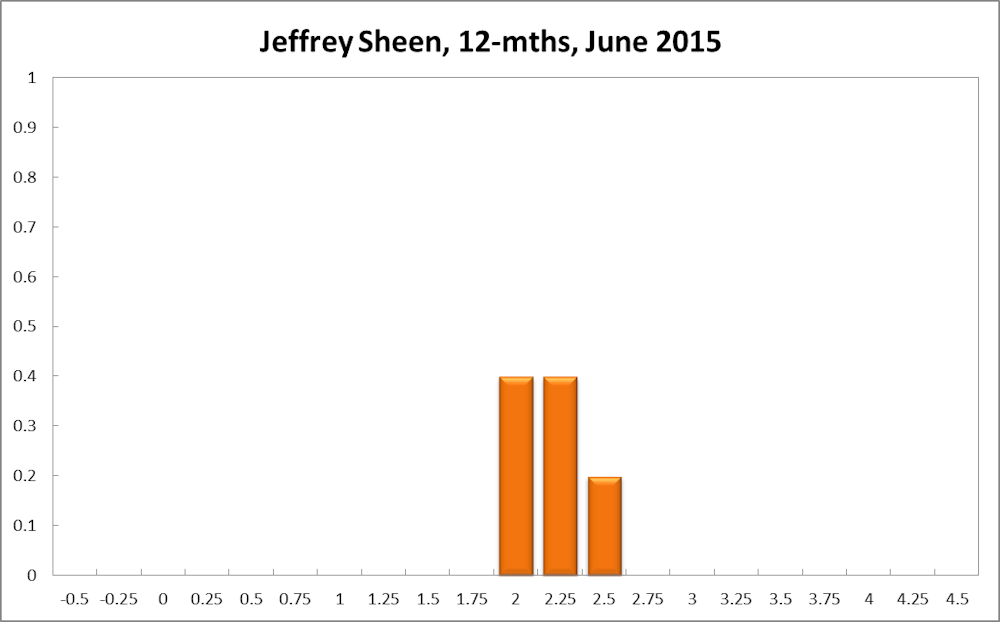

A year out, the Shadow Board members’ confidence in a required cash rate increase equals 81%, in a required cash rate decrease 2% and in a required hold of the cash rate 17%.

Comments from Shadow Reserve bank members

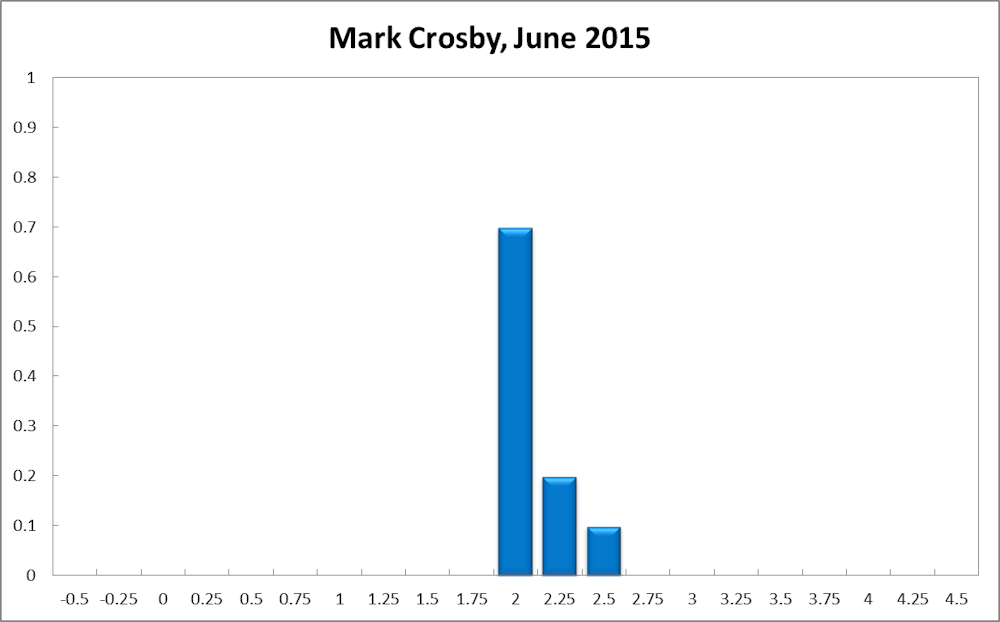

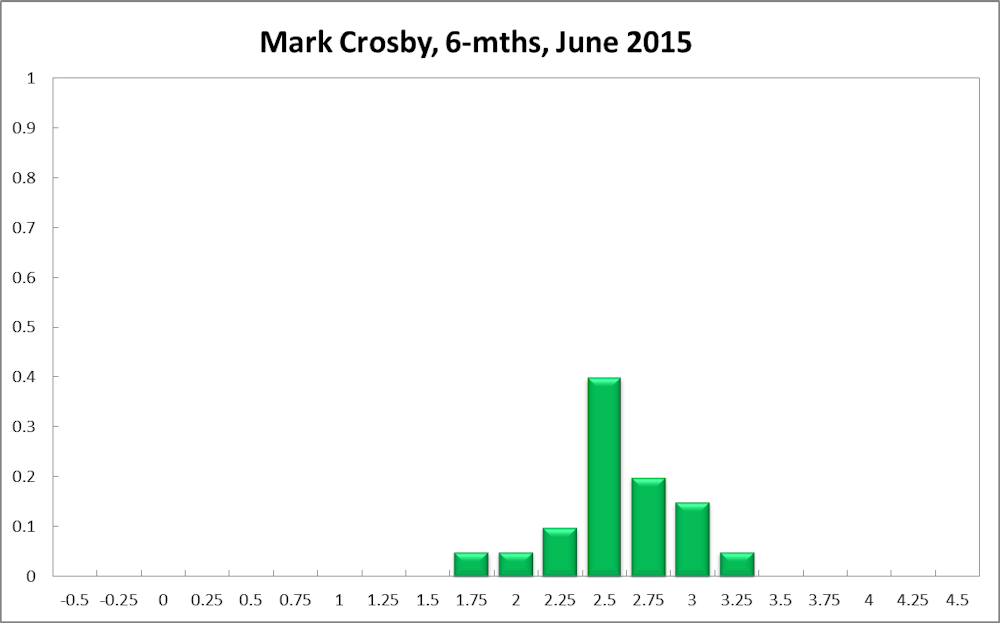

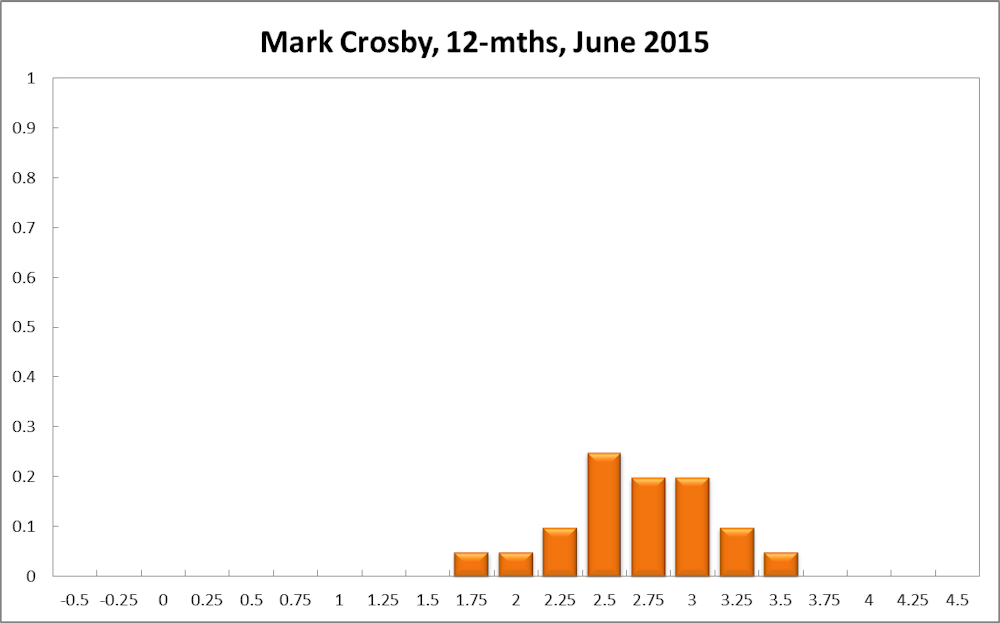

Mark Crosby, Associate Professor, Melbourne Business School:

“The case for a cut or cuts in the near future does not seem to be as strong as in past months.”

Further signs that the economy is not weakening further, so that the case for a cut or cuts in the near future does not seem to be as strong as in past months. Still uncertainty on the global front, with the ever present possibility that Greece may finally default. But does not seem that would have longer term effects on global economies. As a result the longer term outlook would be for a start towards rate normalisation within 12 months.

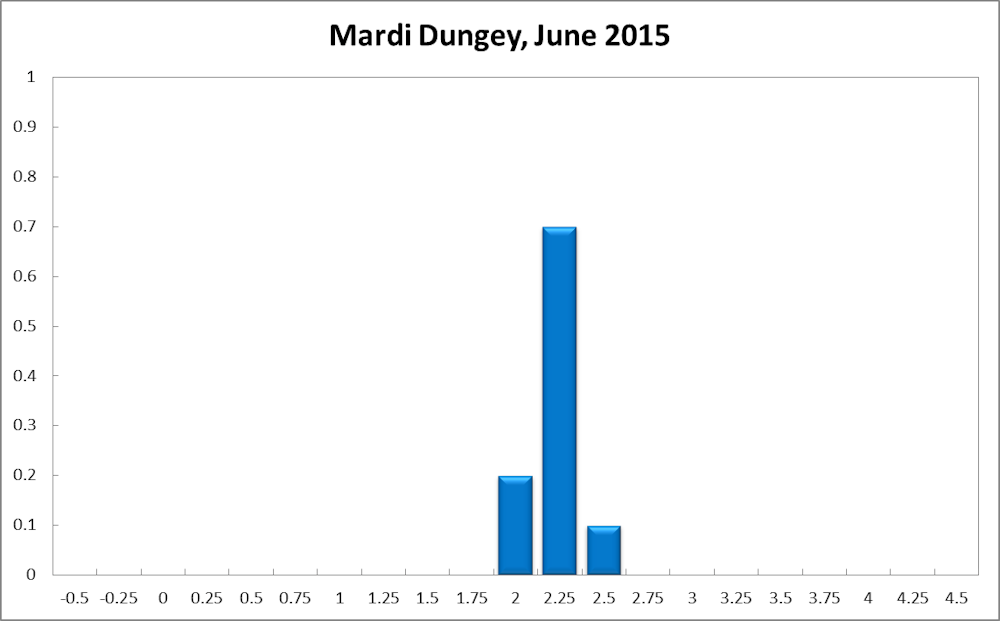

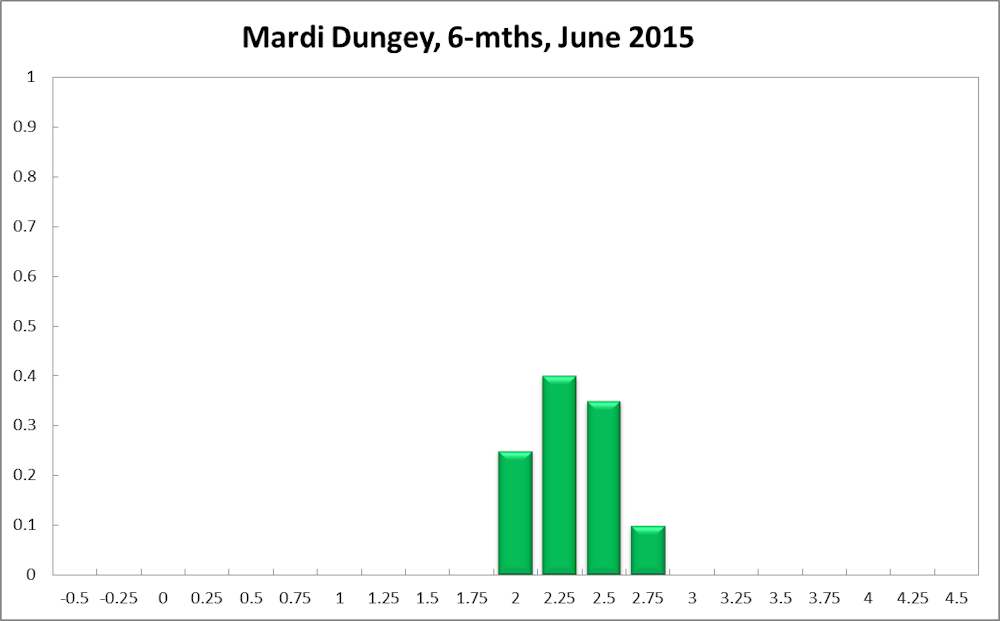

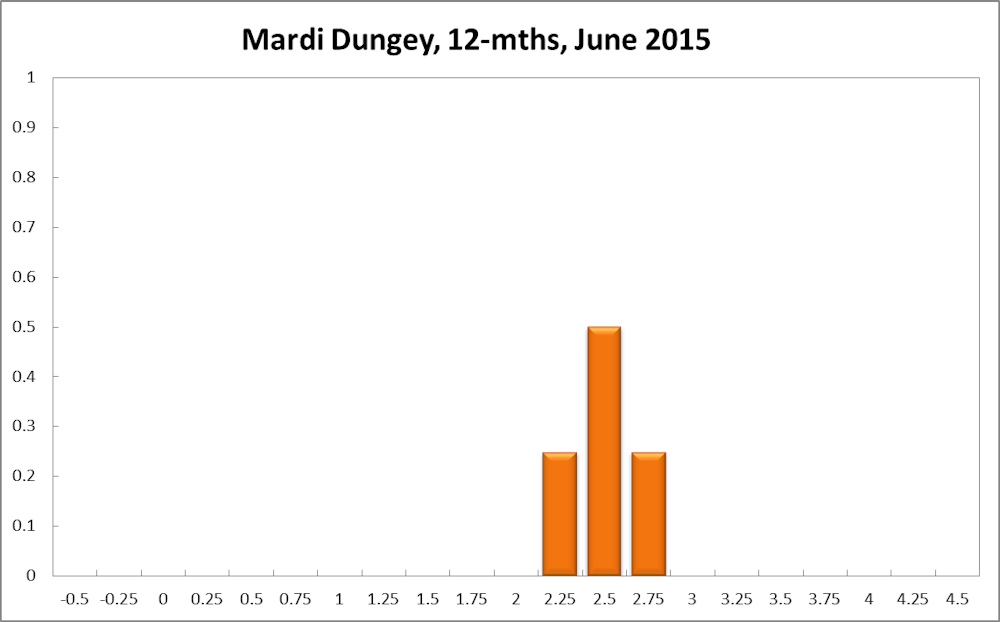

Mardi Dungey, Professor and Deputy Head, School of Economics and Finance at University of Tasmania:

“I recommend that a higher policy rate should have been maintained.”

The RBA’s decision to ease monetary policy in May - the timing of which was partly to meet the “challenges of communication” (RBA Minutes of Board Meeting for May 2015) associated with the timing of the Federal Budget - is a gamble that accommodative monetary policy can overcome the problems of the inactive role fiscal policy is currently playing in macro policy making. As there seem to be few signs of improvement on the fiscal front, the RBA is taking a risk that looser monetary policy can fill part of this role and not cause structural problems elsewhere.

The Board meeting minutes make clear that most domestic conditions are if anything only a little weaker than in previous months; and there is considerable uncertainty as to whether consumption will respond similarly to that experienced in pre-crisis conditions – given the rather nasty scare experienced by many in the economy, it seems unlikely we will seem this type of response to lower rates.

More likely is that looser credit will inflate house prices – an area where the fiscal reform agenda could make substantial improvements by removing a number of incentives to over-invest in housing. Given the hand that the RBA has been played, it is not unreasonable that they chose to move rates. However, if all arms of policy were playing a role in active economic management this would not be the path I would recommend.

For that reason, my recommendations are based on the presumption that monetary policy cannot reasonably be expected to manage single-handed and that it is able to follow its usual best-practice course in setting policy in partnership with other arms of policy making, in which case I recommend that a higher policy rate should have been maintained.

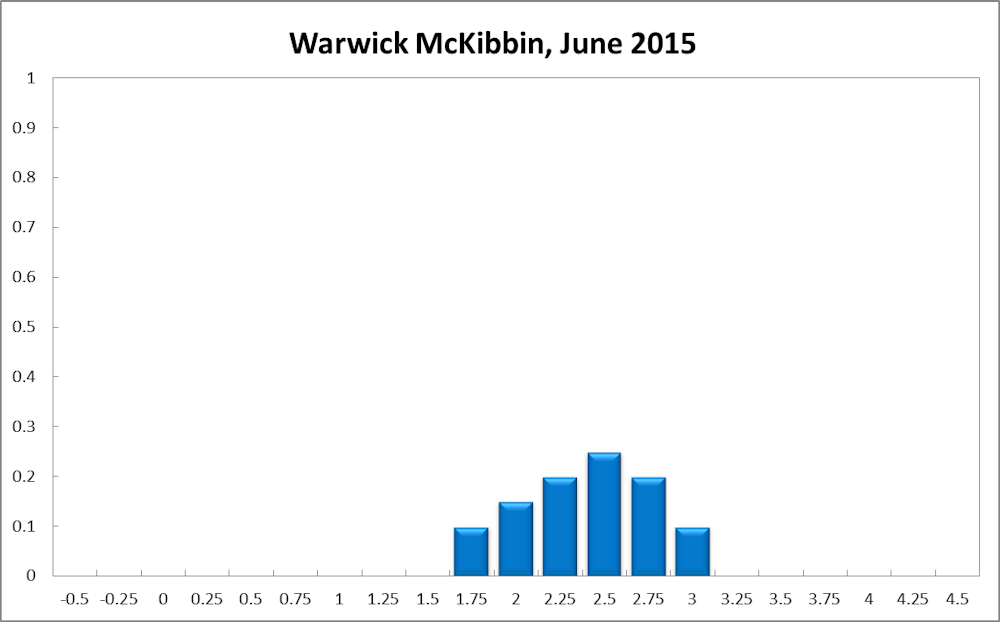

Warwick McKibbin, Chair in Public Policy, ANU Centre for Applied Macroeconomic Analysis (CAMA) , Crawford School of Public Policy at Australian National University:

“The distortion low interest rates is causing in asset markets is worsening.”

Continued weakness in nominal GDP growth in Australia implies that the neutral policy interest rate continues to fall. However, evidence of rising asset prices, particularly in the housing markets of Sydney and Melbourne, makes the setting of interest rates increasingly complex. From the point of view of short term macroeconomic factors, low interest rates in Australia could be justified; however, the distortion this is causing in asset markets is worsening.

This highlights the difficult trade-off between short term growth and medium term vulnerability. My judgement is that the damage caused by a painful adjustment in the housing market and the high levels of leverage by households in an environment of a downward adjustment in trend economic growth is a dangerous mix that loose monetary policy and even more financial leverage cannot solve. Add to this situation, the move to normalise interest rates in the US and there are many bad scenarios for Australia that are plausible.

I recommend leaving interest rates unchanged (indeed I would not have lowered them to the current level). Monetary policy should be focused on medium term stability especially if it has little prospect of solving the problems that cause weak short term demand. There is strong evidence that a point have been reached where monetary policy cannot offset the core problems caused by uncertainty about economic and political prospects in the Australian economy.

The lack of substantial policy assistance from fiscal rebalancing or substantive economic reform generally, is increasingly backing the Reserve Bank into a corner. It appears that many politicians do not appreciate the risks that now face the Australian economy. No wonder investment is weak and uncertainty is damaging economic prospects in Australia. It may be that the optimistic projections in the recent federal budget turn out to be correct, however, the vulnerabilities within the Australian economy are growing and lower interest rates without any other policy response makes this situation worse.

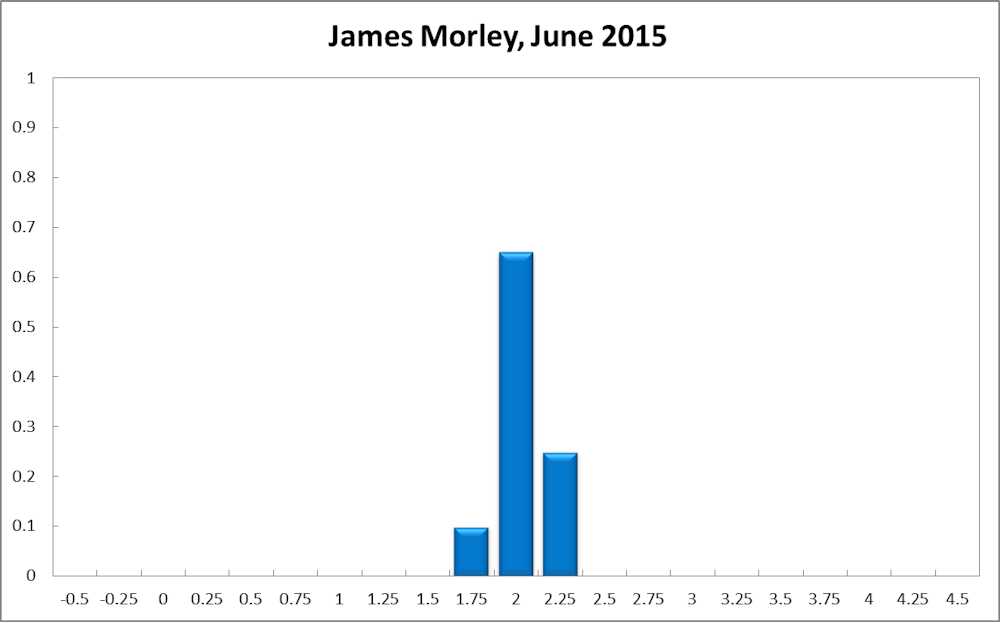

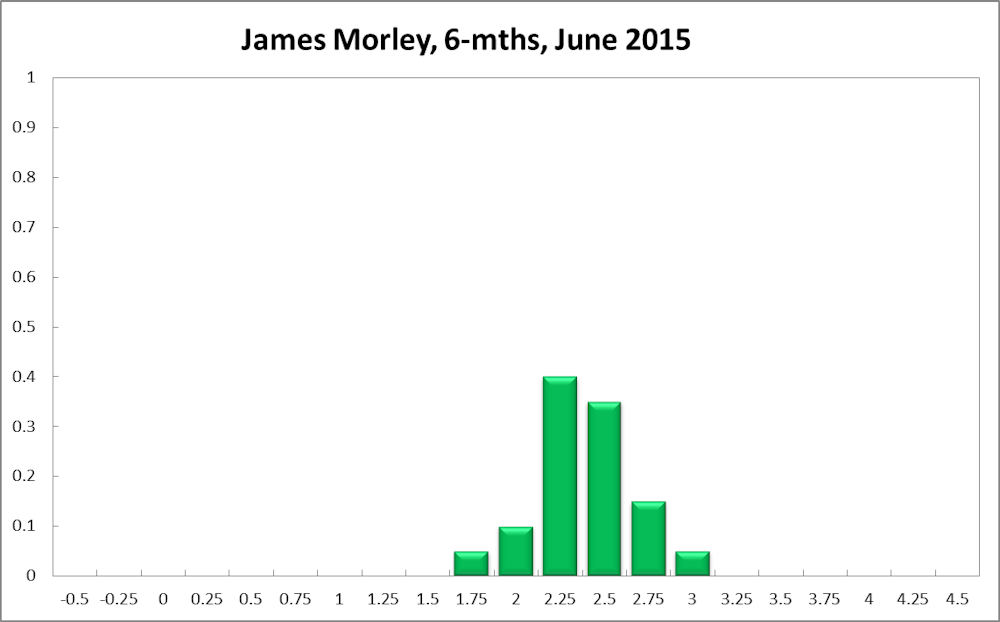

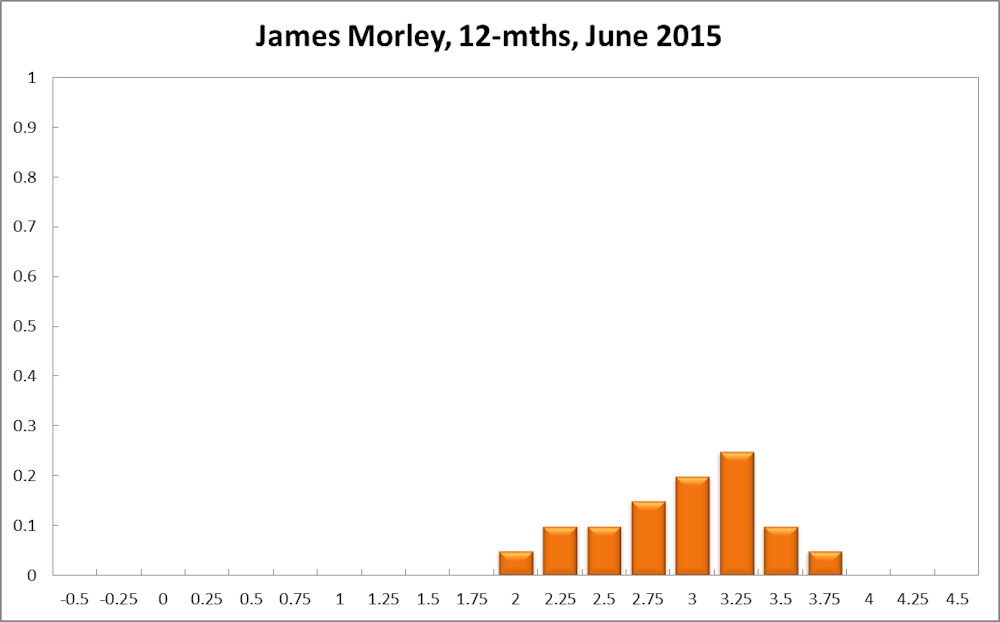

James Morley, Professor of Economics and Associate Dean (Research) at UNSW Australia Business School:

“The RBA has scope to hold the policy rate steady.”

The relatively stimulative federal budget and the recent lower level of the Australian dollar mean that the RBA has scope to hold the policy rate steady this month and even start raising it back to its neutral level over the medium term.

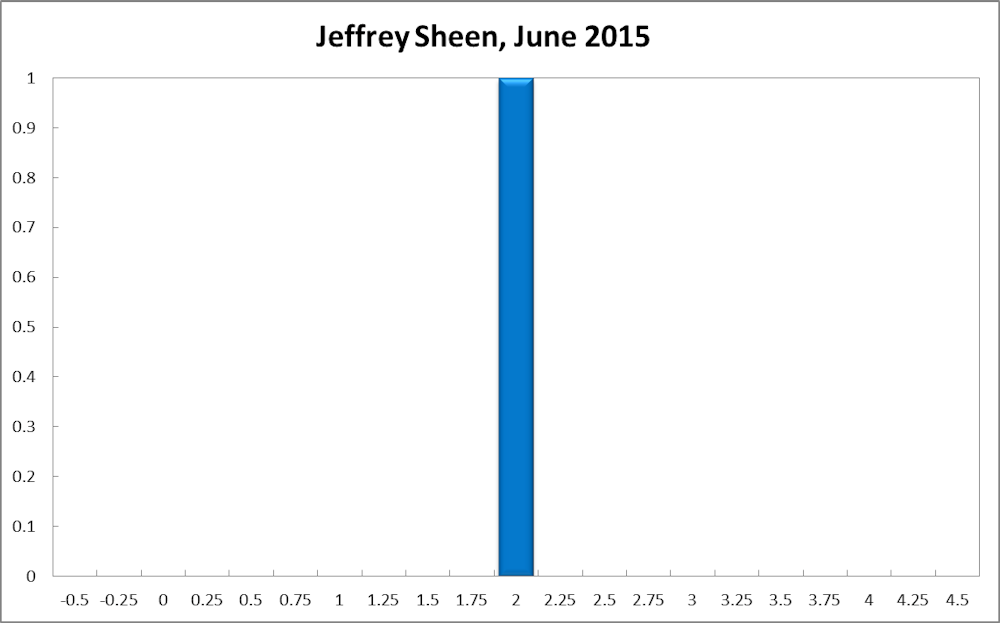

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“The cut in the cash rate to 2% in May was the right move.”

In my opinion, the cut in the cash rate to 2% in May was the right move. My expectation is that it should remain at this level until at least early 2016. The net saving glut in Australia continues to be a problem. Consumption growth is unlikely to contribute much to growth normalisation because of the relatively high levels of household debt. Growth recovery will have to come largely from business investment, which unfortunately shrank badly in the March quarter and continues surprisingly in waiting mode, despite low interest rates.

The proposed federal budget in May 2015 turned less austere than anticipated, reducing one obstacle to the return to normal growth. The 20% trade-weighted exchange rate depreciation over the last 24 months will help growth recovery by boosting non-mining exports, but this boost should continue for a while to be more than cancelled by the falling value of mining exports.

Overall, upside inflation risk remains minimal since wages growth is modest and energy prices are unlikely to rise much. The outlook for Greek debt negotiations looks grim, with possible negative ramifications for global asset markets. Therefore, the Australian economy needs its current monetary policy push to remain for some time yet, and needs a stronger fiscal push.