The Reserve Bank of Australia should leave the cash rate unchanged tomorrow, with little evidence suggesting an interest rate cut is justified, according to members of the CAMA Shadow Board.

The Shadow Board, which gives its views ahead of the decision by the Reserve Bank of Australia, has backed keeping the interest rate unchanged at 3.25%, with a 60% weighting from members.

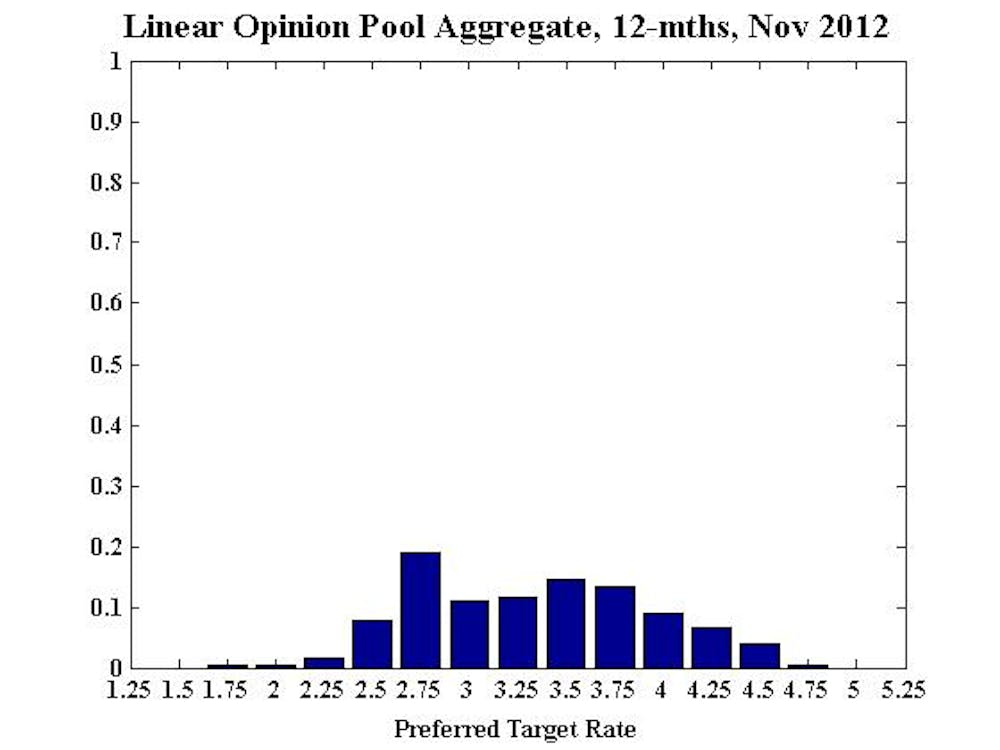

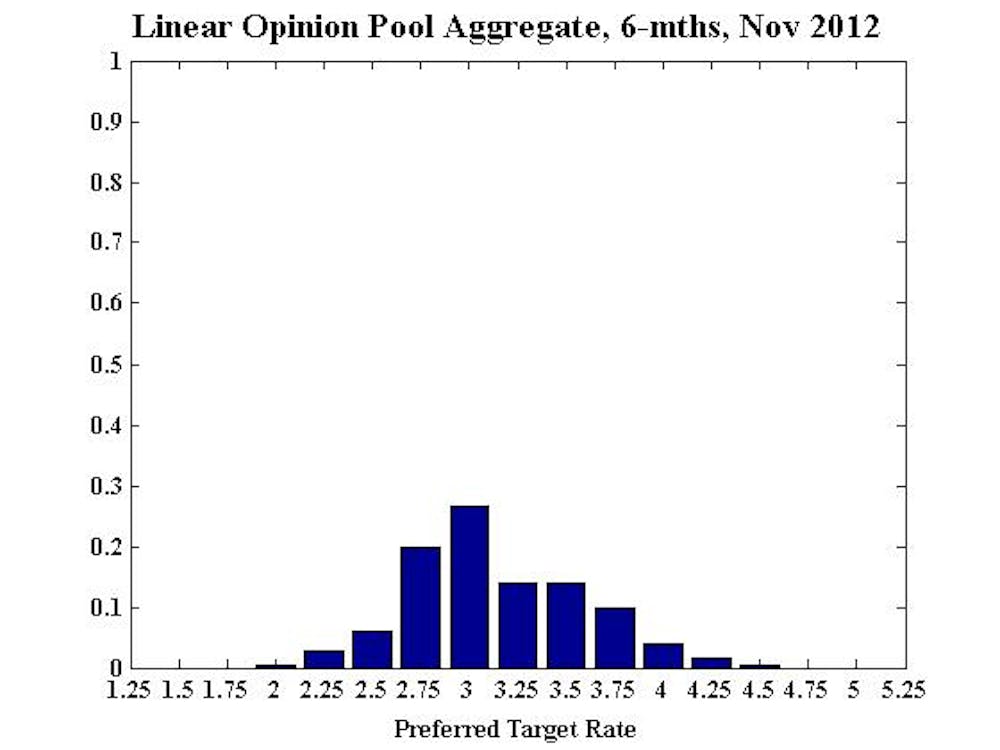

The Shadow Board sees evidence of weakening inflationary pressures in the medium-term. The most preferred setting for interest rates suggests a move to 3.00% within six months. But the risk that rates should be lower still is small, at around 30%.

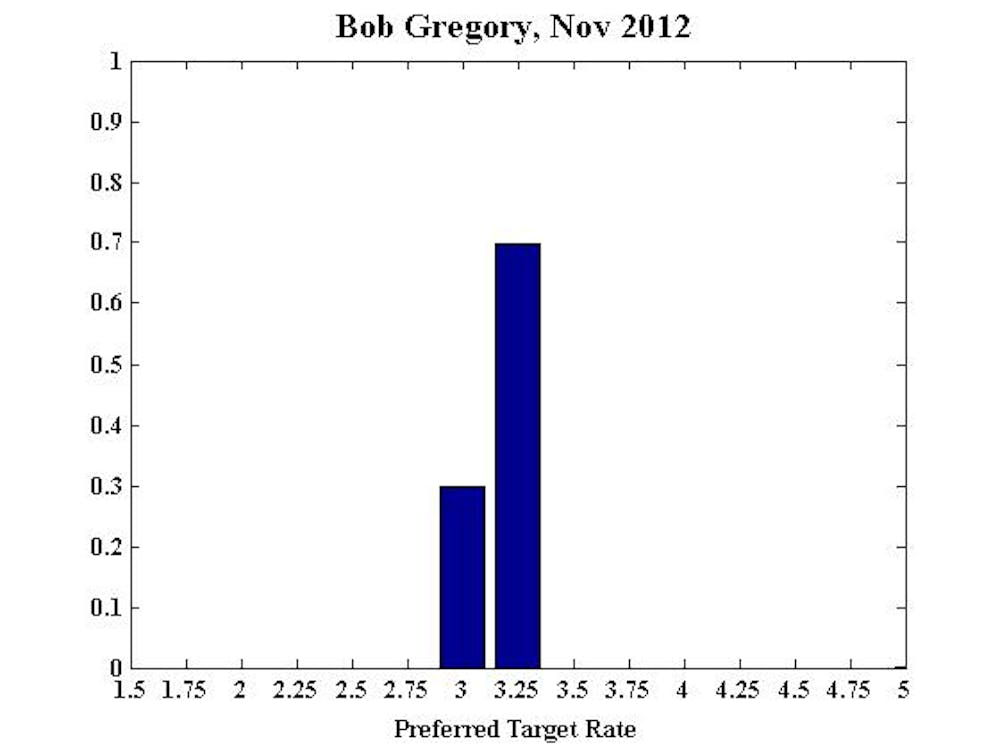

However, two shadow board members, ANU Professor Bob Gregory and Bank of America Chief Economist Saul Eslake both believe rates could be even lower in 12 months, backing a range of 2.50 to 2.75 basis points.

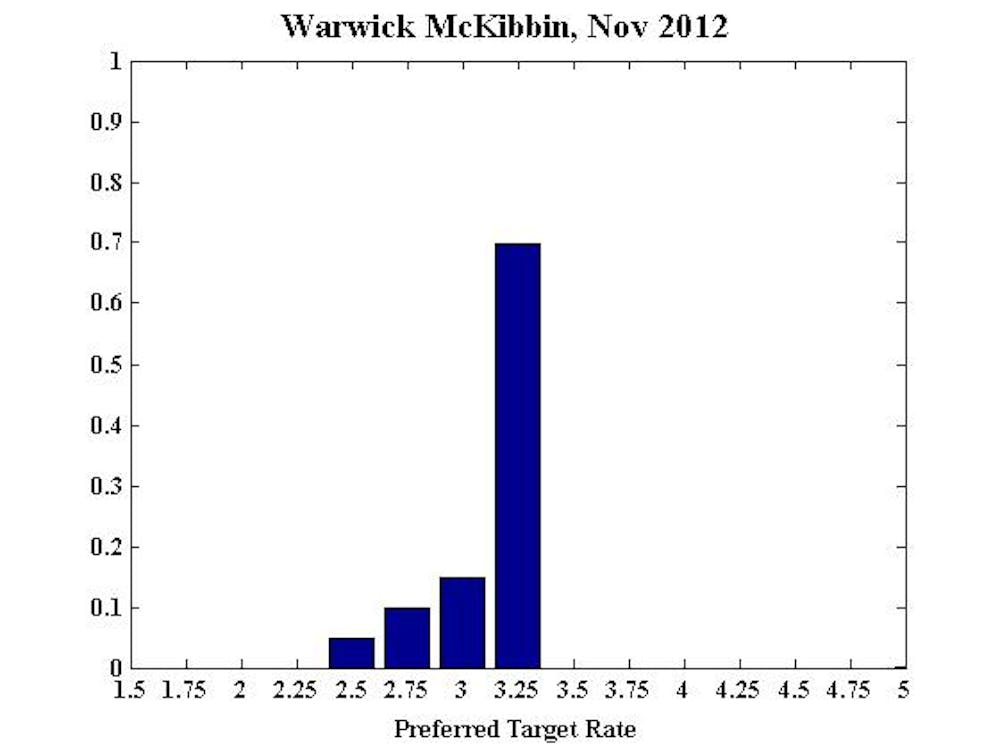

Professor Warwick McKibbin said there were the “beginnings of an inflationary impulse in the world economy” and some domestic inflationary pressures.

“No change in interest rates domestically would be prudent especially given ambiguous signals from various government ministers that the fiscal surplus may not be realised this financial year,” he said.

The Shadow Board is made up of influential economists from the private sector and academia. They are asked to rank their preferred outcomes for the cash rate.

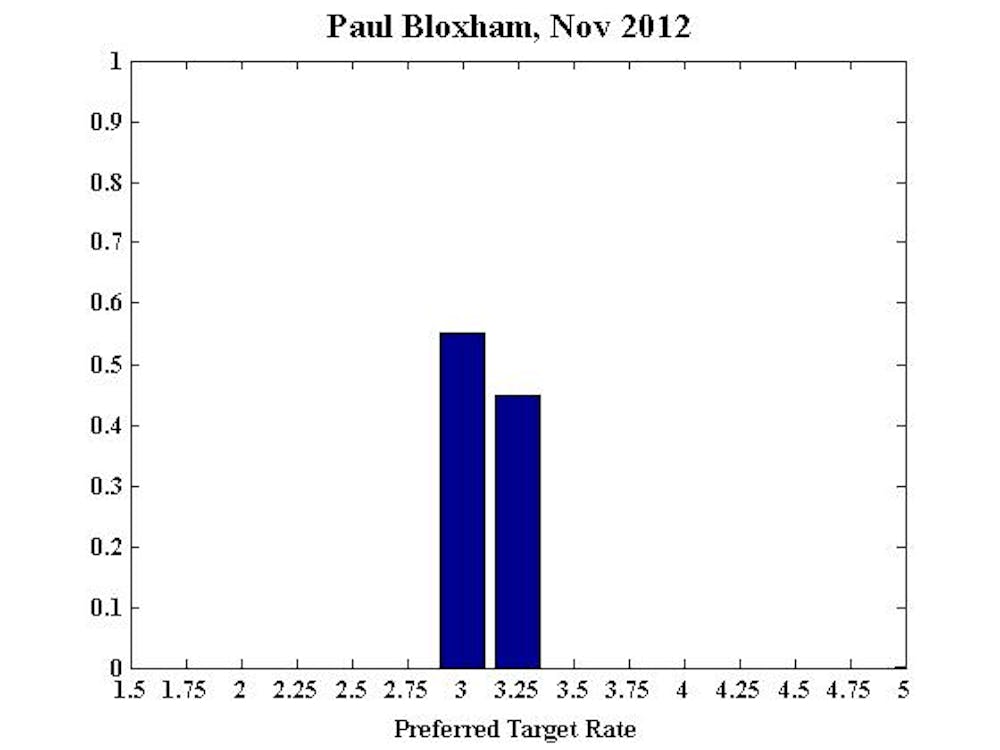

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

While inflation appears to have troughed, it is still low. At the same time the labour market is loosening, with the unemployment rate rising to a two and half year high of 5.4% in September.

Commodity prices have fallen, which is weighing on income growth, particularly as the Aussie dollar has stayed high. While there are tentative signs that the housing market is improving, the pick up has only been modest. The Board needs to be confident that policy is loose enough to see a smooth re-balancing from mining driven growth, to consumer and housing driven growth in 2013.

At this stage the risk of an unacceptably high rate of inflation seems low, while the risk that demand and the labour market weaken further has increased.

The Board could wait for further evidence about the extent to which the current below neutral interest rates are supporting demand in the economy, but with little risk of high inflation it may be prudent to cut rates a bit further this month.

Looking ahead, firmer global economic conditions and signs that Australian monetary policy is providing some support for the economy suggest it is becoming likely that the RBA are nearing the end of the easing phase of this cycle.

Also see Paul’s six month and 12 month projections.

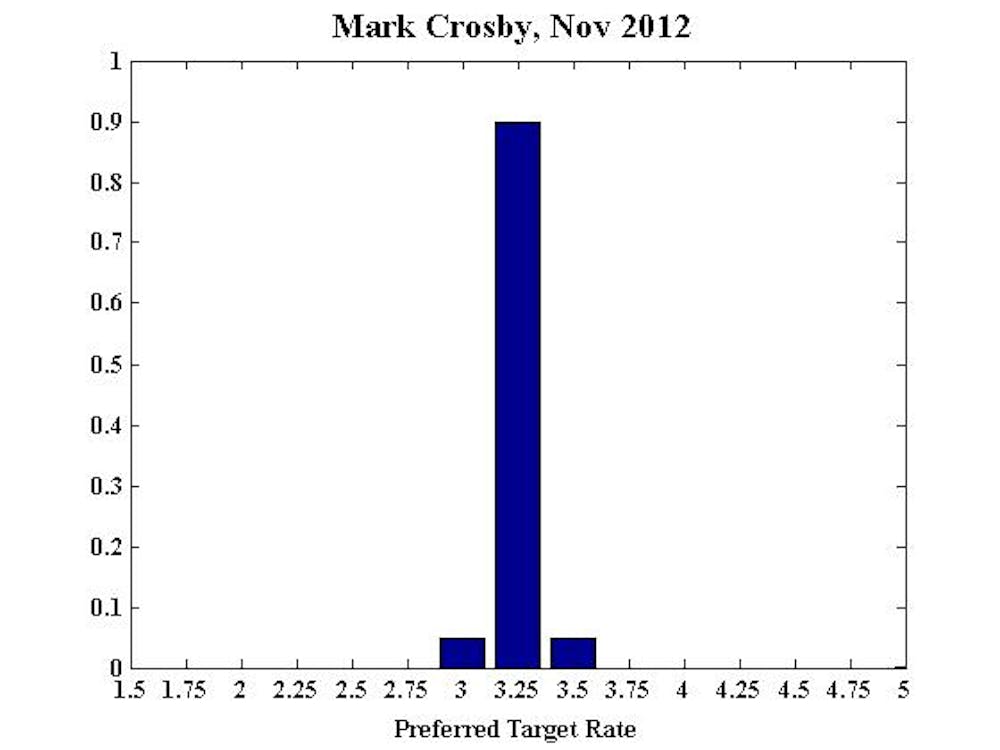

Mark Crosby, Dean of the Global MBA Program, Acting Dean of the Global BBA Program, and Professor of Economics, S P Jain Center of Management in Singapore:

Recent inflation numbers should see the RBA hold on Cup day. Ongoing uncertainty over fiscal outcomes in the US and Japan, and continued weakness in Europe are still a threat in the medium term, so that at the six to 12 month horizon it seems equally likely that the RBA should cut as increase rates in the face of domestic inflationary pressures.

Also see Mark’s six month and 12 month projections.

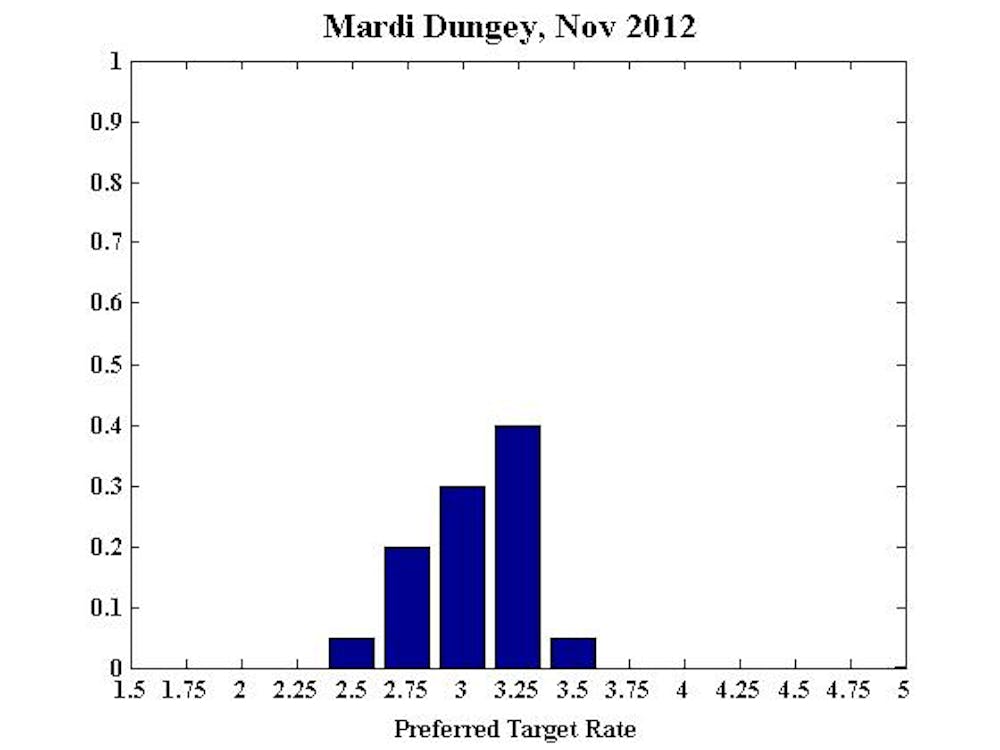

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA

In my view last month’s reduction in interest rates was welcome. There appears to be more widespread concern about the future health of the economy reported in the press, however, the outlook has not changed dramatically since last month, and it seems unlikely that there is a need for rapid action. On balance I slightly favour keeping rates the same for the next month over an immediate 25 basis point cut, but believe that the overall bias is downwards in the next quarter.

Also see Mardi’s six month and 12 month projections.

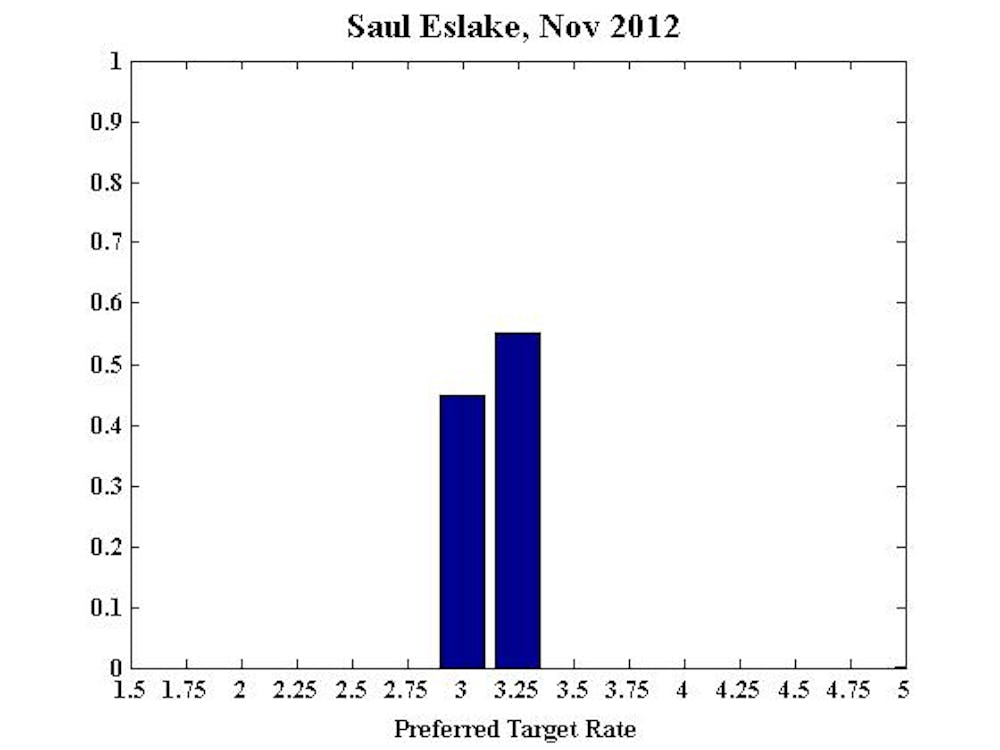

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia

No comment.

Also see Saul’s six month and 12 month projections.

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology

No comment.

Also see Bob’s six month and 12 month projections.

Warwick McKibbin, Professor, RSE, ANU, CAMA

Despite the problems in Europe and the looming fiscal cliff in the United States, there are still inflationary pressures in the Australian economy especially in the non-traded goods sector.

Continuing strength of the Australian dollar will help to offset the overall inflationary pressures through lower traded goods prices but there is the beginnings of an inflationary impulse in the world economy from the excessively loose monetary policy in the major industrialised economies.

No change in interest rates domestically would be prudent especially given ambiguous signals from various government ministers that the fiscal surplus may not be realised this financial year.

Also see Warwick’s six month and 12 month projections.

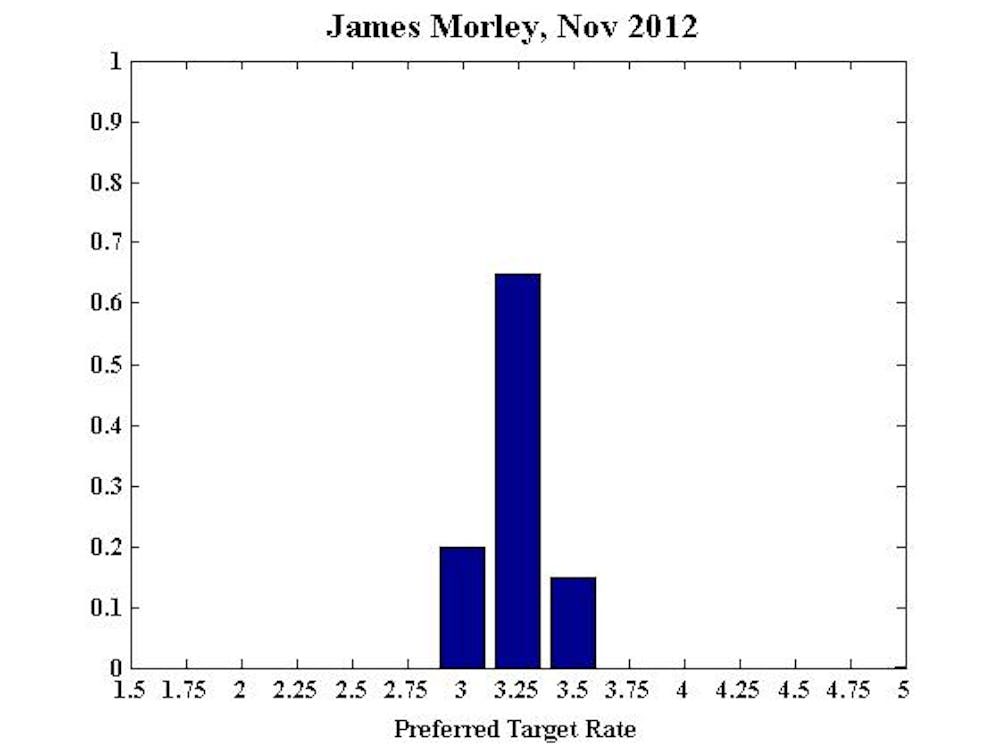

James Morley, Professor, University of New South Wales, CAMA:

On the domestic front, inflation has moved back up to its target range, as expected. However, the unemployment rate has also started to move up. On the international front, European and U.S. conditions have stabilized somewhat in recent months, although they are far from robust. Encouragingly, the outlook for growth in China has improved slightly.

Given recent cuts in the policy rate, monetary policy is loose, with the implicit real interest rate well below its neutral level. Thus, with low inflation and an uptick in the unemployment rate, the current stance is appropriate for the short term, with a slight easing bias in case the employment situation deteriorates further.

Also see James’s six month and 12 month projections.

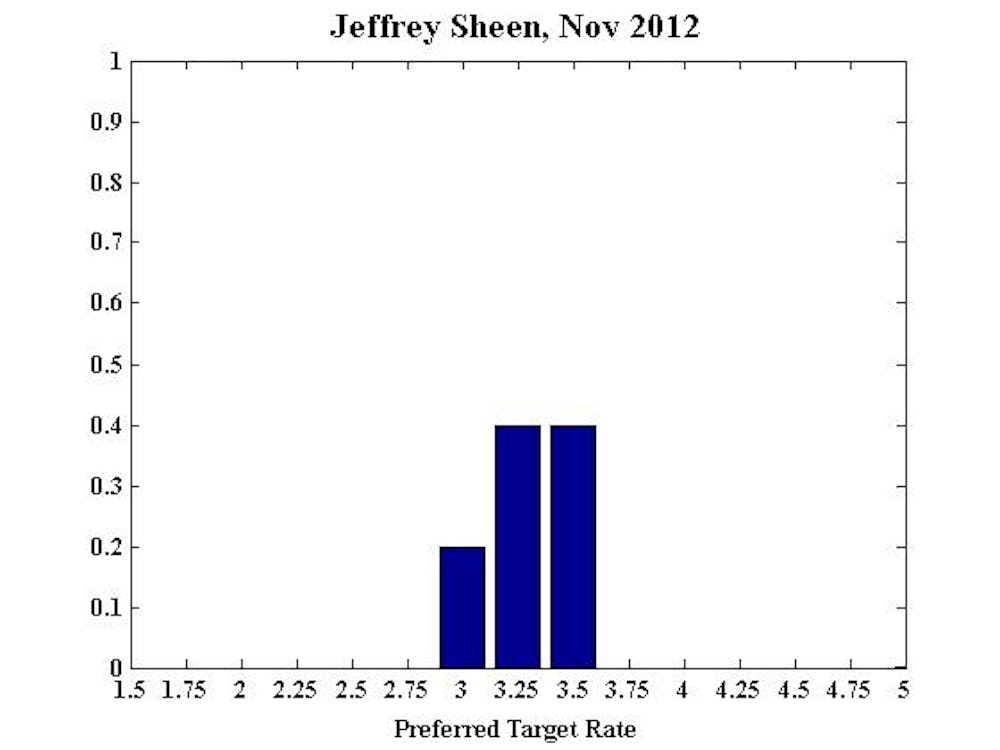

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

No comment.

Also see Jeffrey’s six month and 12 month projections.

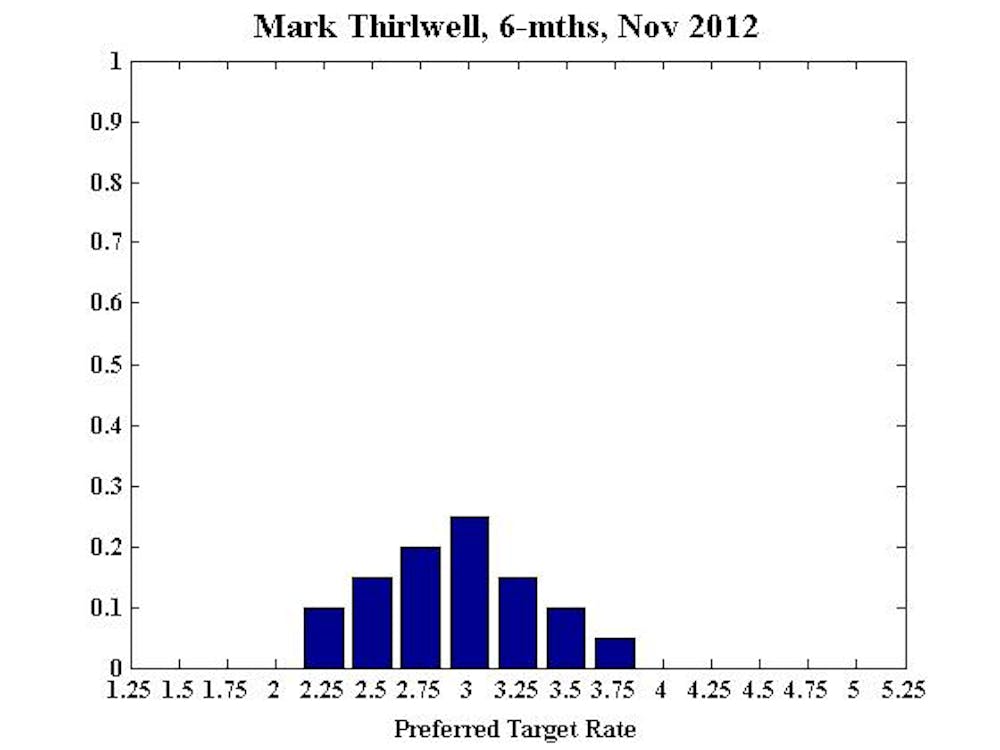

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy

No comment.