Nearly three-quarters of graduates will not clear their student loans before the end of the repayment period. This means the large majority of those who go to university aged 18 or 19 will still be paying off their loans well into their forties and early fifties.

The new higher education finance system, introduced in 2012, will leave graduates with much more debt than under the system it replaced. But graduates who do less well in the labour market will actually end up paying back less than before, while middle and especially high earners will pay back much more. In that sense, the system is more progressive than the one it replaced and looks, for most graduates, rather like a graduate tax.

A new report published by the Institute for Fiscal Studies, and funded by the Sutton Trust, examines the implications for graduates of the new student loan system that accompanied the higher tuition fees introduced in 2012.

These reforms increased the cap on undergraduate tuition fees for UK and EU students from £3,375 to £9,000 per year, while scrapping teaching grants paid by the government to universities for most students.

Students are entitled to borrow the full amount of these higher tuition fees – plus an additional means-tested amount to cover living costs – from the government. They repay this at a rate of 9% of the income they earn above a repayment threshold (increased from £15,795 under the old system to £21,000 under the new system). Any outstanding debt is forgiven after 30 years – extended from 25 years under the old system.

We find that students will, on average, now leave university with more than £44,000 in debt – £20,000 more than under the old system.

This means graduates will pay back an average of £35,446 in today’s prices, compared with £20,936 under the old system, an additional £14,510. Yet 73% of all graduates will not have repaid their debt in full by the end of the 30 year repayment period (at which point it is written off).

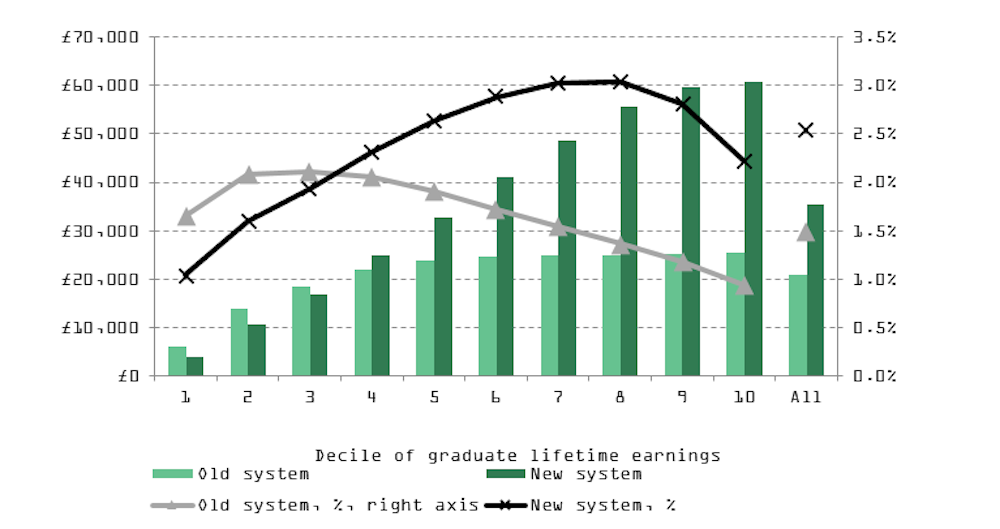

In part, this is because average annual repayments will be lower under the new system than under the old system, because of the higher threshold above which loans must now be repaid. The graph below splits graduates into ten equally sized groups (deciles) on the basis of their lifetime earnings. It shows that the 30% lowest earning graduates will, on average, pay back less in total under the new system than under the old one.

But because mid-to-higher-earning graduates (those from the fourth to the tenth deciles) will be repaying their loans for longer under the new system, they will end up repaying substantially more per year later on in their careers – after the point at which they would have repaid their loans in full under the old system.

For example, we estimate that a middle-earning graduate – someone whose annual earnings are higher than half of all graduates at each age (including those out of work) – would have cleared their debt by age 42 under the old system.

Under the new system, however, they will still owe around £38,000 in today’s prices at this age. This means that they will have to pay back around £1,500 a year (in today’s prices) throughout their forties and early fifties. They will still not have cleared their debt by the end of the 30 year repayment period, at which point they would have around £31,000 written off.

The increase in initial loans and reduction in the repayment threshold mean that graduates will now be making student loan repayments for substantially longer. On average, it will take graduates 28 years to clear their debt (by repayment or write-off), an increase from 19 years under the old system. Even among graduates who would repay in full, the average length to clear one’s debt increases from 16 to 22.5 years.

The new higher education finance system has secured an increase in resources for universities by increasing the contributions made by mid-to-higher earning graduates later in their careers. The system is more progressive than the one it replaced, but many graduates are still paying back substantially more than they did before. Whether you think these reforms are an improvement on the previous system depends on how you weight these different priorities.