_The Conversation, in conjunction with the Centre for Applied Macroeconomic Analysis (CAMA), will present the monthly findings of the Shadow Board, a day before the Reserve Bank of Australia Board meets to consider the official cash rate._

The Reserve Bank of Australia should keep the official cash rate steady at 3.5%, according to CAMA’s Shadow Board, which gives its views ahead of the decision by central bank’s actual board.

The Shadow Board is made up of influential economists from the private sector and academia.

They were asked to rank their preferred outcomes for the cash rate. Keeping the interest rate unchanged at 3.5% was given a 65% weighting, well above the next most popular, an increase to 3.75%, with a 19% weighting.

Support for a cut in the cash rate of 25 basis points or more received a 16% weighting.

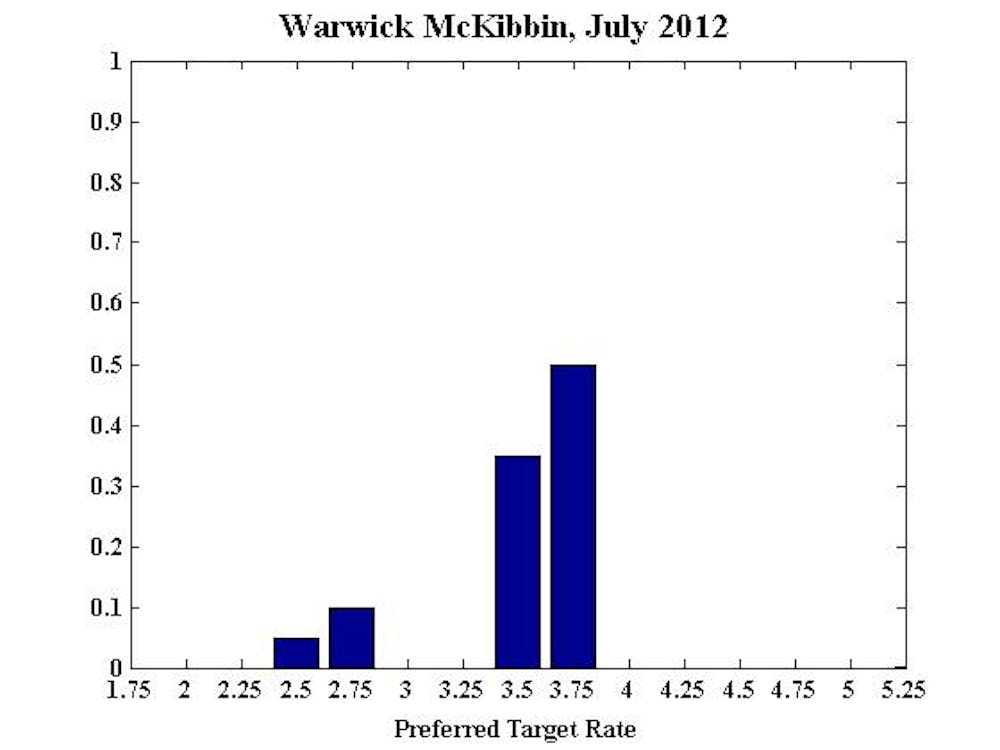

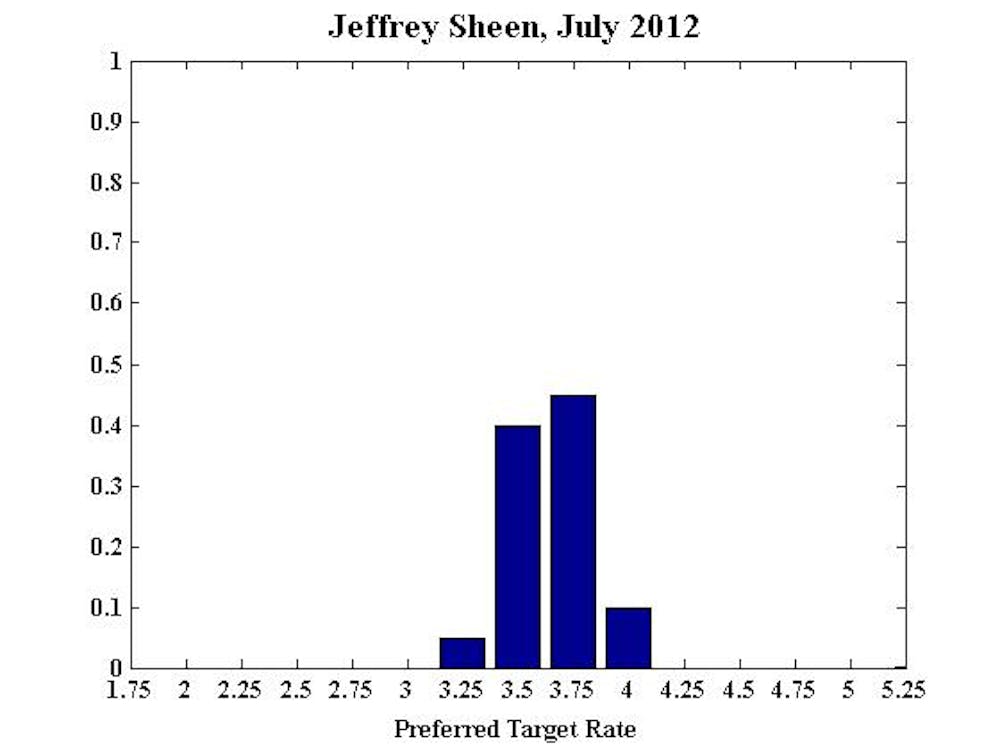

Professors Warwick McKibbin and Jeffrey Sheen were the strongest proponents of higher rates this month, with both indicating a most preferred outcome of 3.75%.

In the longer term, the CAMA Shadow Board see the risks to rates as equally balanced.

The probability that rates should be higher in 12 months is approximately equal to the probability that rates should be lower.

The comments by individual Shadow Board members can be obtained from the CAMA website and are reported below.

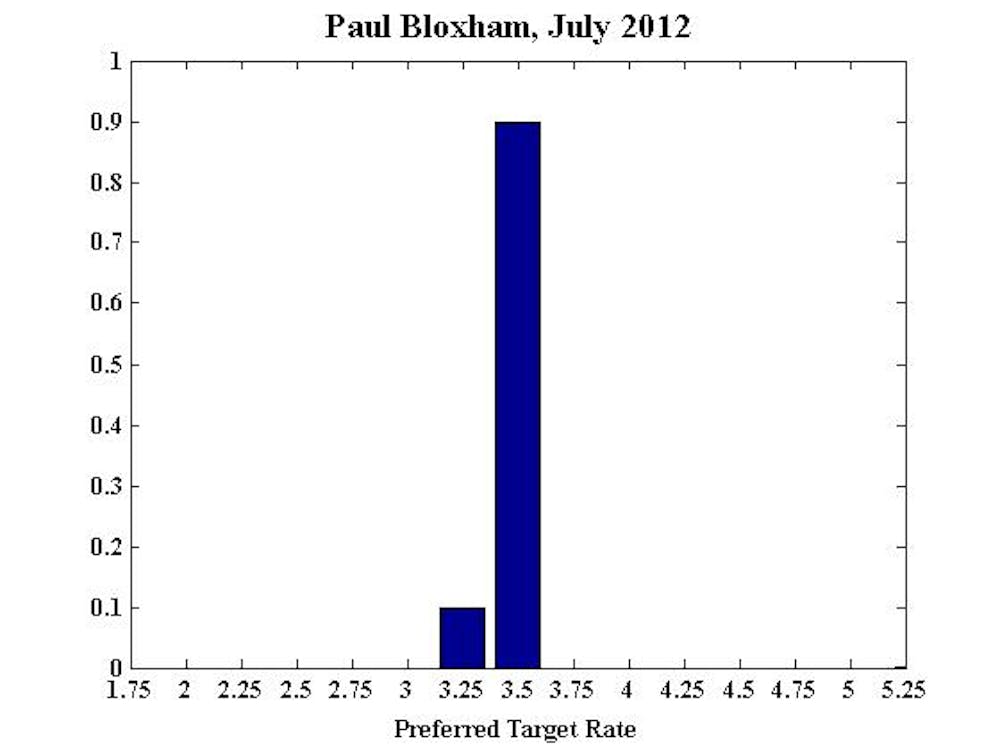

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

“I would recommend the RBA stay on hold this month. Having cut rates by a total of 75 basis points in the past two months, the RBA should now sit still to assess the impact that these rate cuts have had on the economy. Local conditions still look to be fairly solid, with employment growing strongly in May and GDP for Q1 an upside surprise.

"There is a clearly a risk that things have slowed down since then, with business and consumer surveys weakening, and the downside risks from abroad rising. But some part of this risk has already been accounted for in last month’s cut. Rates are now clearly stimulatory. With the AUD no longer appreciating, upside risks to inflation are also building. A discussion about cutting this month could be had around global risks, but I would not recommend a cut this month, having just gone last month.

"Looking further out, much is dependent on the global outlook. How the European debt crisis resolves is clearly key in this regard. Assuming the euro muddles through, with only a modest recession but no sharp financial shock, rates are likely to stay unchanged, or be cut only modestly from here in the next six months. In this fairly benign euro scenario, there would be an increasing chance that rates will need to be lifted over a twelve month horizon. If the euro situation deteriorates further, however, rates may need to be cut more aggressively.

"There are also risks due to the China slowdown, though these seem much less concerning at this point than those emanating from Europe.”

Also see Paul’s six month and 12 month projections.

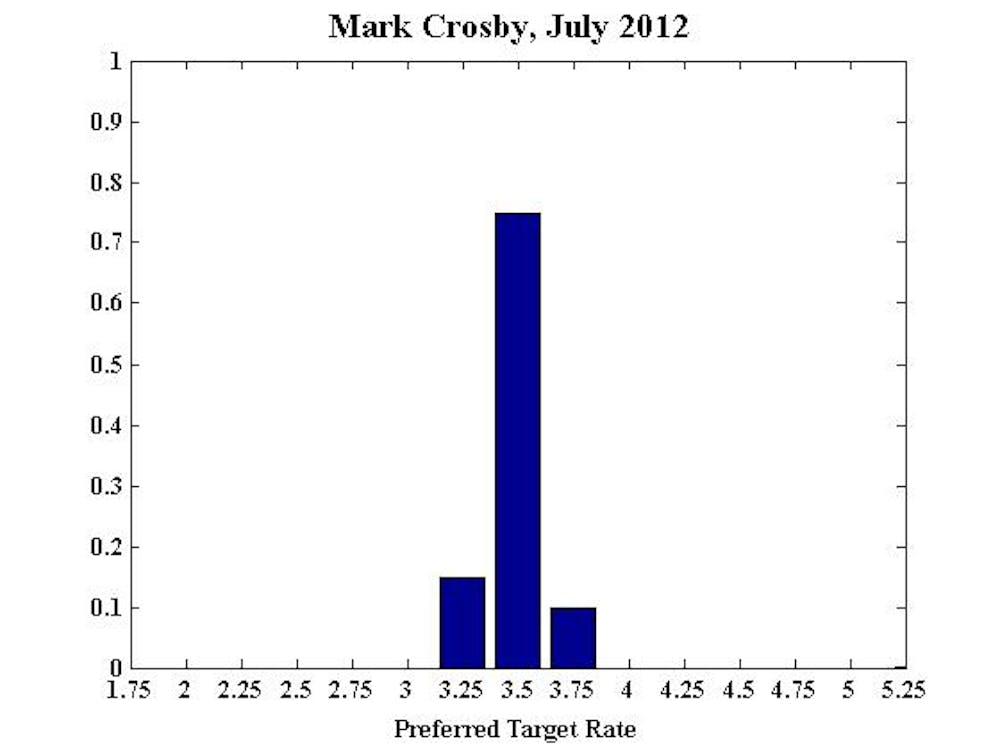

Mark Crosby, Dean of the Global MBA Program, Acting Dean of the Global BBA Program, and Professor of Economics, S P Jain Center of Management in Singapore:

No comment.

Also see Mark’s six month and 12 month projections.

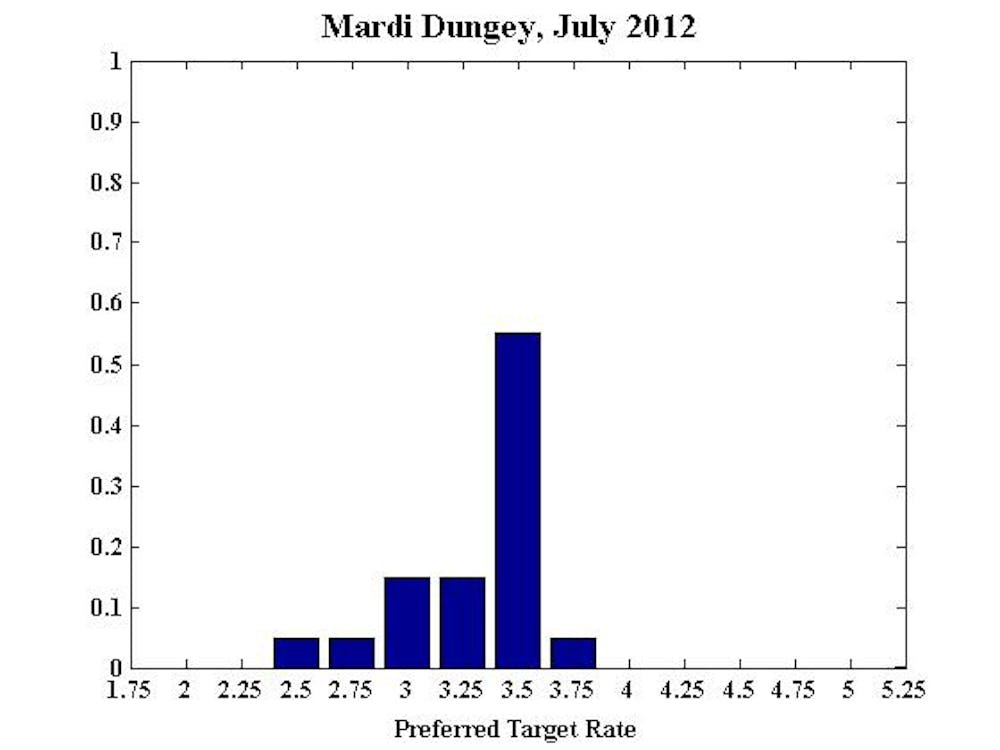

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA

No comment.

Also see Mardi’s six month and 12 month projections.

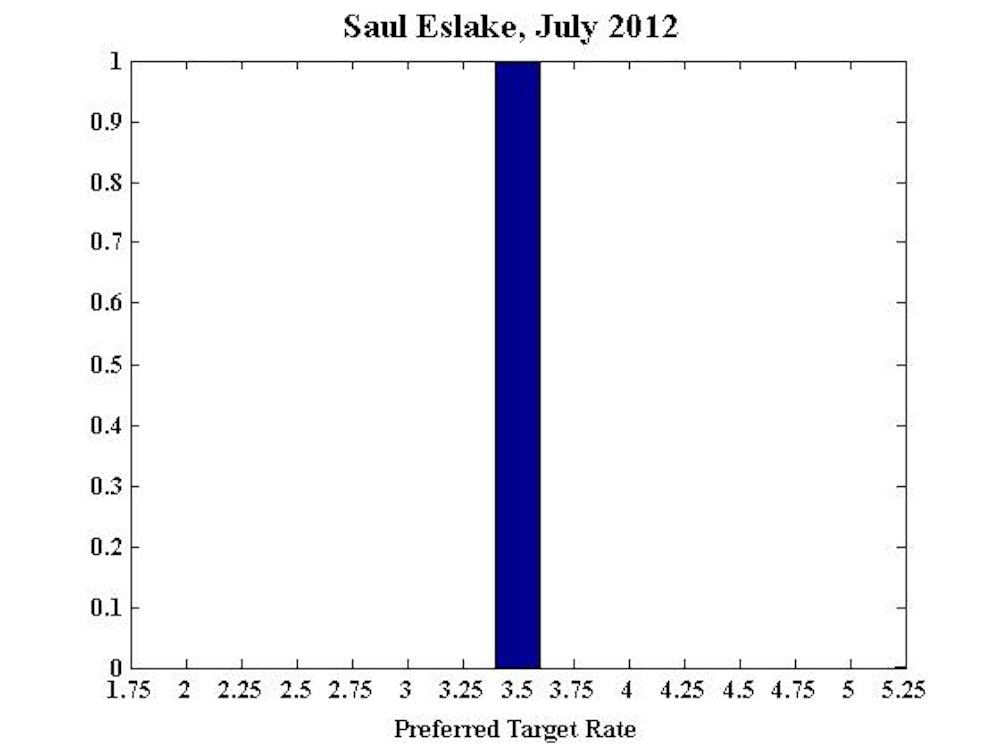

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia

“Noting that last month’s decision to cut rates was "finely balanced” (according to the minutes), and since then we’ve had the second Greek elections (the outcome of which has lowered the near-term probability of a disorderly Greek exit from the euro), and much stronger Q1 GDP and May labour force survey data, I think there’s zero chance that the RBA Board should do anything other than leave rates on hold at this week’s meeting.

“The six-month view (and my 12-month view) reflects a view that there are (broadly speaking) two plausible monetary policy scenarios - one, with 80% probability, that there isn’t another major global financial shock, and that the Australian economy slows from its Q1 pace (with unemployment riding towards 6%), prompting one (or possibly two) 25 basis points reductions in the cash rate; and a second, with 20% probability, that there is another major global financial shock, prompting a more aggressive easing from the RBA.”

Also see Saul’s six month and 12 month projections.

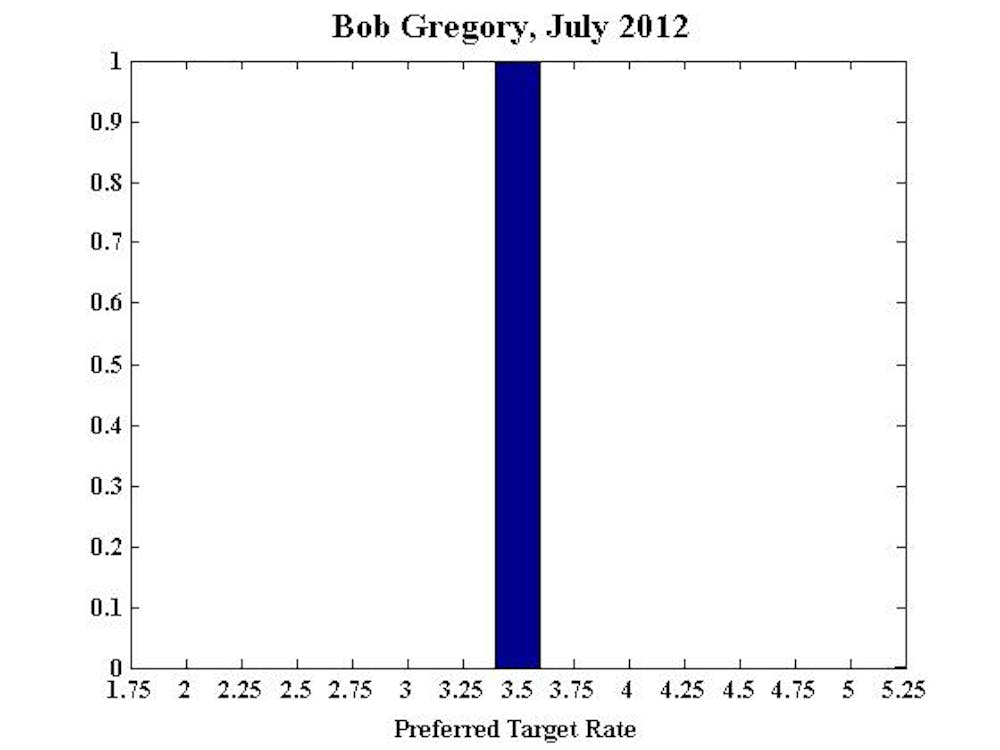

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology

No comment.

Also see Bob’s six month and 12 month projections.

Warwick McKibbin, Professor, RSE, ANU, CAMA

No comment.

Also see Warwick’s six month and 12 month projections.

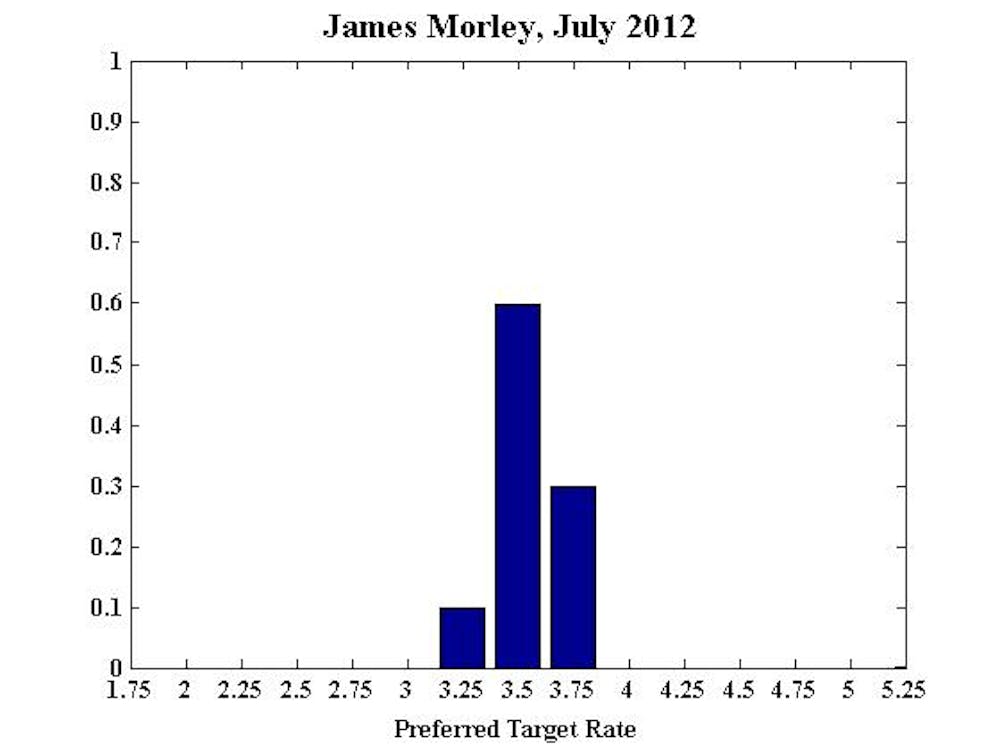

James Morley, Professor, University of New South Wales, CAMA:

“Slow adjustment back to neutral, but always ready for quick response to unusual developments in inflation or financial conditions:

"After cuts in the policy rate over the past few months, monetary policy is currently in an accommodative stance. This provides some insurance against any possible deterioration in the domestic economy or spillovers from continuing problems in the rest of the world. However, in the absence of a full-blown financial crisis in the Eurozone, the main focus of policy should be on the appropriate timing to return to a more neutral stance over the next six to twelve months. This timing will depend in part on the inflation outlook, with the current outlook allowing for a fairly gradual adjustment.

"As always, monetary policy should be ready to respond immediately to a new global financial crisis. But it should not do so pre-emptively unless the likelihood of a full-blown crisis rises substantially before the next policy meeting.”

Also see James’ six month and 12 month projections.

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“The cash rate was cut last month, which was a move that I did not support, but does constrain what I recommend now. Since then, the March quarter national accounts data have come out, showing real GDP growth at 4.3%, well above normal.

"This may well be revised downward later, but not by enough to justify any further pessimism about the overall Australian economy. The source of expenditure growth was not only (mining) investment, but also consumption, which broadens the base for the recovery. In addition, employment growth (particularly, full-time) in May was positive, as was participation (which actually meant unemployment rose a little, but is still very low).

Though the trend growth and level of productivity remains a concern, this is not something monetary policy can properly address. Global risks have declined following the outcome of the Greek election, and then the agreement by European leaders to allow direct recapitalisation of troubled banks and to encourage stimulus policies as well as a closer economic union in the longer run. Disaster would seem to be averted, but its hard to see ailing Europe as anything but the new Japan in the medium term.”

Also see Jeffrey’s six month and 12 month projections.

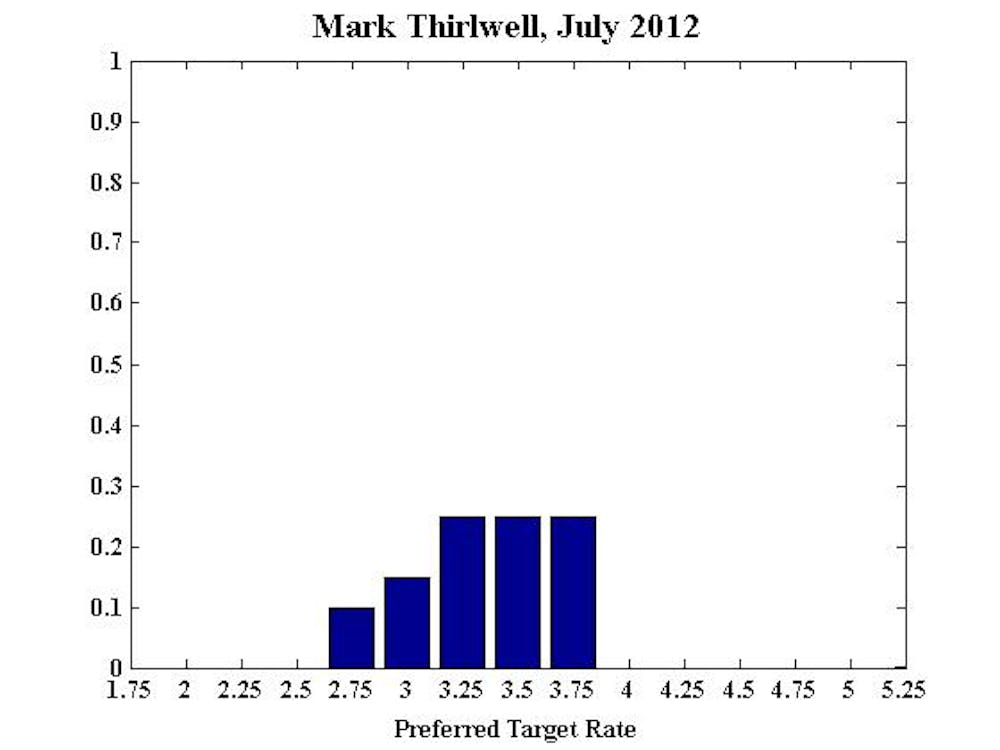

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy

No comment.