The Abbott government’s deal with the Palmer United Party to freeze the minimum superannuation contribution rate at 9.5% until 2021 will not only cost retirees, it will also see future governments forced to bear the brunt of an increased reliance on the Age Pension.

There has been considerable discussion of the impacts of the deal on both the wages of workers and their retirement savings. However, asserted effects have been either speculative (in the case of wages) or limited to a few hypothetical examples (in the case of retirement savings).

In work undertaken as part of a collaboration between researchers at The University of Melbourne and professional services firm Towers Watson, we have combined nationally representative household survey data derived from the HILDA Survey with an adaptation of the ASIC Moneysmart retirement planner to project Australians’ retirement savings and living standards in retirement. In doing so, we are able to model the effects of the delay in the super guarantee increases on the entire Australian population.

Retiring with less

Our projections show the delay has a relatively small, but nonetheless negative, overall effect on the future adequacy of the retirement savings of Australians.

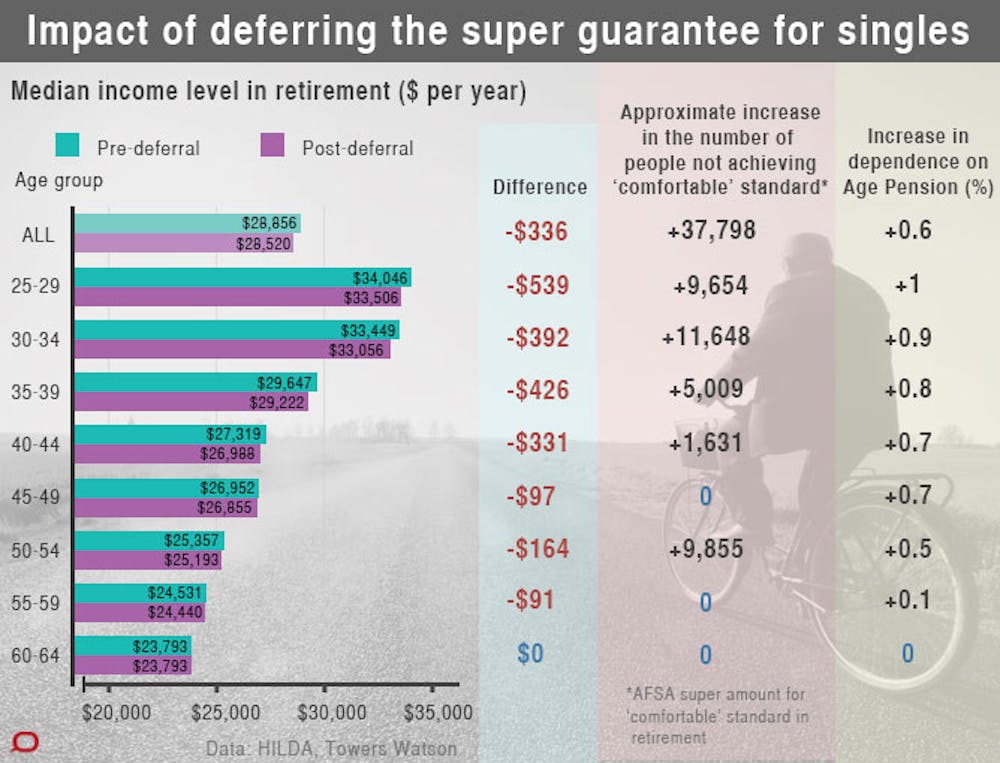

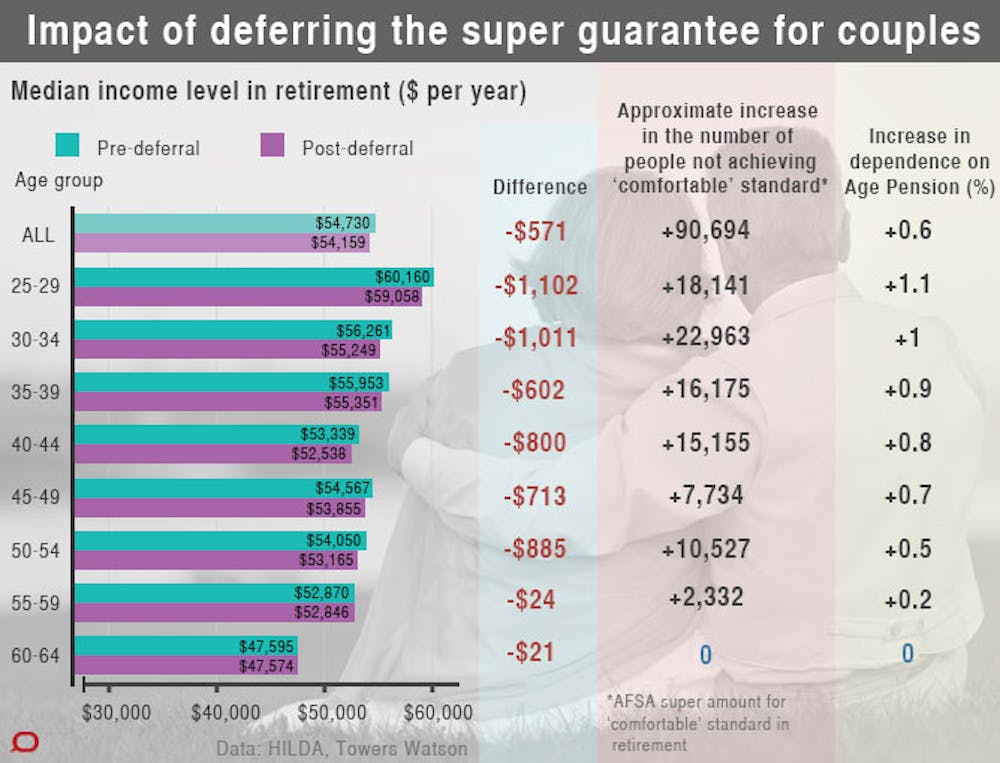

On average, in today’s dollars, superannuation balances at age 65 are projected to be A$8,598 lower for single people and A$20,790 lower for couples. These numbers translate into a decrease in annual retirement income of about 1.1%. As a result, an additional 1% of the population aged 25 to 64 are projected to have a living standard lower than the Association of Superannuation Funds in Australia (ASFA) Retirement Standard for a comfortable lifestyle (currently A$58,128 per year for couples and A$42,433 for singles).

Adverse effects are generally largest for people currently under the age of 40. The effects also tend to be larger in absolute terms for middle-to-high-income individuals, reflecting the fact that, even absent the policy change, low-income people are projected to largely rely on the Age Pension. Overall, singles tend to be affected more than couples.

Prior to the Palmer deal, the guarantee was scheduled to increase to 10% on 1 July 2015 and reach 12% on 1 July 2019 (although some delay in the guarantee increases had already been announced in this year’s budget). The new policy therefore represents a six-year deferral of the increases.

While the base impact of the changes is not large, it should be viewed within the broader context that 75% of single people currently aged 25-64, and 46% of couples currently aged 25-64, were already projected to fail to achieve a comfortable living standard in retirement.

The negative effects of the delay in the increase in the super guarantee rate will be magnified once the Age Pension age is raised to 70 and the pension is indexed to prices rather than wages, as proposed by the Abbott government as part of the last budget. In this environment, accumulating a sufficient level of private savings prior to retirement will become crucial for retirees.

Of course, individuals are free to make their own additional provisions for retirement — including voluntary superannuation contributions. Our projections assume individuals do not respond to the guarantee delay by increasing their voluntary contributions, or otherwise increasing their saving — yet rational, forward-looking individuals would be expected to do just that (which would in fact mean that the super guarantee itself is redundant).

But the overwhelming evidence, both in Australia and in other developed countries, is that people consistently fail to save enough for retirement and, moreover, that mandatory retirement saving, such as is achieved by the super guarantee, has few adverse effects on voluntary saving. As a consequence, mandatory retirement savings accounts are quite effective at increasing self-reliance in retirement, and more effective than other measures currently known.

A multi-billion dollar impost on future governments

Notwithstanding the proposed changes to the Age Pension, the deferral of the super guarantee increases will also increase demands on the Age Pension, as lower private savings are likely to translate into higher dependence on the pension.

Our projections show an increase in the mean proportion of retirement income drawn from the Age Pension of 0.6 percentage points, which is likely to translate to many billions of dollars in increased pension payments over future years.

The super guarantee deferral will, however, improve the short-term net fiscal position, largely because a reduced fraction of personal income will be taxed at the concessional rate applied to superannuation contributions. The deferral therefore represents an improvement in the fiscal position over the period covered by the forward estimates at the expense of the longer-term fiscal position. While it is very difficult to quantify the magnitudes of these effects, there can be little doubt that they are sizeable.

How much is required?

So how much do you need to retire comfortably, and what superannuation contribution rate is required to achieve that? According to the Moneysmart retirement planner, a home-owner couple retiring today aged 65, and expected to live to 86, requires approximately A$570,000 in superannuation (and other savings) to achieve the ASFA comfortable living standard for the duration of their retirement. A single person requires approximately A$480,000.

Importantly, however, the Age Pension makes a substantial contribution to retirement income at these superannuation balances, so the minimum required balance is sensitive to future Age Pension policy settings.

For people not yet retired, the contribution rate needed to achieve a given superannuation balance will depend on the level of earnings, the length of working life, and the returns achieved by the fund manager (net of fees). This — in conjunction with uncertainty about future pension policy — means there is no single “golden number” for the super guarantee rate. What is clear, however, is that less than half the population is likely to achieve the ASFA comfortable standard under current policy settings. So, for most Australians, saving less is probably not a good idea.

John Burnett and Nicholas Wilkinson from Towers Watson contributed to this article.