The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set. Timo Henckel is the non-voting chair of the board.

Australia’s economic outlook has not moved much since last month. Growth remains slightly below trend and inflation well contained within the official target band. Weakening commodity prices, a pickup in domestic production, slowing growth in China and Europe and geopolitical uncertainty suggest the most appropriate action is for interest rates to stay on hold.

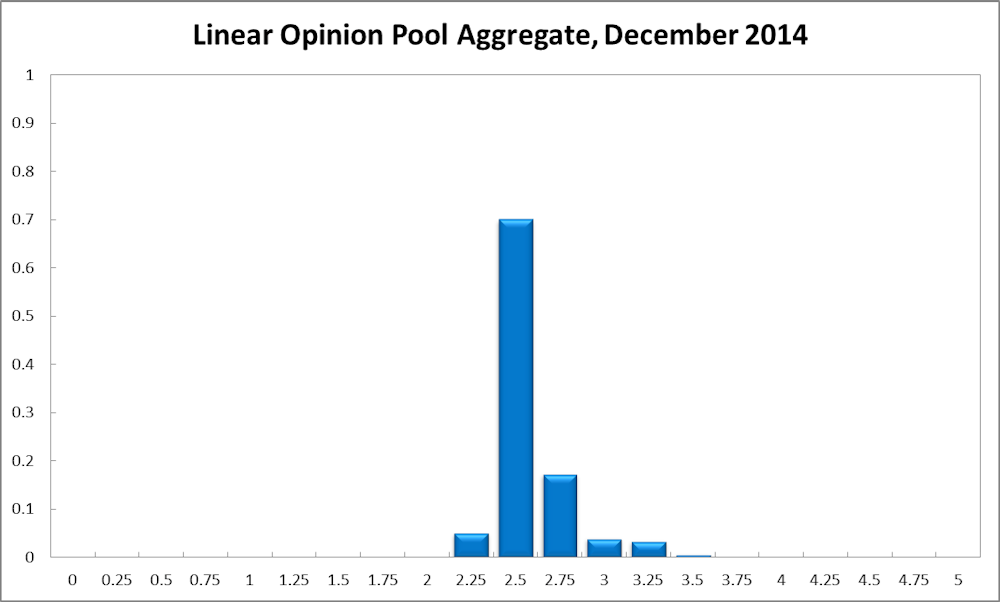

The CAMA RBA Shadow Board continues to recommend with confidence that the cash rate remain at its current level. The Board attaches a 70% probability that the cash rate ought to remain at 2.5% in December. The confidence attached to a required rate cut equals 5%, while the confidence in a required rate hike has increased to 25%.

There is no new data on headline inflation since the previous quarter when it fell 2.3%, largely driven by a fall in electricity prices. Sustained weakness in global energy prices will maintain downward pressure on domestic inflation.

The Australian dollar continues to hover around the 85 US¢ mark, a value many economists consider reflects fundamentals. If domestic interest rates have indeed bottomed out and demand picks up, the Aussie dollar may strengthen a little. Further softening of commodity prices may in turn lead to a continuing decline of the currency.

The Australian Bureau of Statistics’ most recent revision puts the unemployment rate at 6.2%. The employment-to-population ratio has dropped to 60.6%, the lowest it has been since late 2004. Without significant improvement of the labour market on the horizon, wages growth is likely to remain muted.

Business investment in capital goods, which includes buildings and equipment, rose 0.2% in the September quarter, well above economists’ expectations of a fall of up to 2%. This suggests that the Australian economy is successfully rebalancing as the mining boom wanes. This rebalancing is reflected in the shift of economic fortunes from the mining states to populous NSW and Victoria, with Sydney’s economy growing more than twice as fast in the last financial year (4.3%) as all other capital cities.

Other business indicators are mixed. Capacity utilisation increased slightly to 80.43% in October, as did the manufacturing PMI (from 46.47 in September to 49.42 in October). On the other hand, the Services PMI has fallen from 45.50 to 43.60 in October and the NAB monthly survey of business confidence has slipped slightly from 5 to 4. The Westpac-Melbourne Institute Leading Index of Economic Activity remained steady.

The outlook for the global economy is similar to the previous month’s. Europe, including Germany, risks a major recession while growth of China’s economy is modest. Better news is coming from the USA; however, with the Republicans taking control of Congress in this month’s midterm elections, President Obama will face fierce opposition, giving little hope for any serious structural reforms. The situation in Eastern Ukraine remains highly unstable and Western efforts to combat ISIS in Iraq and Syria continue to pose serious threats to any recovery of the world economy.

What the CAMA Shadow Board believes

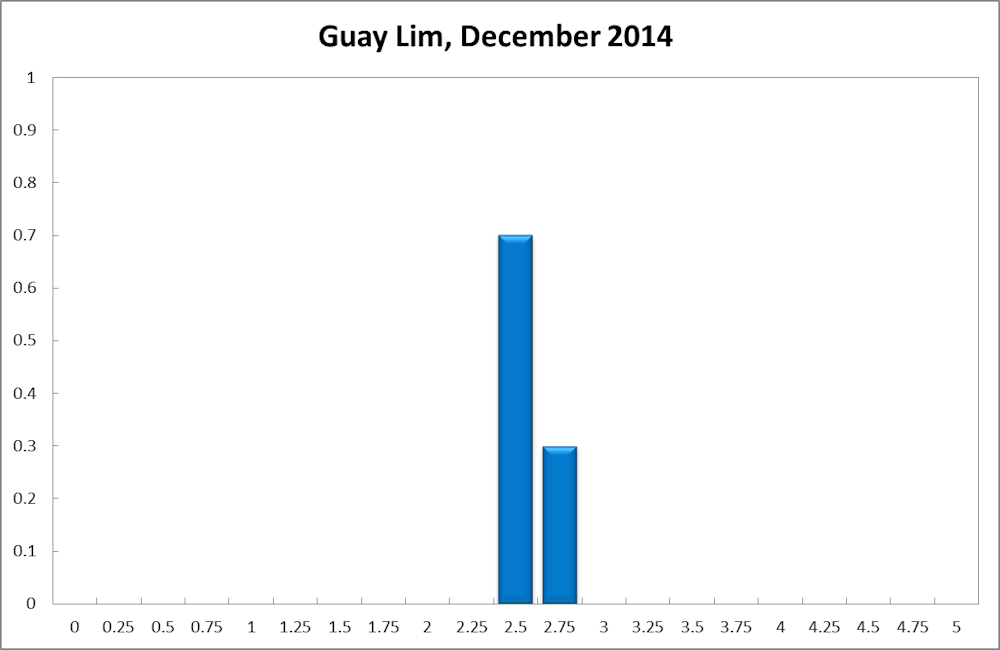

The consensus to keep the cash rate at 2.5% remains virtually unchanged at 70%. The probability attached to a required rate cut equals 5% (6% in October) while the probability of a required rate hike has risen slightly to 25% (23% in October).

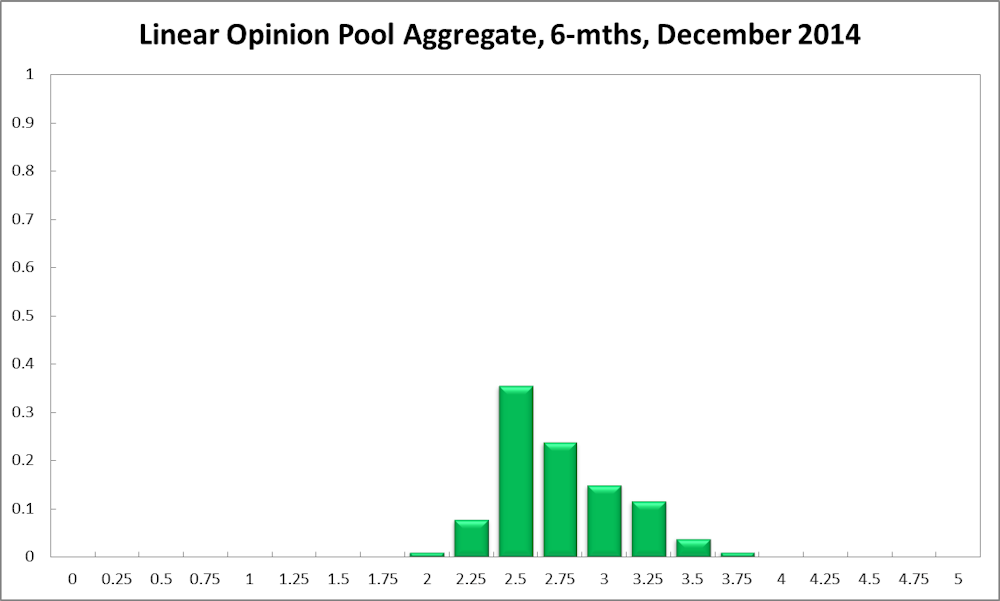

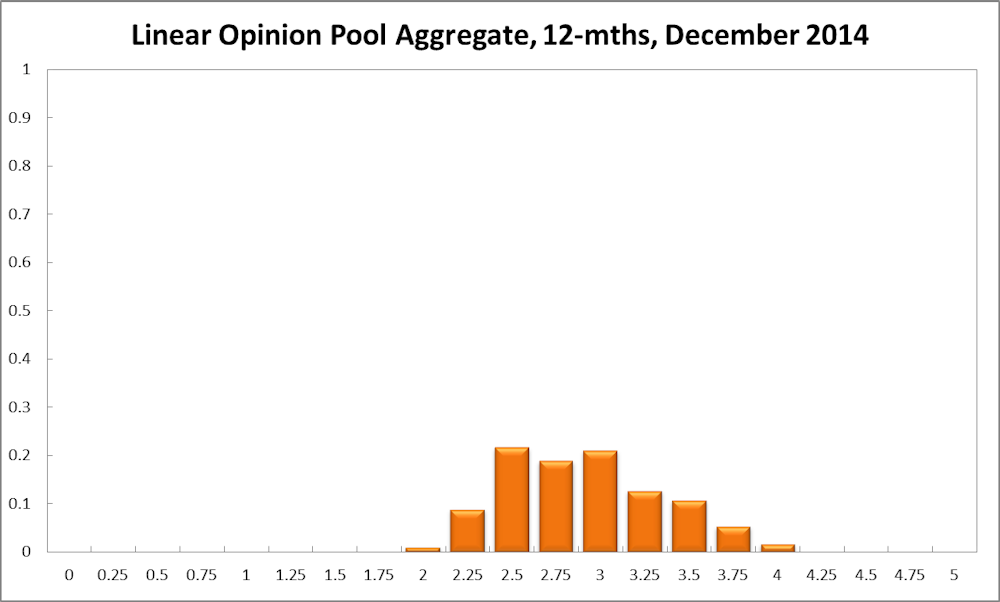

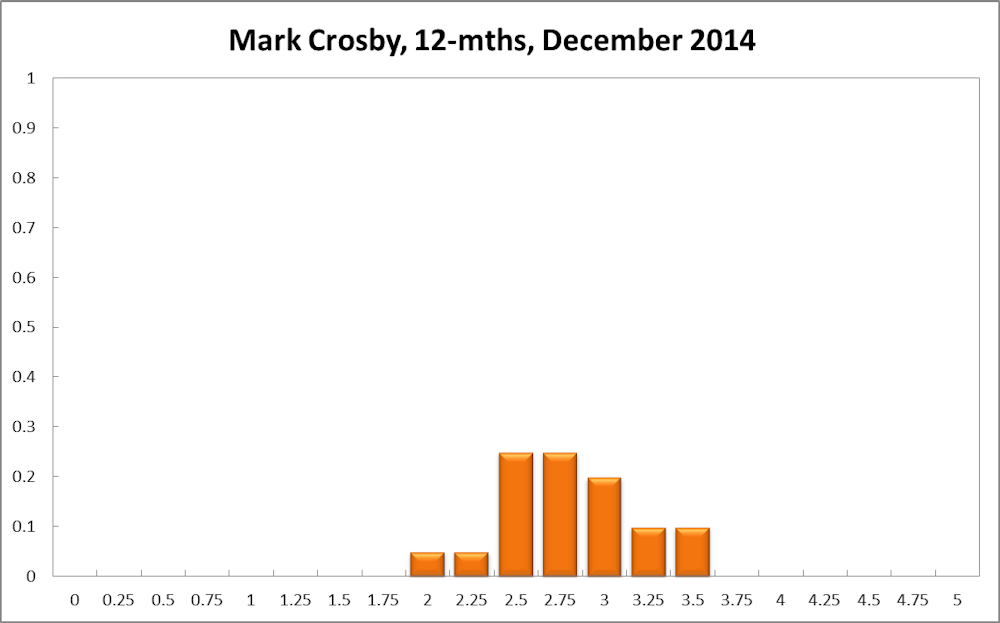

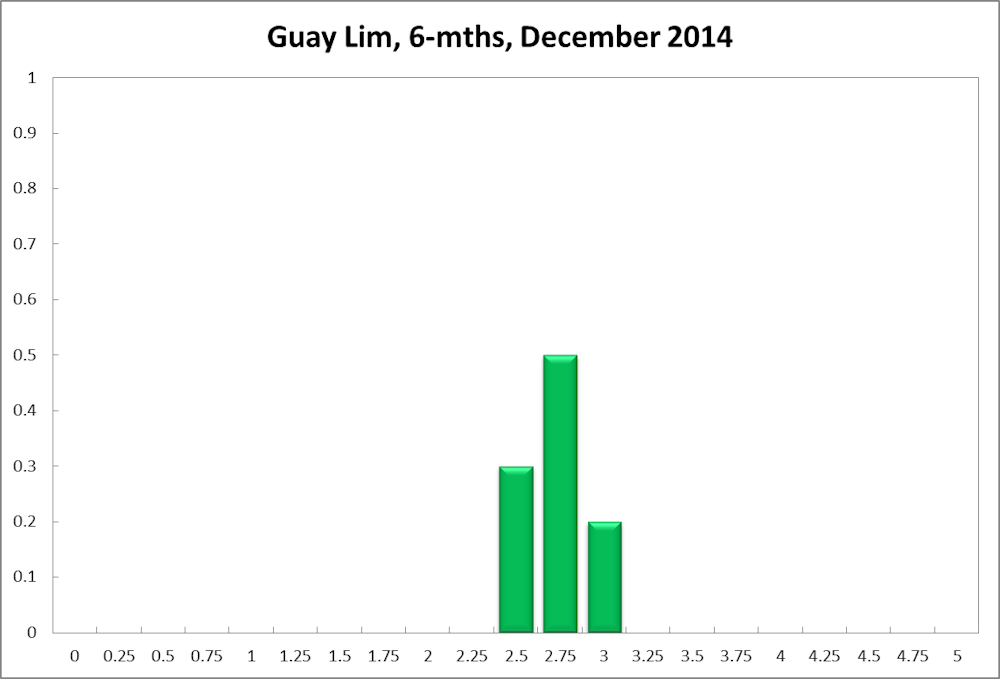

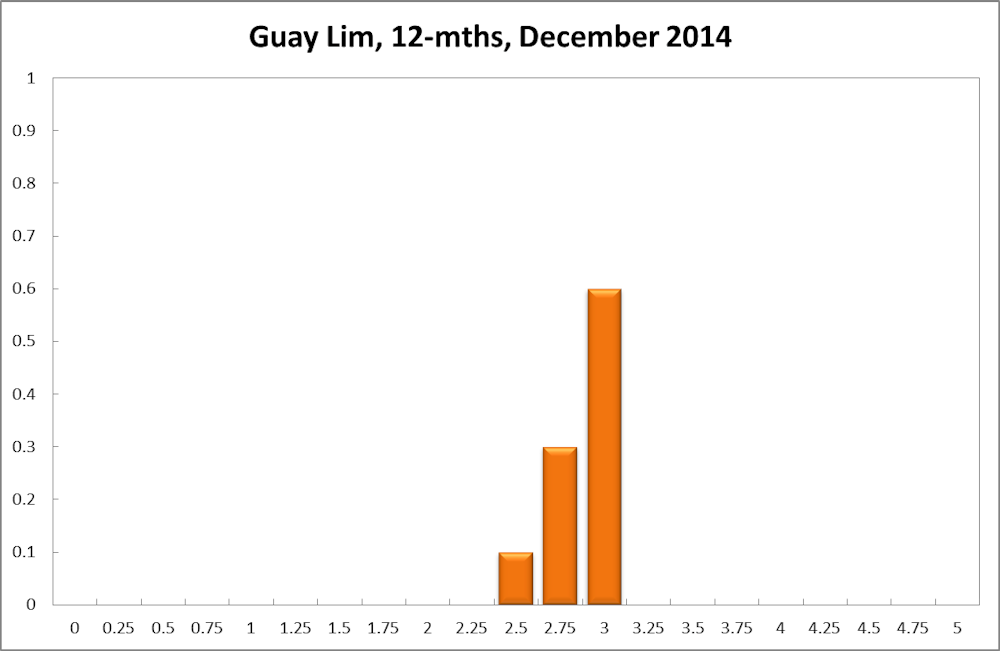

The probabilities at longer horizons are as follows: six months out, the probability that the cash rate should remain at 2.5% slipped down one percentage point, to 36%. The estimated need for an interest rate increase reverted back to its October value of 56% (54% in November), while the need for a decrease still equals 9%. A year out, the Shadow Board members’ confidence in a required cash rate increase is up 4 percentage points to 71%, the need for a decrease fell to 10% (12% in November), while the probability for a rate hold is 22% (23% in November).

Comments from Shadow Reserve bank members

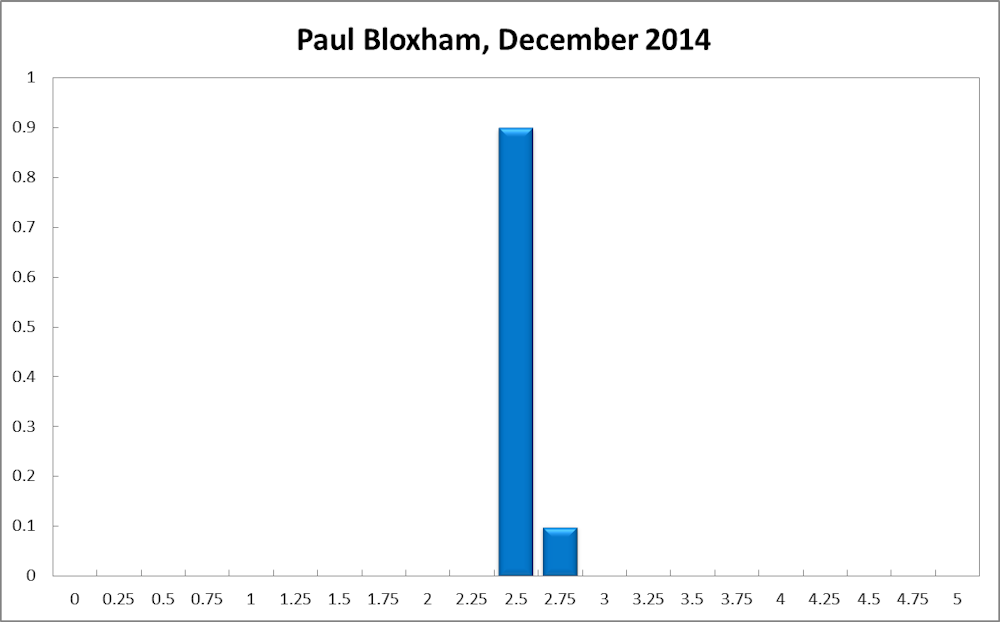

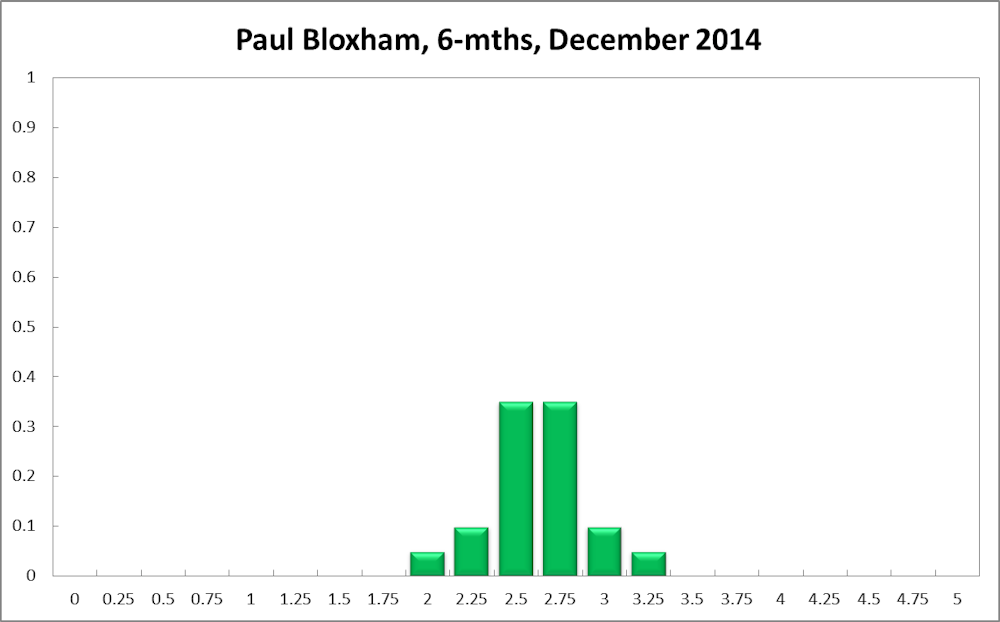

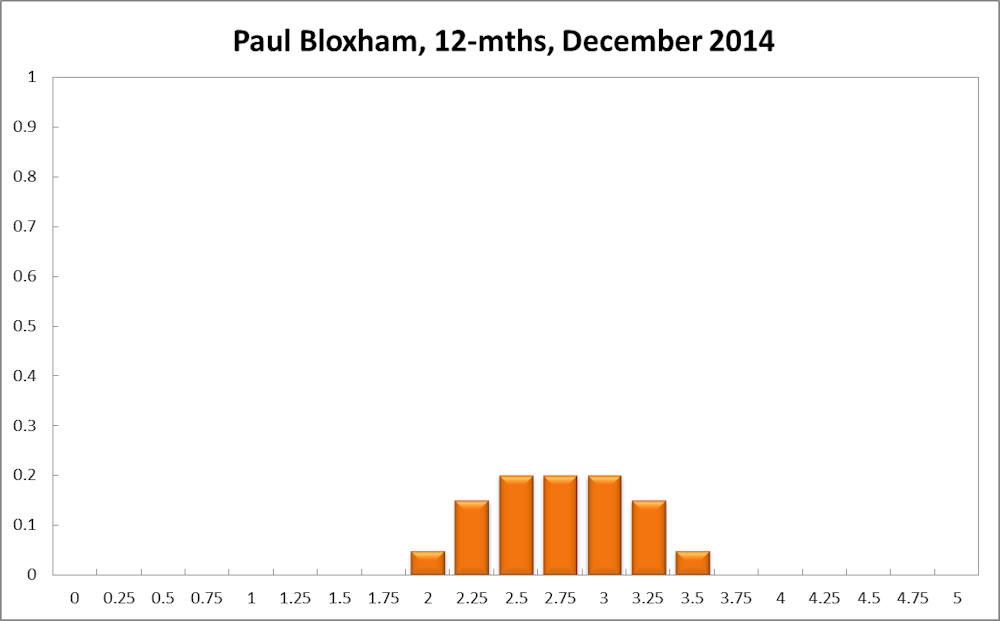

Paul Bloxham, Professor of Economics at Australian National University:

“Low interest rates are working to support growth.”

Australia’s economic growth is continuing to re-balance from being mining-led to non-mining-led, largely as a result of very accommodative monetary policy. There continue to be clear signs that low interest rates are working to support growth. Housing market activity is still strong and non-mining business conditions are gradually improving. As yet, this improvement is yet to appear in the official labour market indicators, although other labour market measures suggest some stabilisation of conditions.

At the same time, the mining sector has weakened further in recent months. Iron ore prices have fallen to new five-year lows, which will be a drag on national income growth. The appropriate policy response, however, is to allow fiscal policy to be looser in the face of weaker national income growth. Monetary policy is already doing its job and demanding more of it, by cutting rates further, increases the risk of asset price misalignments.

Given that growth remains below trend and inflation is well contained, I recommend that the cash rate is left unchanged this month. I still expect that the cash rate may need to be lifted in the next 6-12 months, given the growing risks that could stem from leaving interest rates too low for too long.

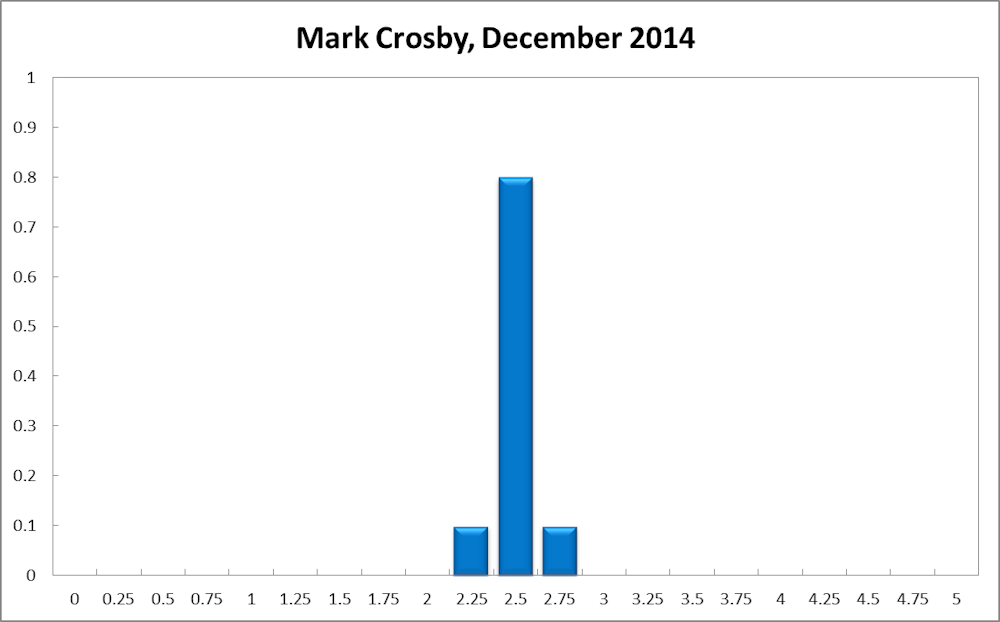

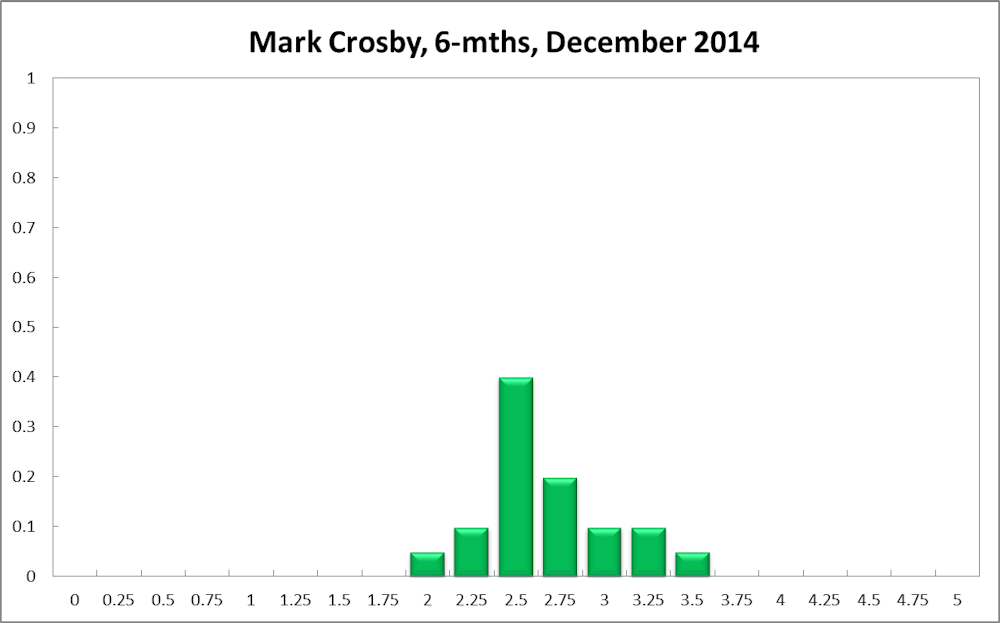

Mark Crosby, Associate Professor, Melbourne Business School:

“The RBA will sit on their hands again in December.”

Little data to change the outlook from the previous month, so the RBA will sit on their hands again in December. Chinese data is still mixed, though recent rate cuts may improve the medium-term outlook and so lead to improving growth and higher rates in the medium to longer term. However, these rate cuts also reflect concern over the outlook, so the more likely outcome will have the RBA waiting for clearer positive signals on the global outlook before raising rates.

Guay Lim, Professorial Fellow, Deputy Director, Melbourne Institute of Applied Economic and Social Research at University of Melbourne:

“The time for a rate change is approaching.”

There are signs that growth in the economy is picking up, with contributions from non-mining investment and net exports. Although the unemployment rate is likely to stay around 6% for a few more months, it is expected to fall next year. It would be prudent to keep the cash rate at 2.5% for now, but the time for a rate change is approaching.

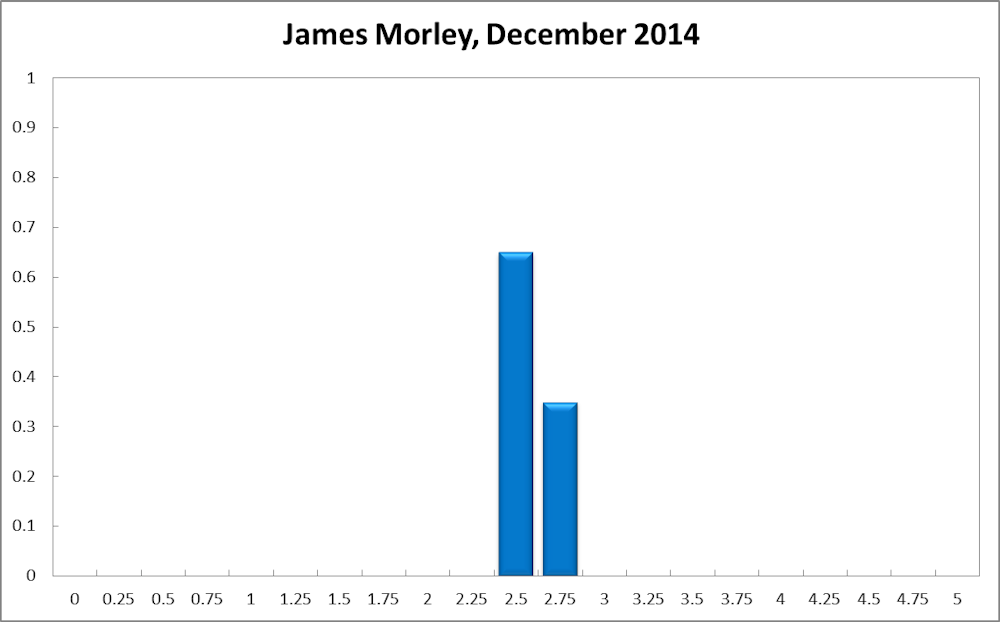

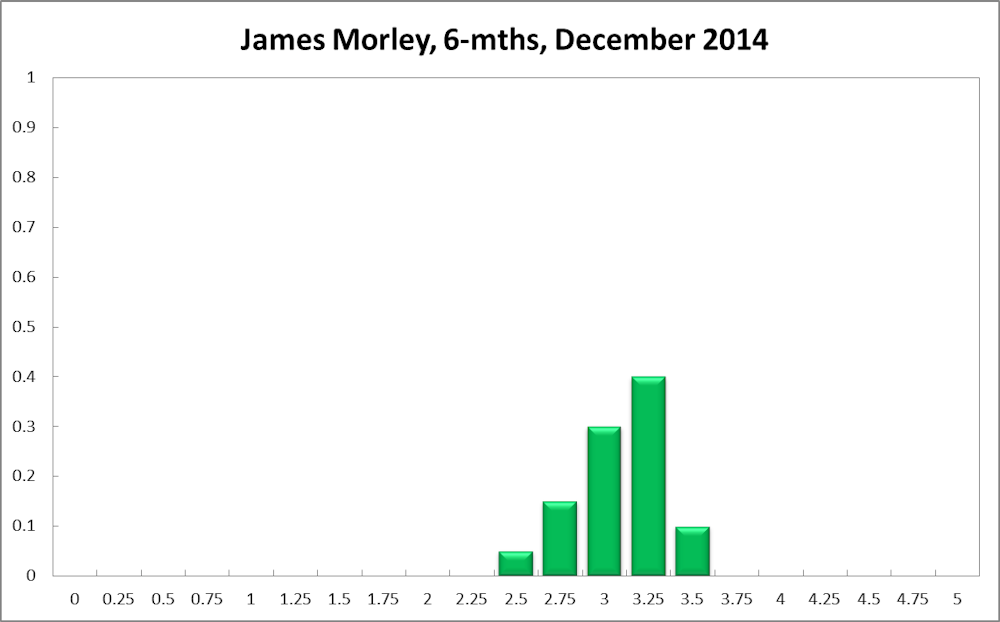

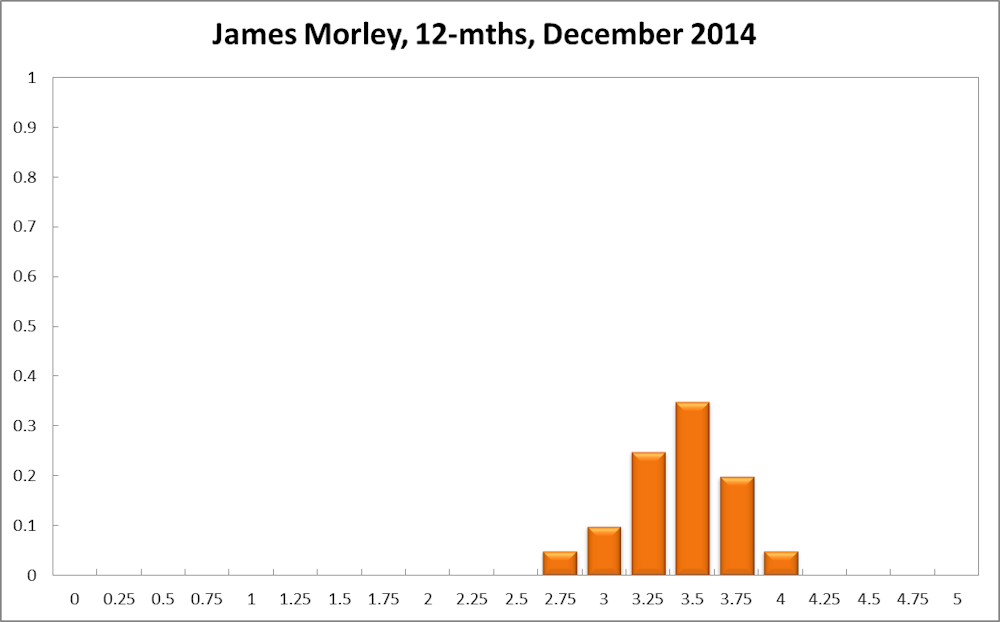

James Morley, Professor of Economics and Associate Dean (Research) at UNSW Australia Business School:

“I anticipate that the RBA will not start raising rates until early to mid-2015.”

Inflation could pick up slightly in the near term as the one-time impact of removing the carbon tax wears off. But it should remain within the 2-3% target range. Meanwhile, a lower dollar and stable unemployment continue to provide scope for an increase in the policy rate to help cool the housing market.

But, similar to last month, I anticipate that the RBA will not start raising rates until early to mid-2015 after they have signalled a change in their plans for “a period of stability in interest rates”. Instead, there may be an imminent announcement on loan-to-value restrictions for mortgages similar to what was implemented by the RBNZ in New Zealand last year.

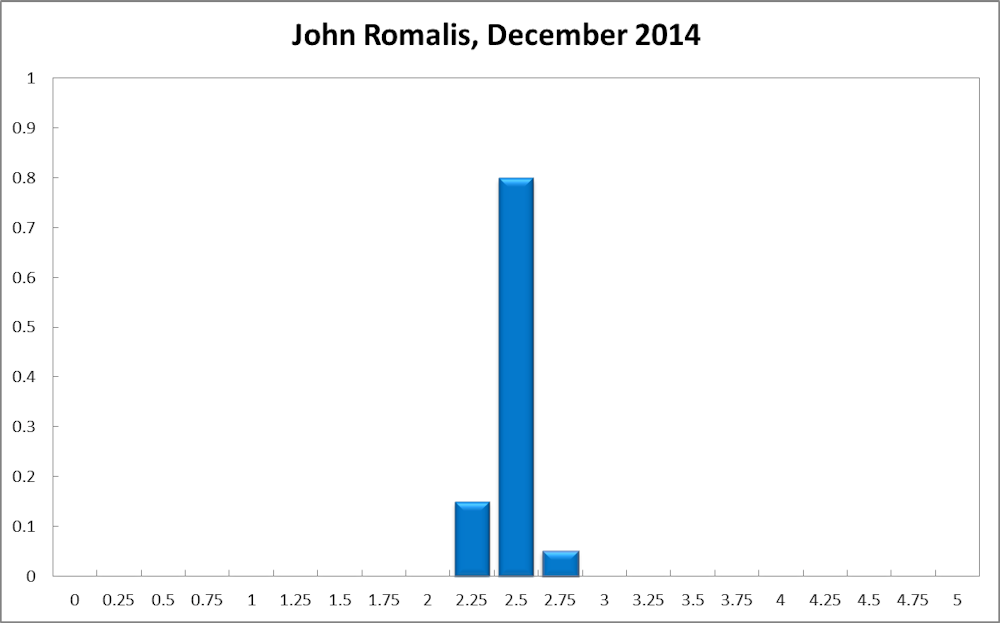

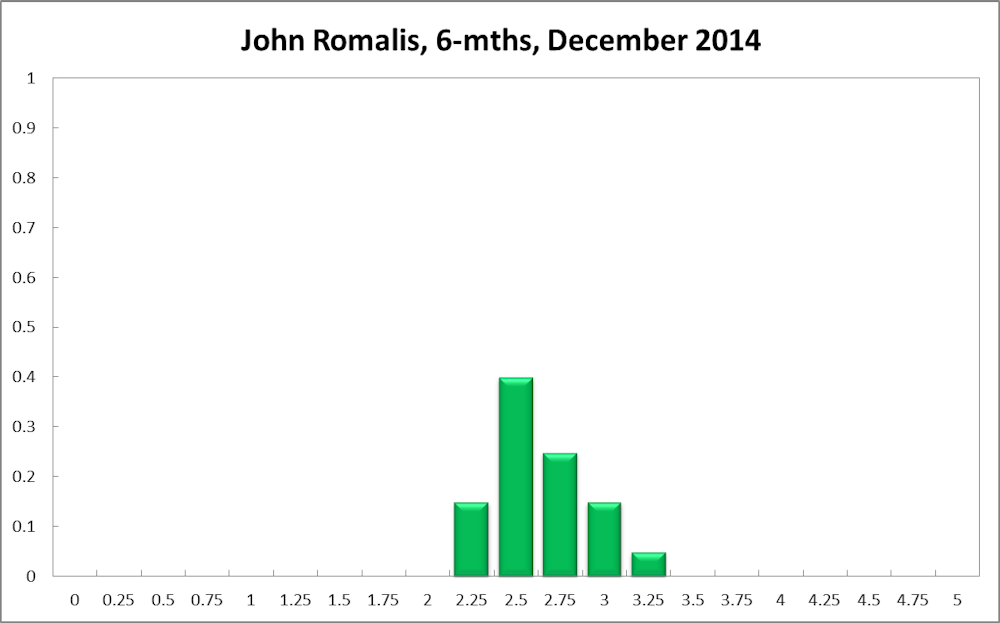

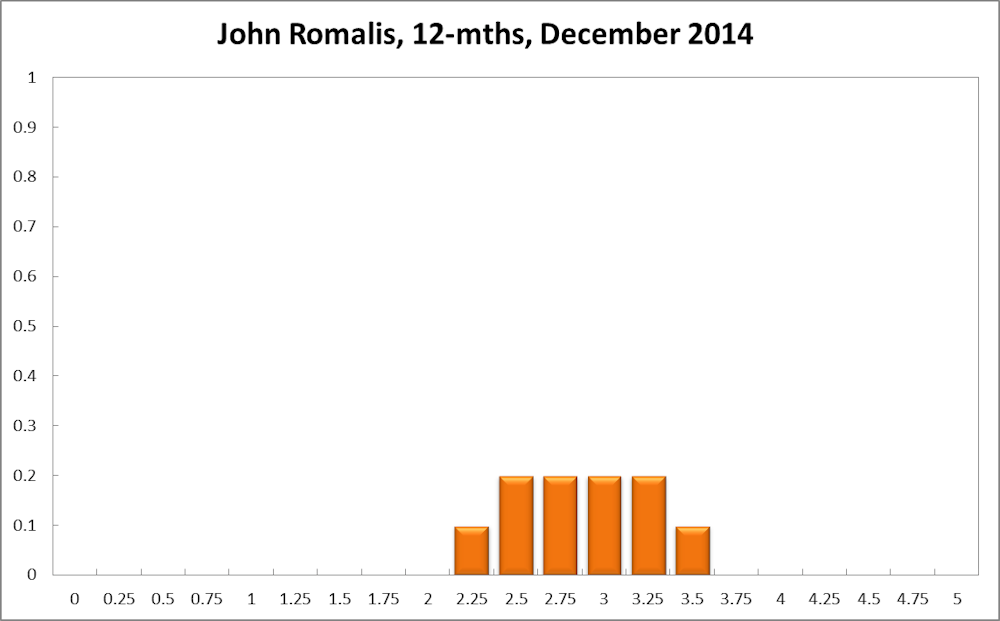

John Romalis, Professor of Economics at the University of Sydney:

Moderate domestic growth, stable inflation, weakening commodity prices, slightly slower growth in China and fragility in Europe suggest that the target cash rate should not be rising any time soon.

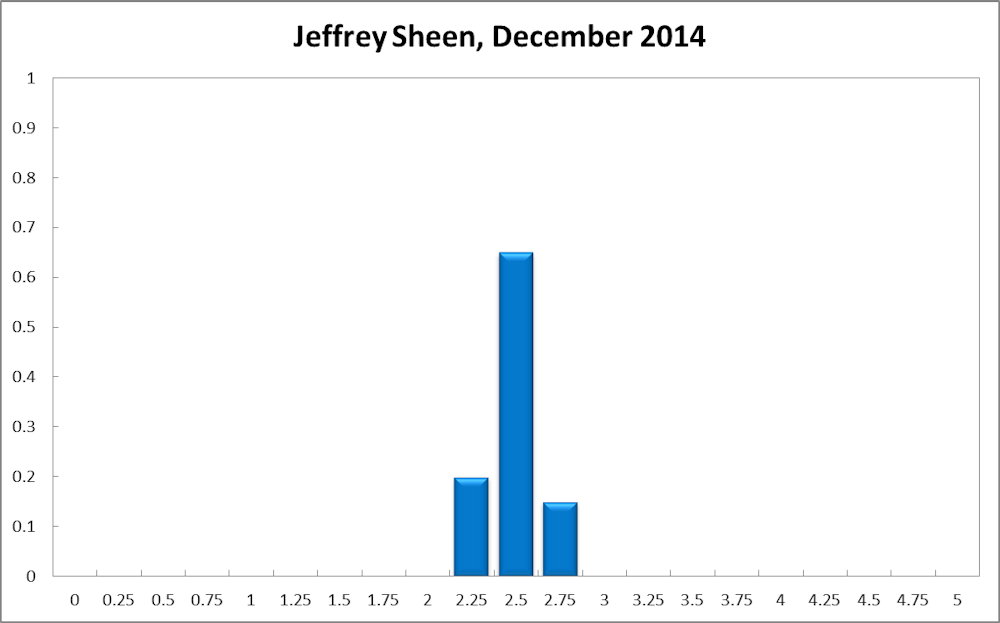

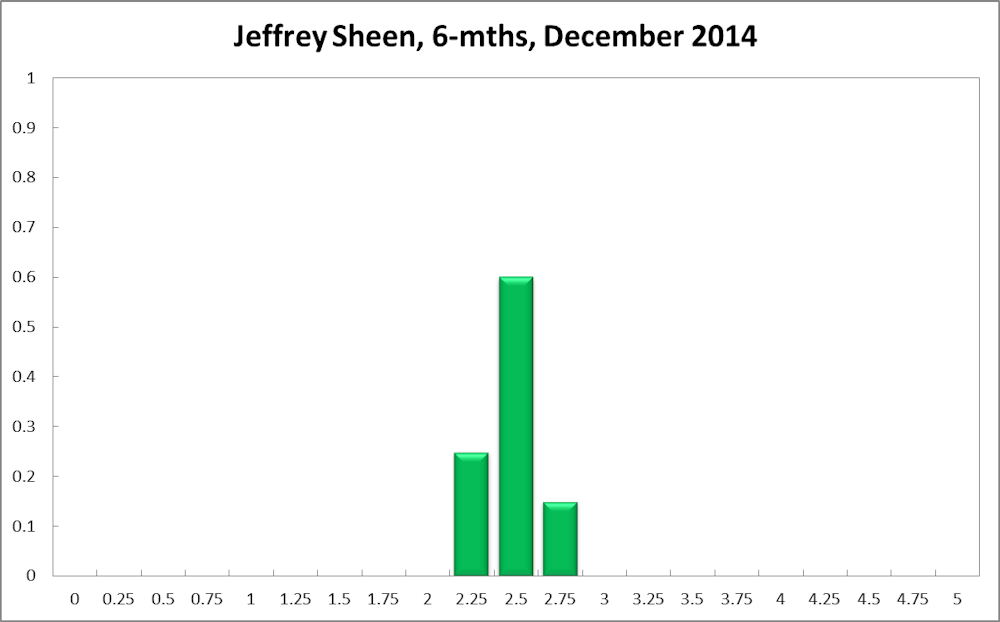

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“The major unknown is when the Fed will choose to make its next move.”

The modest trade-weighted growth of Australia’s major trading partners is likely to change little into 2015. Weakness in Japan and Europe should mean low global interest rates and ample liquidity through 2015, though the major unknown is when the Fed will choose to make its next move, given the growing strength in the US economy.

The RBA should remain cautious about raising the cash rate because the Australian dollar is likely to remain too strong into 2015. Australia needs further real depreciation to assist in the gradual rebalancing of its growth from the mining to the non-mining sectors. Though waiting for this rebalancing to occur risks asset price inflation, this is not yet a problem that should influence monetary policy.