The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set. Timo Henckel is the non-voting chair of the Board.

Australian headline inflation eased from 3% p.a. in the second quarter to 2.3% p.a in the third quarter. The drop in inflation, along with the continued weakness in the global economy, takes some pressure off the RBA to lift the cash rate. On the other hand, the strong real estate market poses a worrying risk to financial stability.

The CAMA RBA Shadow Board continues to recommend with confidence that the cash rate remain at its current level. The Board attaches a 71% probability that the cash rate ought to remain at 2.5% in November. The confidence attached to a required rate cut equals 6%, while the confidence in a required rate hike has decreased to 23%.

The drop in headline inflation to 2.3% reduces the pressure for the RBA to lift the cash rate. However, the lower inflation rate is largely driven by a fall in electricity prices, following the abolition of the carbon tax in July, and should be interpreted as a once off adjustment to prices as opposed to a sustained fall in inflation. Furthermore, continued weakness of the Aussie dollar will add inflationary pressures to the domestic economy in the medium run.

The continued weakness of the Australian dollar will be welcome news for many exporters, especially in the manufacturing, education and tourism sectors. However, it normally requires sustained weakness of a currency before export volumes pick up.

Wages growth has been weak recently and with the unemployment rate above 6% will probably remain weak in the medium term.

Business indicators have softened further: the NAB Business Confidence, the Manufacturing PMI, and the Australian Performance of Services Index all posted lower numbers. The capacity utilisation rate fell to 80.17%. On the upside, the Westpac consumer confidence index improved slightly. Estimates of GDP growth are largely unchanged. Residential construction has continued to strengthen, benefiting from low interest rates and rising house prices. The fiscal outlook remains unclear with the government still not managing to pass all components of its May budget in the Senate.

The global economy is worsening. Europe, including Germany, looks to slide into recession. China’s economy seems a long way from returning to double-digit growth. The US economy has been mixed but low and falling inflation expectations in the world’s largest economy do not bode well for the future. In spite of the Federal Reserve Bank’s assurance that it will not revive its policy of quantitative easing, US interest rates, and global interest rates, are likely to stay very low for some time. The deterioration of the armed conflicts in Iraq and Syria pose a serious threat to the world economy.

What the CAMA Shadow Board believes

The consensus to keep the cash rate at its current level of 2.5% remains unchanged at 71%. The probability attached to a required rate cut equals 6% (4% in October) while the probability of a required rate hike has fallen to 23% (25% in October).

The probabilities at longer horizons are as follows: 6 months out, the probability that the cash rate should remain at 2.5% edged down one percentage point, to 37%. The estimated need for an interest rate increase fell to 54% (56% in October), while the need for a decrease equals 9% (7% in October). A year out, the Shadow Board members’ confidence in a required cash rate increase is down 4 percentage points to 67%, the need for a decrease edged up to 12% (9% in October), while the probability for a rate hold rose to 23% (20% in October).

Comments from Shadow Reserve bank members

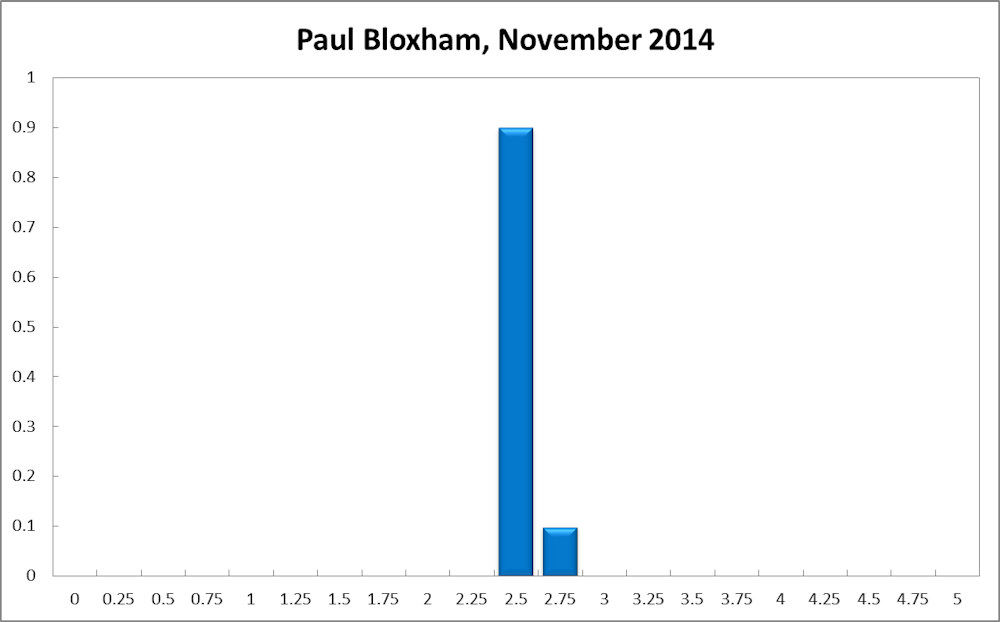

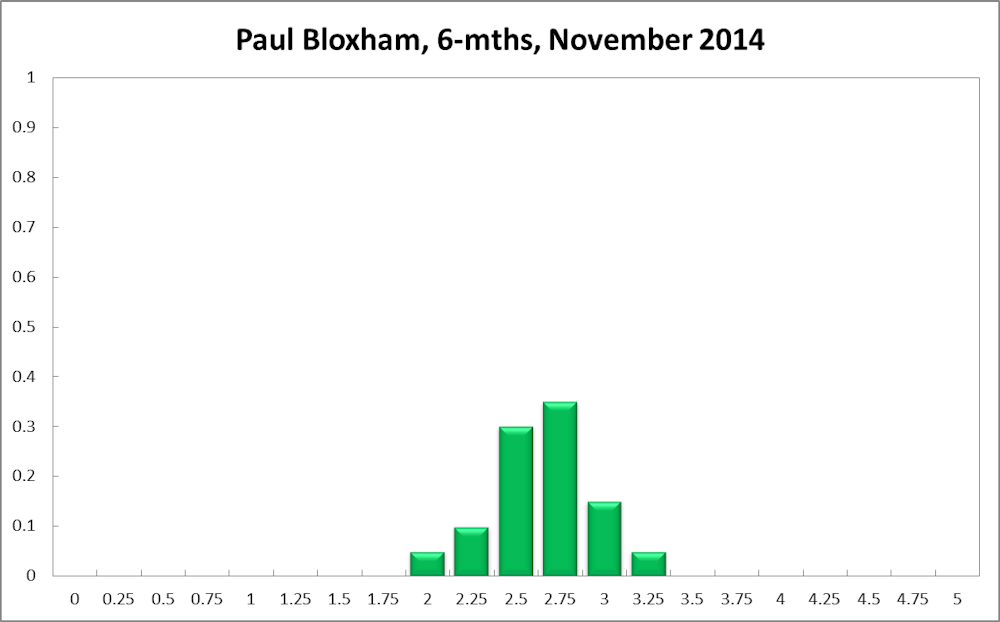

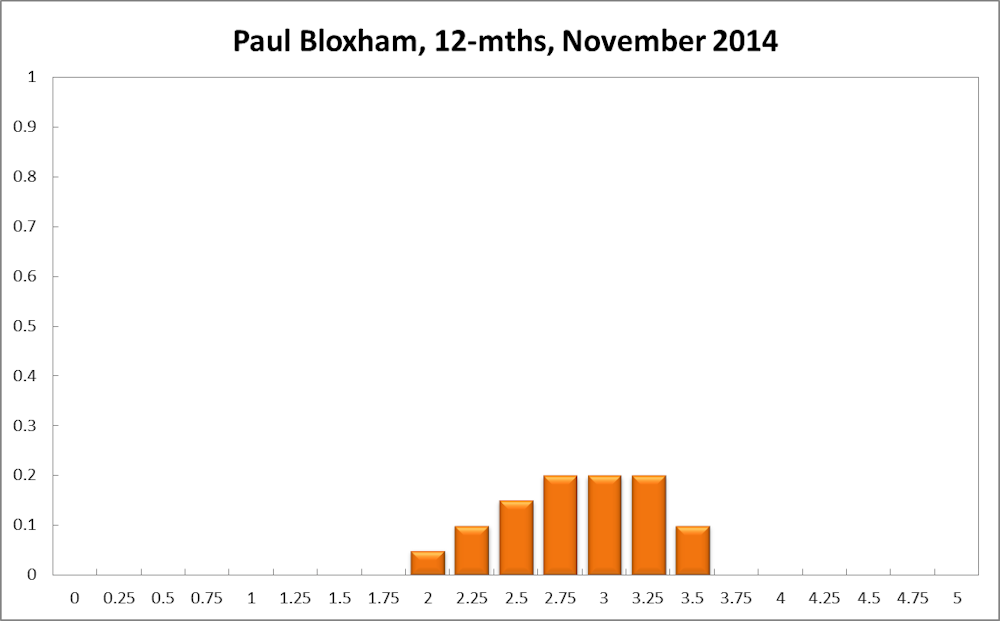

Paul Bloxham, Professor of Economics at Australian National University:

“The pick-up in the non-mining sectors is being led by a strong rise in housing prices.”

The re-balancing of Australia’s economic growth from being driven by the mining sector towards the non-mining sectors has continued and is being supported by very low interest rates and a lower Australian dollar.

The pick-up in the non-mining sectors is being led by a strong rise in housing prices and an upswing in the residential construction cycle. Other sectors of the economy are showing positive signs and the rise in demand has been sufficient to keep underlying inflation in the upper half of the RBA’s target band over the past year. The pick up in demand has, however, not been strong enough to put downward pressure on the unemployment rate as yet, although there are signs that the labour market has stabilised.

As the cash rate has now been very low for an extended period, the risks of asset price misalignments are also increasing, with the strong rise in housing prices and increased investor interest in housing both symptoms of increased risk taking. Given that growth remains below trend and inflation is well contained, I recommend that the cash rate is left unchanged this month. I still expect that the cash rate may need to be lifted in the next 6-12 months, given the growing risks that could stem from leaving interest rates too low for too long.

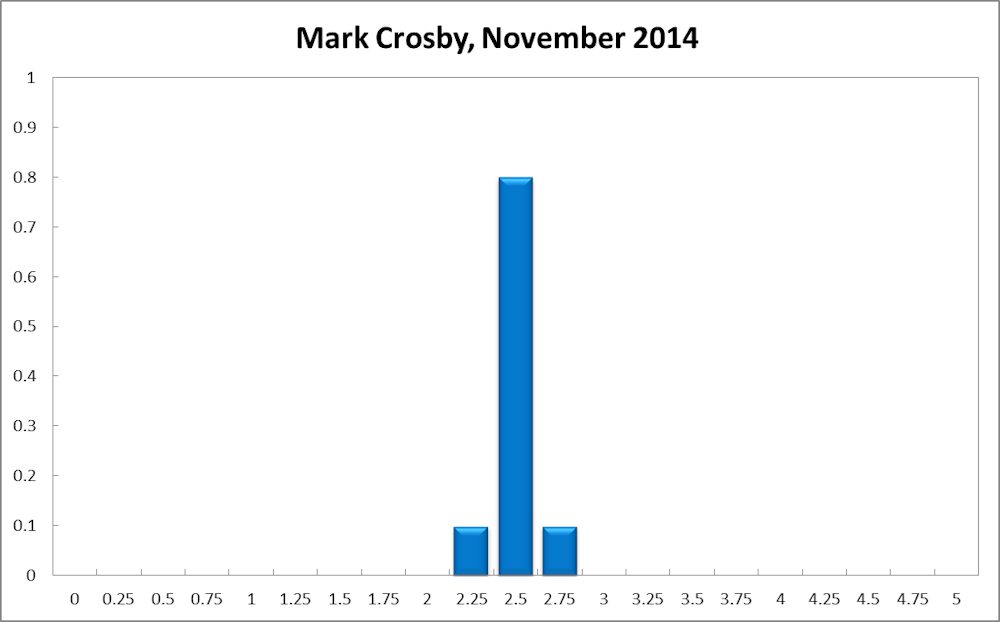

Mark Crosby, Associate Professor, Melbourne Business School:

“The global outlook remains highly uncertain.”

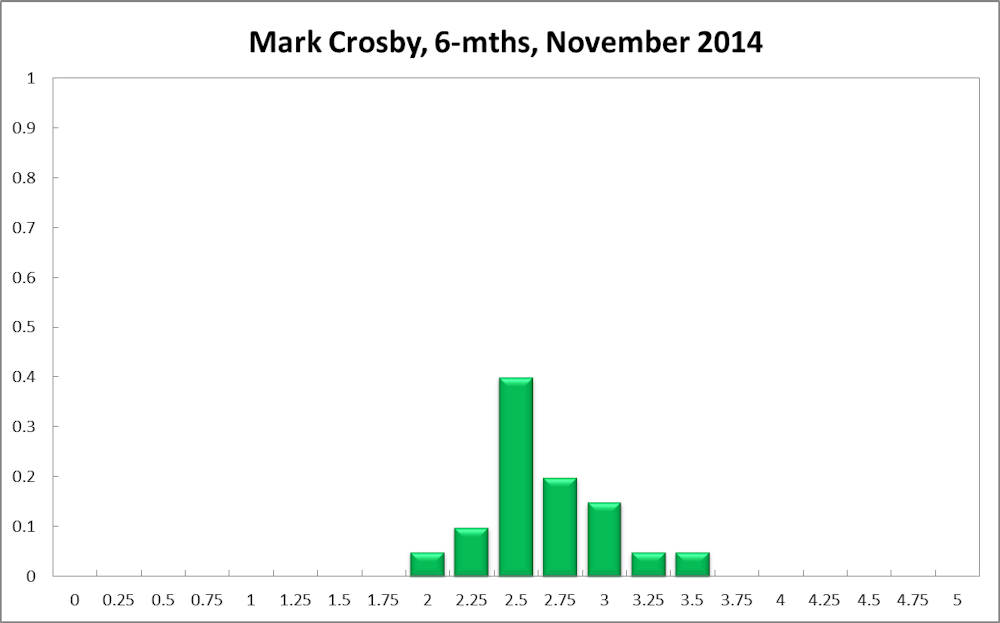

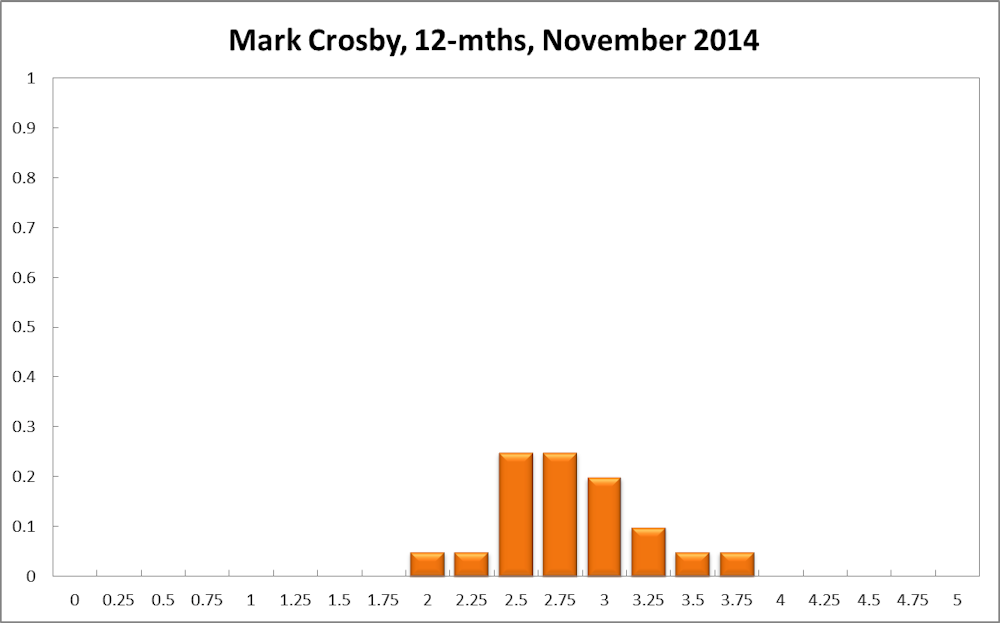

Recent weak wages growth is consistent with modest inflation outcomes in the medium term, and so less reason to raise rates in the next six months. Given asset price pressures it would still seem desirable to be moving rates towards a more neutral stance at the 12 month horizon. The global outlook remains highly uncertain however, and negative shocks may yet see rates stay on hold.

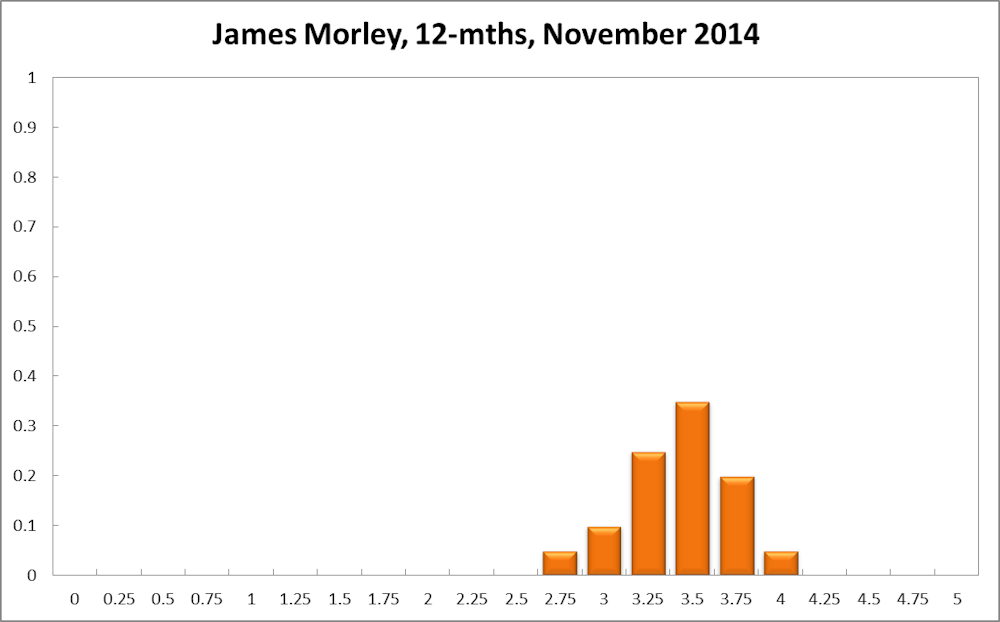

James Morley, Professor of Economics and Associate Dean (Research) at UNSW Australia Business School:

“The continued overheating of the housing market needs to be addressed.”

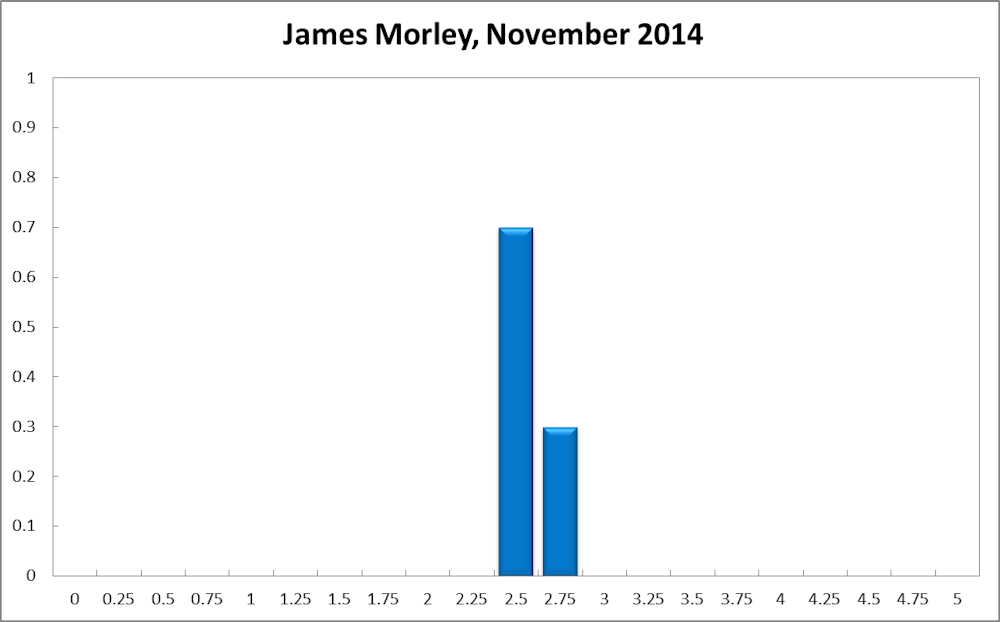

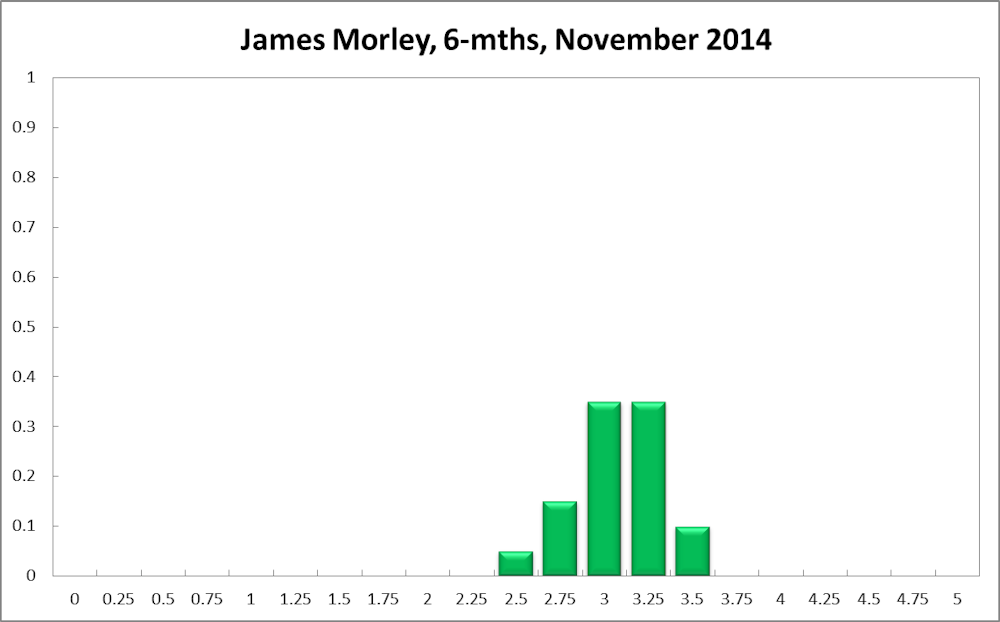

Inflation eased in the most recent quarter to 2.3%. This provides the RBA with more scope to maintain its policy rate at the current low level. However, the continued overheating of the housing market needs to be addressed before it leads to a huge problem down the road.

Macroprudential policies such as restricting loan-to-value ratios provide a possible means for the RBA to cool the housing market. But these policies can have large distributional effects (e.g., they particularly affect first-time home buyers), without necessarily achieving a large overall effect on the market. Thus, the RBA will have to back up any macroprudential policies with an increase in the policy rate in the near term, returning it back towards its neutral level. A lower dollar and stable unemployment provide scope for such a move by the end of the year.

But I anticipate that the RBA will not, in fact, start raising rates until March or April at the earliest after they have signalled a change in their plans for “a period of stability in interest rates”.

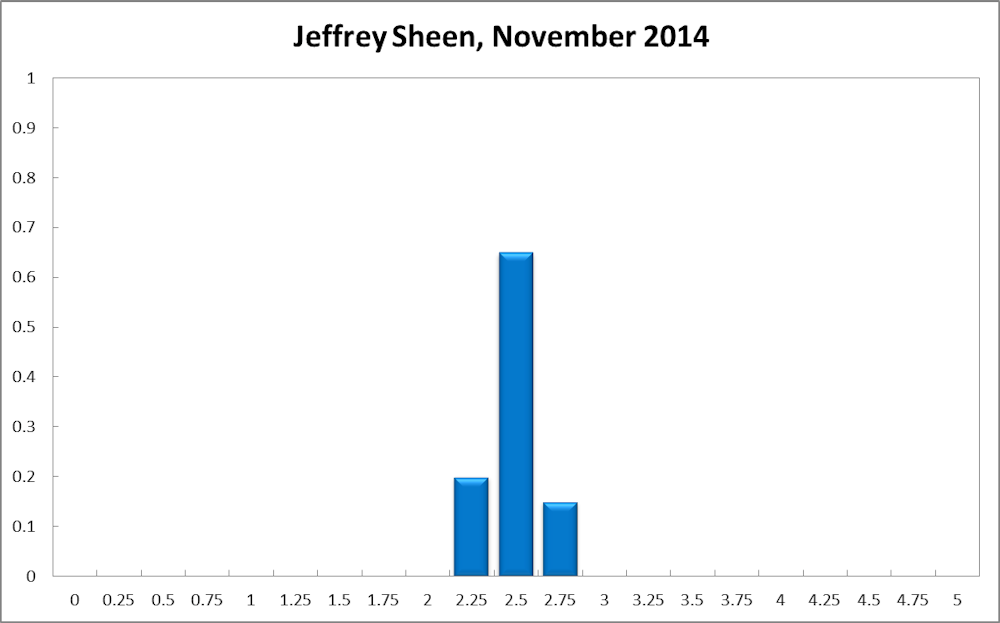

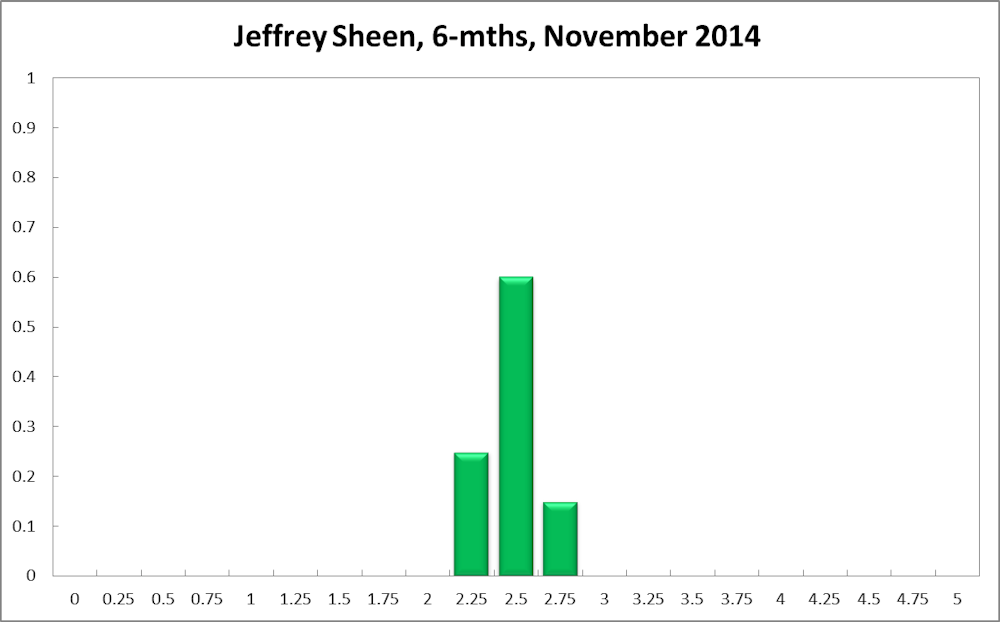

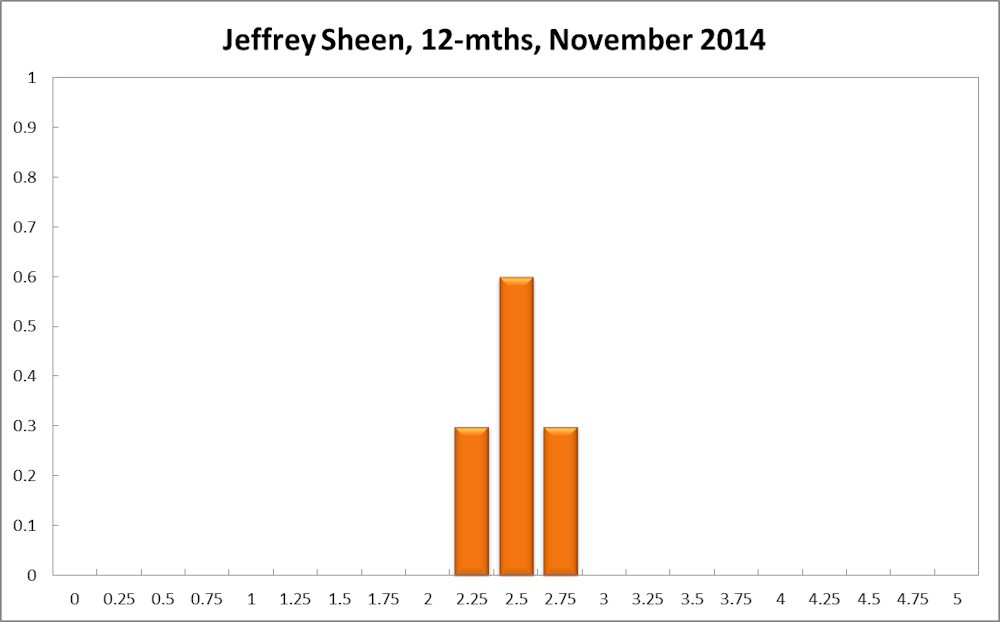

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“The RBA may need to delay raising the cash rate.”

Few would have expected that the world’s economies would still be grappling with the shadow cast by the 2008 financial crisis. While the US Fed has now completed its planned quantitative easing as the US economy begins to approach normality, the ECB has finally begun its program to provide much needed liquidity to the ailing Euro area. This should mean global interest rates will remain low for longer, and thus keep low the cost of foreign-sourced funds for Australian financial institutions.

As a result, the RBA may need to delay the time when it will begin raising the cash rate. However there is a marginally higher probability of a cut next year if the downward trend in Australia’s trading partners’ economies persists into 2015, notwithstanding the recent 5% depreciation of the real TWI (mainly due to the strengthening US dollar, to which the yuan is essentially pegged), which is a positive sign for Australian exports.