The Council of Small Business of Australia (COSBOA) and The Tax Institute plan to hold a round table meeting this May with the purpose of developing a better definition of small business for tax and legal purposes.

Yet why is this issue of importance?

The problem of defining small business

From an academic perspective the ability to define and classify subjects for future analysis is important. In the natural sciences the process of taxonomy is valuable as it helps to identify, name and classify organisms allowing for better measurement in future research. A problem with small business research is the lack of a common agreement about how to define and classify this type of organisation.

Around the world there are many different approaches to defining small to medium sized businesses. For example, in many parts of Asia a small business is one that has less than 50 employees. In the European Union it is a business with less than 50 employees but also an annual turnover of below €10 million. However, in the United States a small business has less than 500 employees.

Such wide variations in the way small businesses are classified poses significant challenges for researchers trying to make comparisons of businesses across different countries.

How do we define small business in Australia?

The Australian Bureau of Statistics (ABS) defines a small business as one that employs fewer than 20 people. This business will typically be independently owned and operated. The owner-managers who run the business will also tend to be the principal decision makers. They will also contribute and own all or most of the firm’s operating capital.

However, there are many sub-types of small business. The ABS also recognises micro-businesses that have less than 5 employees. Here we can separate them further into those that employ and those that only have the owner-managers as employees. There are also medium sized businesses that have between 20 and 200 employees.

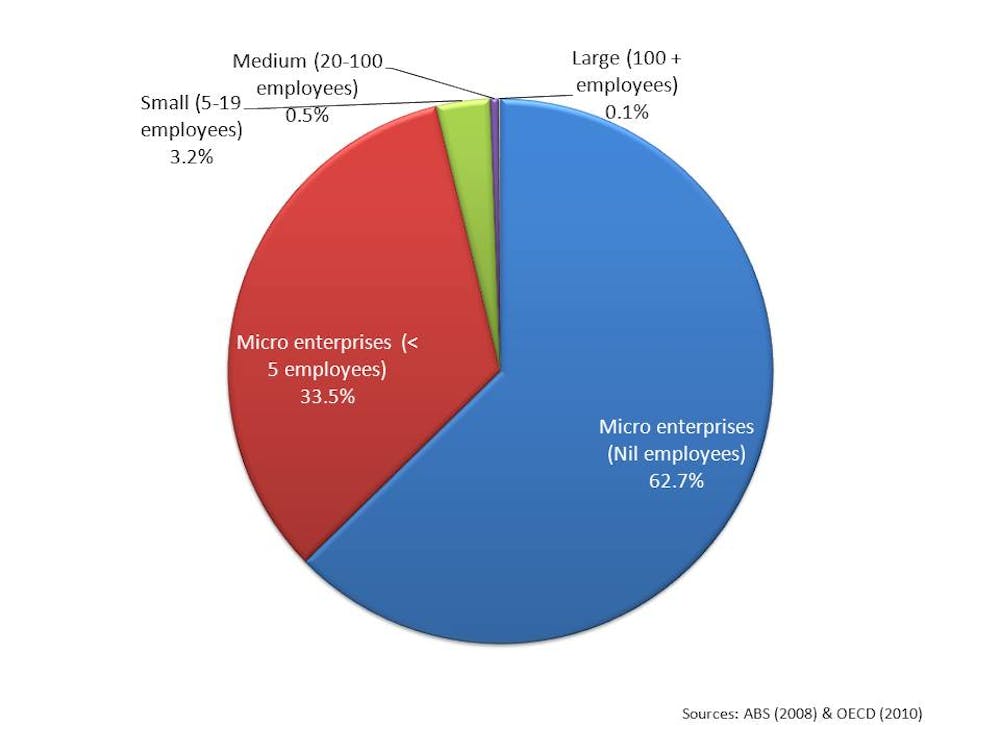

When we examine the distribution of such firms across the spectrum of total Australian businesses an interesting pattern emerges (see graph). First, the proportion of large firms with more than 200 employees is less than 1%, although they make up around 35% of all employment. The remaining 99% of all businesses are divided into 63% non-employing micros, 33.5% employing micros, 3% small and 0.5% medium firms.

What this suggests is that around 96% of all our businesses are employing fewer than 5 people and the majority of those do not employ at all. Rather than business organisations these micro-firms are individuals seeking to earn a living through entrepreneurial endeavour. In essence there are some 1.2 million self-employed business operators throughout Australia who are not sub-contractors. The majority (79%) are supporting their families with this business activity.

So why is there a problem with a lack of definition?

Considering that the ABS has already defined and apparently measured our small business sector you may wonder why COSBOA and The Tax Institute feel it is so important to develop a better definition.

The reason is that despite the work of the ABS the way small businesses are defined by government for different purposes is quite unrelated to the statistical agency’s classification system. For example, the Australian Taxation Office (ATO) focuses on annual turnover not employment. So a small business is one that has an annual turnover (excluding GST) of less than $2 million. In the case of businesses that are part of a group or that have subsidiaries, the ATO uses “aggregated turnover” and may even consider a firm’s aggregate net assets which must be less than $6 million.

In the case of employment, Fair Work Australia (FWA) defines a small business as one that has less than 15 employees whether full or part time. The ability to meet this definition offers the owner-manager a simplified approach to the dismissal of employees and 12 months rather than 6 months as the period of time in which unfair dismissal claims cannot be made.

Another contentious issue that combines taxation and employment together is state payroll tax. In NSW the current threshold is an annual wages bill of $678,000. In WA the threshold is $750,000. Although the 2007 Harmonisation Protocol seeks to bring this into alignment.

For the purposes of the Privacy Act a small business is defined as a business that has an annual turnover for the preceding financial year of below $3 million. Another area where there are definition issues is in the Equal Opportunity for Women in the Workplace Act (1999). Firms with fewer than 100 employees are not required to comply with this legislation.

OK so what should be done?

So it seems that there is a good deal of complexity and lack of consistency in how we define small businesses. As can be seen from these examples the two most common variables used to define small firms are employment and annual turnover. This is due to the interest that governments have with unemployment and the collection of tax.

How we define a small firm does matter, and we should start to look more closely at variables other than employment and turnover. These may include whether or not the business is engaged in a particular industry (this is common in many other countries that differentiate manufacturers from services). It might also consider if the business is home-based or how much money it expends each year into R&D.

Given these complexities the development of a universal definition of small business seems challenging. It might also be a disadvantage to many small firms if a single definition were applied.

Of more value would be a taxonomy of small business developed for different purposes that recognised the management realities of the small business operators. We need to focus such definitions or classification systems so as to find ways to help these businesses. After all, they are the majority of Australia’s business community.