This is the fourth in a series of articles on cash flow management in small firms that I have prepared for this column, drawing upon academic research papers published in the past five years. In this article we look at cash flow management within small owner-managed businesses from a systems perspective. I have selected two papers that address the process of financial management in small firms with reference to Australian and British companies and different accounting or performance measurement systems.

Performance measurement practices in small Australian manufacturing firms

The first study is by Sujatha Perera and Pamela Baker of Macquarie University. It was published in Small Enterprise Research: The Journal of SEAANZ in 2007. They surveyed 86 small to medium sized manufacturing firms in Sydney and followed up with in-depth interviews with eight of the owner-managers from these firms.

The research sought to determine whether small firms place more emphasis on financial measures than non-financial measures in their performance measurement systems. They also examined whether larger firms used more performance measures than their smaller counterparts, and if there were differences between small business owners and non-owner managers.

The study found that 95% of the firms surveyed regularly measured their performance, but only 47% made use of non-financial measures. These included such things as share of market, employee absenteeism and productivity, plus customer satisfaction. Key financial measures included sales revenue, profitability, cash flow, cost reduction and return on investment.

It was also found that as firms grew larger there was an increase in the total number of performance measures used. However, this was only found to be significant for financial measures and not for those relating to employee or product performance.

It was also found that non-owner managers of small firms made greater use of performance measures, specifically non-financial ones. However, the frequency with which the owners and non-owner managers monitored their performance measures was not found to be significantly different.

In discussing their findings, Perera and Baker noted that the owner-managers who they interviewed in-depth were all highly focused on financial controls. They reported being “cost conscious”, having “tough profit targets” and seeking to control costs. However, they also appeared to have relatively unsystematic “ad-hoc” approaches to performance management. They also seemed to be “slow in their move towards more systematic performance measurement systems” even when the firm had experienced growth. This was attributed to a lack of time and other resources.

This study highlights the focus by most small business owner-managers on financial rather than non-financial performance measures and the relatively unsophisticated nature of such systems. It should come as no surprise to find non-owner managers make greater use of performance measures. Such individuals have a responsibility to the actual owners to look after the business and as professional managers they are more likely to be skilled in management systems and their implementation.

Financial reporting by small firms

The second study is by S. Sian from Cardiff University and C. Roberts from the University of Aberdeen. Their paper examines the accounting and financial reporting needs of small firms in the United Kingdom. This study was published in the Journal of Small Business and Enterprise Development in 2009.

They surveyed 398 accountants and 299 small business owners in the UK in order to assess the demand for and usefulness of financial reporting guidelines in relation to small owner-managed businesses. They found that 57% of small firms surveyed made use of external accountants or bookkeepers to assist with tax compliance and financial reporting. Not surprisingly the larger the business became, the more sophisticated their financial management systems.

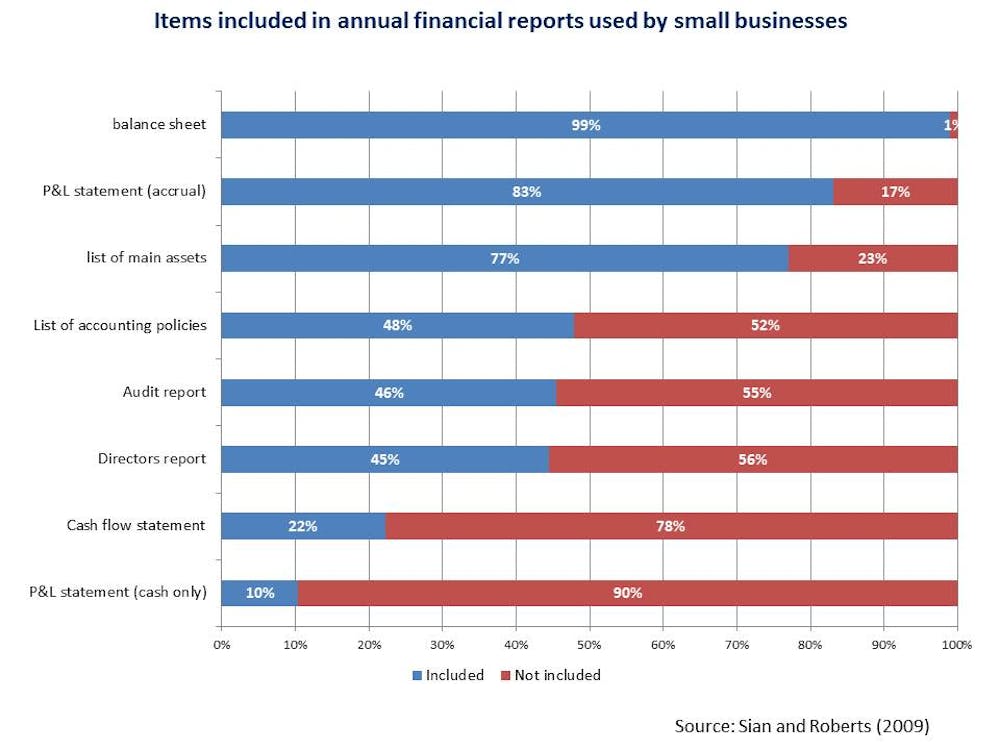

Of interest were the findings. When asked about their financial reporting statements most of the small business owners indicated that they received a balance sheet, accrual based profit and loss (P&L) statement and list of main assets held by their company. However, only 22% reported getting cash flow statements and only 10% a P&L statement based on a cash accounting approach. These results have been summarised in the following chart.

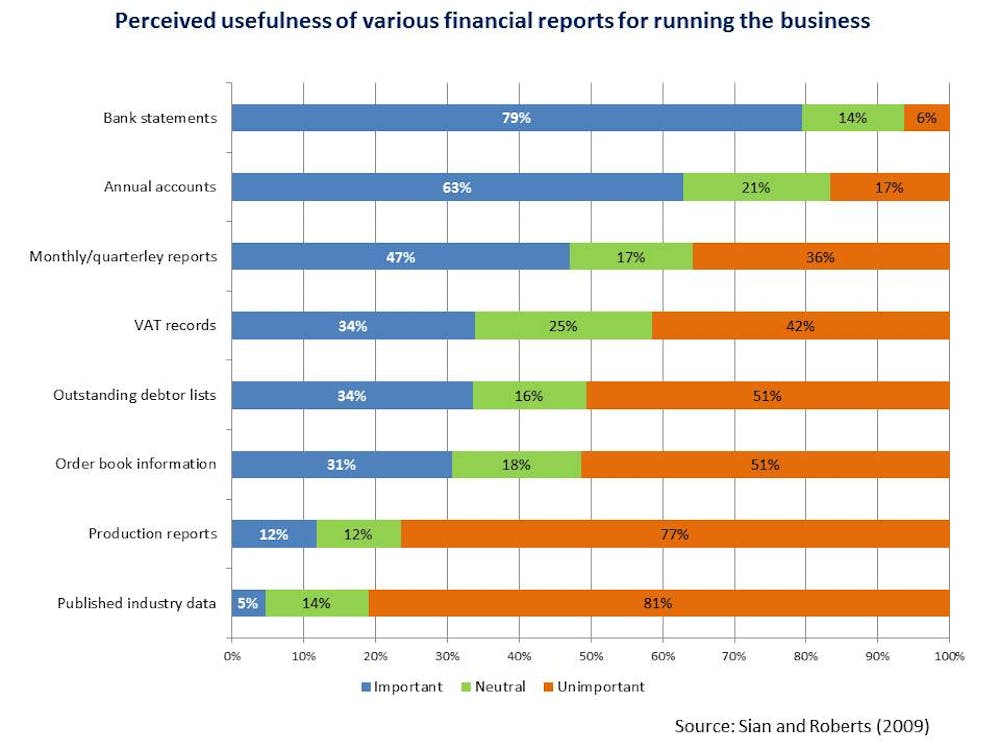

When asked about the usefulness of different types of financial reporting systems as an aid to running their business, the majority of small business owners reported that the most important sources of information were bank statements, followed by annual financial accounts. Of much less importance was published industry data and production reports. This is illustrated in the chart below, and it is worth noting that just over half the owner-managers considered their outstanding debtor lists as being of little importance.

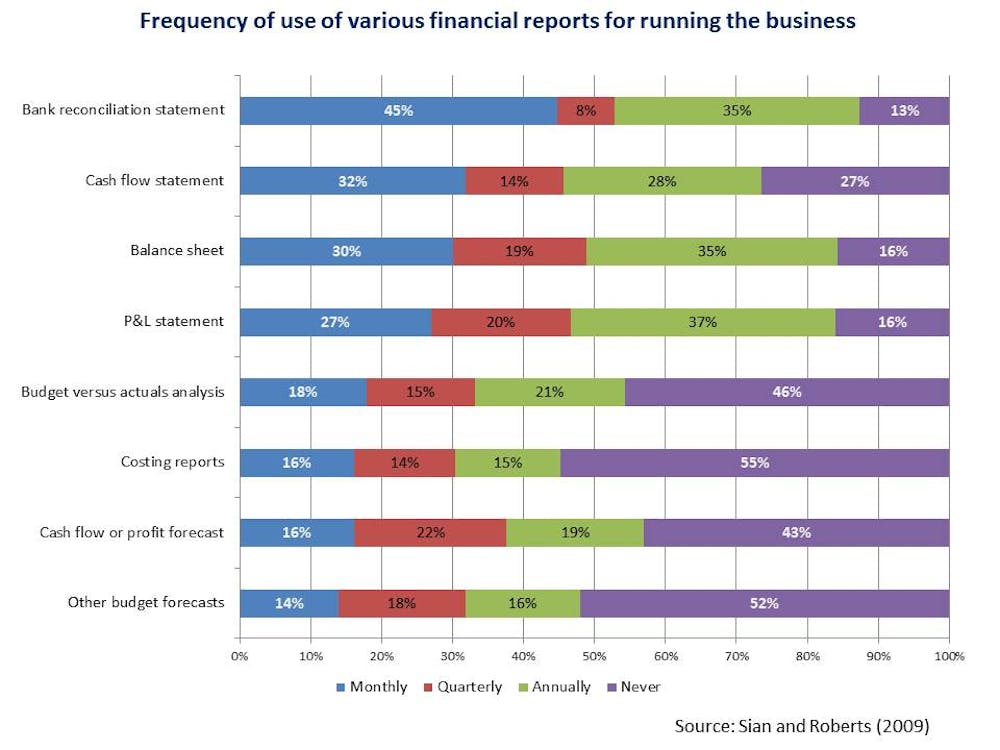

In terms of their use of financial reports as tools to help them manage their businesses the study found a high proportion of owner-managers who made relatively little use of financial analyses. As shown in the following chart, most owners reported making some use of bank reconciliation, cash flow and P&L statements along with their balance sheets. However, cash flow budgeting, costs analyses, cash flow and profit forecasting and similar systems were not used at all by 43% to 55% of owners.

The accountants who were surveyed reported that the most important use made of financial reporting was to look backwards at historical performance rather than using them to help manage the business going forward. Around 84% of the accountants reported that they used financial statements to examine how their client’s business had performed during the previous year. However, only 39% felt their small business clients used financial information as a tool to improve their firms’ financial performance. The use of financial reporting by small business owners for cash flow management was reported as important by only 19% of accountants.

In their conclusions, Sian and Roberts suggest their findings show that the majority of small business owner-managers have low levels of financial awareness and little formal training in accounting or management skills. They note that this has implications for authorities such as taxation agencies who may require small business to keep and maintain financial records. Faced with this compliance work the majority of small business owners seek help from their accountants, but this is driven primarily out of necessity in the preparation of taxation returns or VAT/GST reporting.

According to this study while most small businesses appear to produce the standard financial reports of balance sheet and P&L statement, most do not produce cash flow statements. This should ring alarm bells for those concerned with the survival and growth of small firms. The data suggests that many owner-managers not only don’t produce cash flow statements in their formal reporting, only a small proportion review them more then monthly. Further, around half of these small business owners were not actively engaged in cash flow forecasting or cash budgeting and appeared to rely on their bank statements and annual reports for running the business.

Taking the complexity out of financial reporting

These two studies highlight the reality that most small business owner-managers find financial management an often difficult and complex aspect of their daily business activities. While they recognise its importance, most lack the time, skills and knowledge to set up and run more than a rudimentary performance measurement system.

The benefits of good financial monitoring and control systems, in particular those that can assist with forecasting profitability and cash flow requirements, are clear. However, there is often a significant gap in how most small businesses operate and where these systems should be. Accountants can play a key role in helping their small business clients set up such systems and many do this. Nevertheless, for many owner-managers the main use of accountants is to undertake tax compliance work looking back at the past year rather than seeking ways to operate the business more profitably into the future.

With most small businesses now making use of computer-based accounting software it should be possible for better financial reporting and management systems to be implemented. These should not only provide support to taxation and GST compliance, they should enable the owner-manager to get timely and reliable information upon which to base future decisions. Such functionality is now being built into these accounting packages, and it is to be hoped that accountants take the time to help their small business clients establish appropriate reporting systems. It is also hoped that their small business clients realise the importance of having these systems and learning how to make best use of them.

Note: Tim Mazzarol is President of the Small Enterprise Association of Australia and New Zealand (SEAANZ).

SEAANZ is a not-for-profit organisation founded in 1987. It is dedicated to the aim of bringing together small business professionals in practice, education and training, and to promote small business development, communication and dissemination of research, ideas and information.