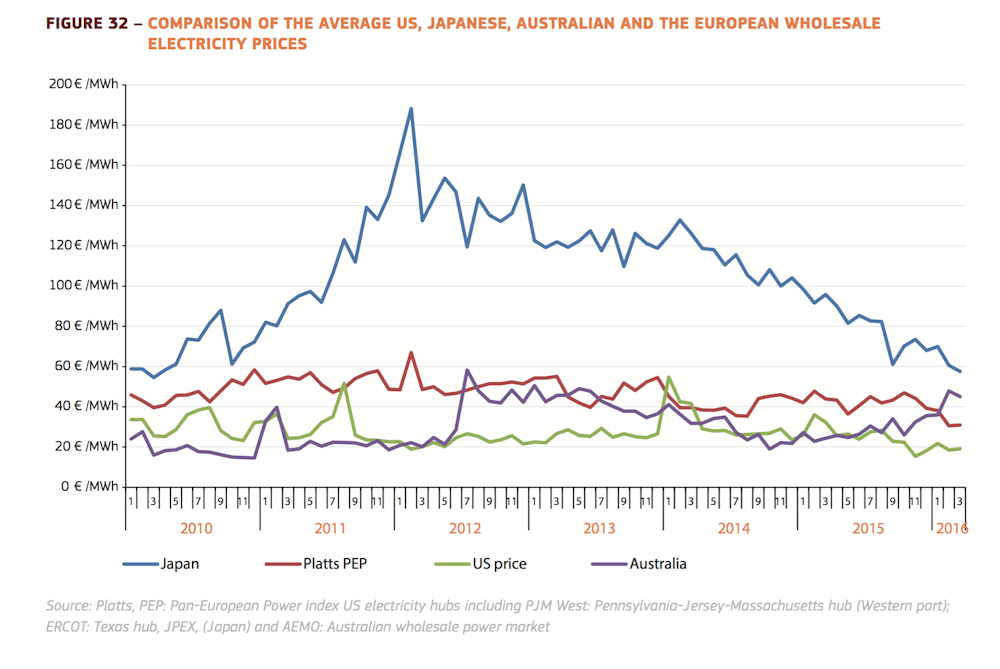

The European Commission’s latest Quarterly report on electricity markets makes sobering reading down under.

Over the last year wholesale electricity prices have been falling just about everywhere across the developed world except here in Australia, where they are skyrocketing.

Australian prices are now above the European average, well above the US and rapidly converging with Japan, which is still recovering from the shock of Fukushima in 2011 when prices rose to over eight times Australian.

With Japan now reactivating nuclear power production, and Australian LNG exporters putting the squeeze on domestic gas markets, it can be anticipated that Australia will soon be top of the price tree. Indeed, with 2016 Q2 and Q3 Australian prices rising at unprecedented rates, it probably already is.

Combined with exorbitant power distribution costs, the alarming trends highlighted by the EC’s report will be exercising the mind of our new Federal Minister for the Environment and Energy, Josh Frydenberg.

How fast are Australian prices rising?

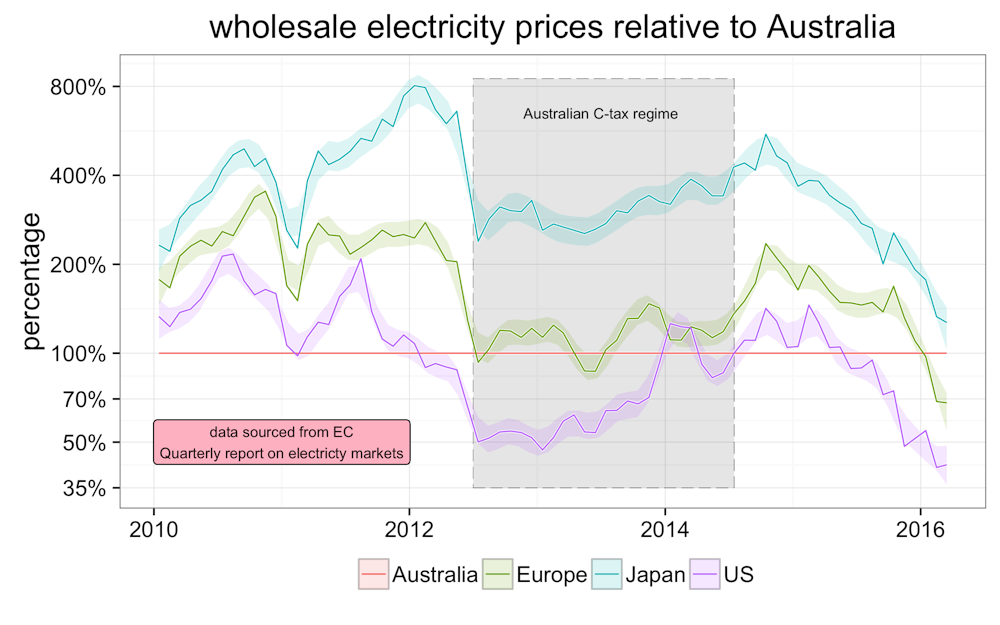

The trends highlighted by the EC’s report are expressed in Euros, so they somewhat obscure local dynamics. In reality, Australian wholesale prices are rising more steeply than ever before, having risen by around 45% over the last year. Prices over the last six months are now higher in aggregate than at any comparable time during the carbon tax period, which added around 50% to wholesale prices in the period 1/07/2012 - 17/07/2014. When the impact of the carbon tax on 2014 prices is removed, prices are up by more than 65% in just 2 years.

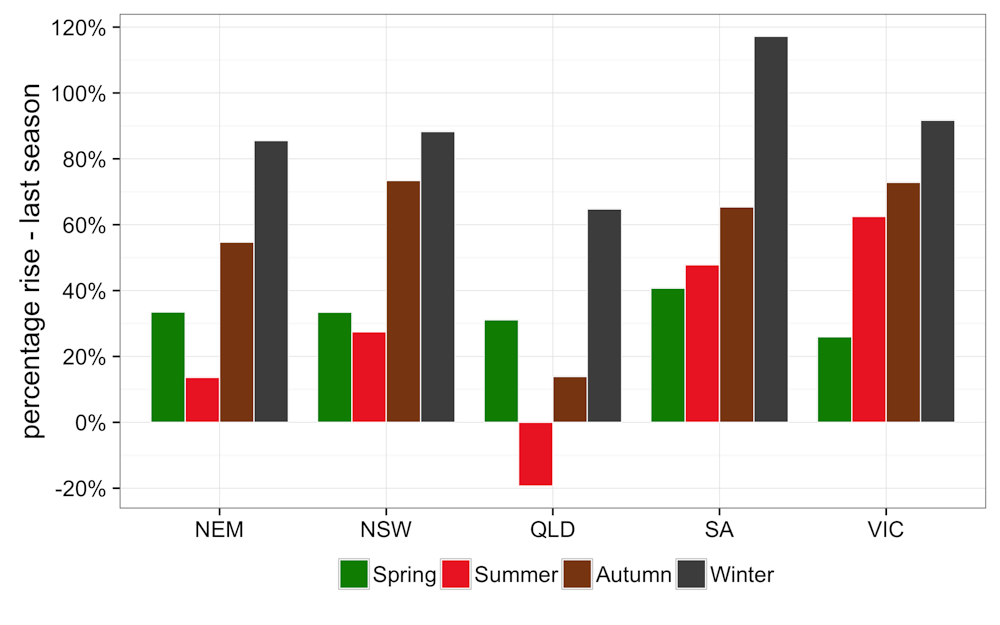

Compared to the same period one year earlier, wholesale prices have risen across all seasons and all jurisdictions in the last year, excepting summer in Queensland. The rate of increase has risen steadily from the spring 2015 through to the winter 2016. For the winter period of 2016, prices were up by an average by 85% compared to the previous winter, with the increase ranging from 65% in Queensland to 115% in South Australia.

Why are electricity prices falling everywhere but Australia?

The reasons for wholesale electricity price falls in Europe and Japan are straightforward.

Both are dependant on imported gas, and with the oil-linked price for gas falling, so too are electricity prices. In the US market, the flood of shale gas greatly exceeds export capacity, so there is a continuing glut of cheap gas [1].

The story in Australia is quite different. Despite a three fold increase in gas production in the eastern states in the last few years, due to the opening up of new coal seam gas (CSG) fields in Queensland, the domestic market is being squeezed as LNG exporters struggle to meet supply contracts.

In the Australian CSG industry it is an open secret that some exporters agreed punitive clauses in contracts should they fail to fill their LNG trains. Despite strong opposition from former industry champions such as John Ellice-Flint, exporters such as Santos stretched themselves on production by committing to two LNG trains. Now gas is being diverted from domestic markets to avoid industry collapse. The consequence is that Australian gas consumers are increasingly subject to scarcity pricing when domestic prices can rise to many times that which international buyers have contracted for the same gas.

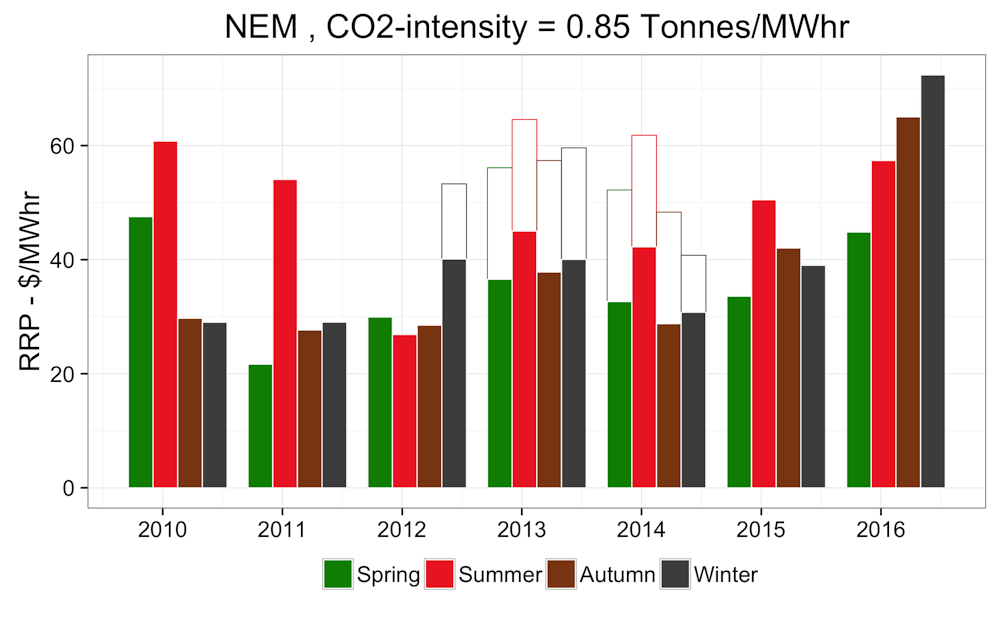

Not surprisingly, steep rises in the cost of gas is causing a reduction in gas use in domestic electricity markets. In Queensland gas fired power output in the winter of 2016 was down about 250 megawatts or 20% on the year before. Meanwhile black coal generation was up 450 megawatts, with Queensland’s CO2-production from the electricity sector increasing by 5%.

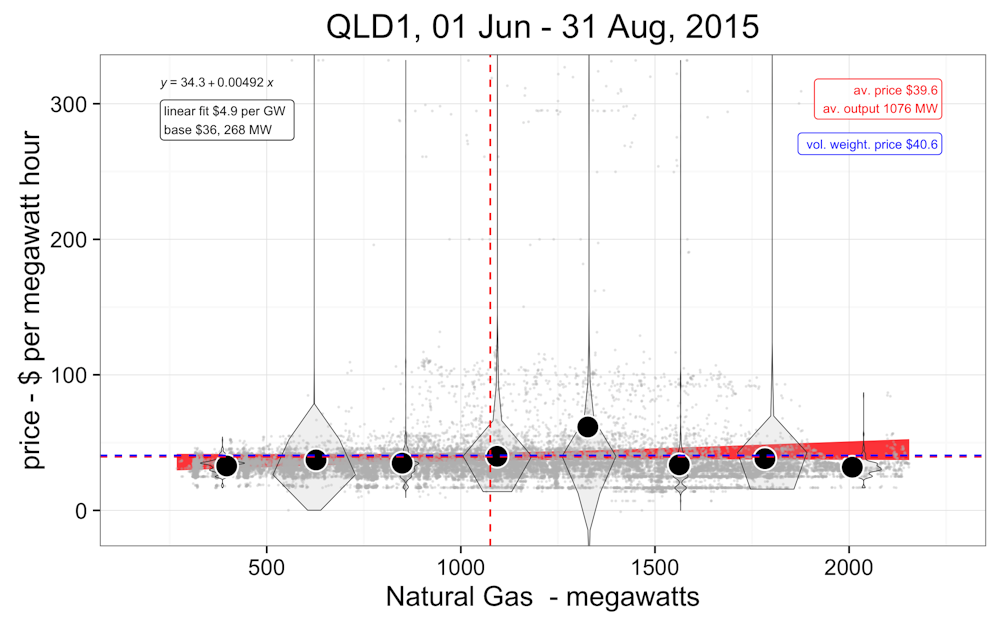

An insight into the impact of the rising cost of gas on our electricity market is provided in the figures below, which show how market prices varied with gas dispatch in Queensland over the winters of 2015 and 2016, respectively. In winter 2015, when gas dispatch averaged 1076 megawatts, there was no correlation between wholesale prices with the amount of gas dispatch, consistent with gas generation being a price taker. Then the average price of electricity was $39.6 per megawatt hour.

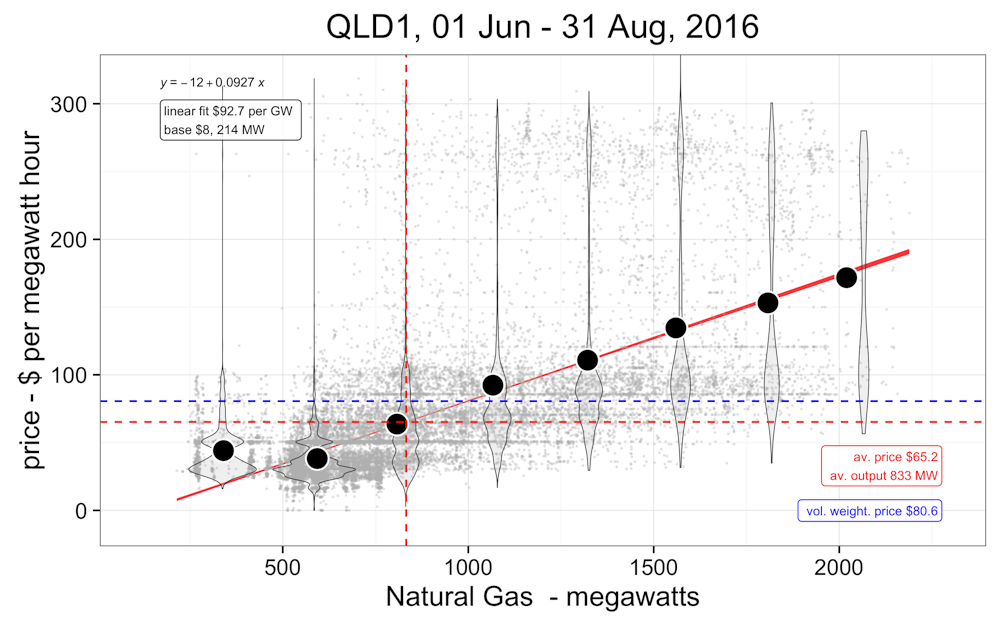

By winter 2016, when gas dispatch averaged 833 megawatts, a strong price correlation had established as gas generators increasingly set the price. Average prices had risen to $65.2 per megawatt hour with spot prices increasing almost $100 per megawatt hour for each additional gigawatt of gas dispatch.

We really need to talk about gas

In 2015, the availability of “ramp” gas made Queensland settings somewhat analogous to the US, where cheap gas increasingly fuels electricity generation. By winter 2016 when more LNG export trains had been commissioned, scarcity pricing was manifesting in our domestic gas markets impacting our electricity market big time.

As the EC’s quarterly market report flags, the historical competitive advantage Australia has had as a cheap provider of electricity has been obliterated in a little over a year. And that is without any carbon tax. It is hurting most severely in South Australia which has always been more exposed to gas prices than other states by virtue of its limited coal reserves.

While several compounding factors have played out in extreme electricity price rises in South Australia, as discussed in my last post, the broader rises across Australia have their underpinnings in the rising domestic gas market prices as well as contractual arrangements in gas piping. The smoking gun is the recent steep rise in Queensland electricity prices - a market that remains essentially a renewable free zone.

The damaging reality of the situation is highlighted by a recent post on the tech website Whirlpool

- “We are a business in SA [South Australia] with high usage (use up to 14MW), on spot pricing since June 1st – and are turning everything off when a spike hits – but the last 5 minute spike was at the end of the half hour pricing cycle (price is averaged in half hour periods). We just chewed through $75,000 worth of power in a half and hour! (we are used to paying $1000). This period while the interconnector is down could effectively burn about 3 years of profits in 4 working days if the forecast prices come to fruition.”

One might ask why such energy users exposed themselves to spot (wholesale) pricing (the norm is via the contract market). Whatever, the cautionary is that 14 MW represents 1% of average South Australian power consumption. Ten such business at threat of going under would be devastating, with potential to reduce South Australian electricity demand by 10%.

The horse has bolted, so what next?

The EC’s quarterly market report was already flagging in Q1 2016 that Australian electricity production was expensive by international standards. Since then, further steep price rises across the NEM in autumn and winter 2016 have further exacerbated price differentials, surely now placing Australia amongst the most expensive producers of electricity in the world.

No doubt the gas lobby will absolve the industry from any responsibility for the recent events that have transpired on our electricity markets, arguing the solution lies in even more gas production, and that renewable energy policies are more to blame.

To be sure, eastern Australia is short on supply of cheap conventional gas from the offshore Gippsland Basin and a few other locations. Expanding the gas base by exploiting unconventional resources such as CSG was always going to come at a price, since such resources are inherently more expensive.

But developing the new CSG fields at such scale was always going to risk that production would fall short of targets. As much was acknowledged by the joint Department of Industry and Bureau of Resources and Energy Economics study into Eastern Australian gas markets

The current development of LNG in eastern Australia and the expected tripling of gas demand are creating conditions that are in stark contrast to those in the previously isolated domestic gas market. The timely development of gas resources will be important to ensure that supply is available for domestic gas users and to meet LNG export commitments. Such is the scale of the LNG projects that even small deviations from the CSG reserve development schedule could result in significant volumes of gas being sourced from traditional domestic market supplies

The hope is that the events of 2016 are transients, related to temporary development schedule difficulties. If they are not, then god help domestic consumers, not just those exposed to electricity prices but also right across the gas sector. A broader question for our gas exporters is just how much risk from any such development schedule difficulties is appropriate to defray onto domestic consumers? As the Eastern Australian Gas Markets Study highlights, it is not as though such circumstances were not anticipated.

In prosecuting the case to deliver more of our national gas resources to market, perhaps it is not too much to ask that domestic gas consumers are offered some insurance against any further development schedule difficulties incurred by our exporters? After all, it is our gas.

Domestic reservation, anyone? - at least while transitional issues work through the system.

Notes

[1] Shale gas economics in the US is linked to co-produced liquids, and thus differs markedly from the CSG fields in Australia where there is no liquid hydorcarbon production.