We have got used to living with the productivity puzzle but the labour market figures released today now add a labour market conundrum. The total number of people in work fell by nearly 70,000 comparing the three months to May 2015 with the previous three months – the first significant dip in the figures since 2010. But why? We would normally associate sharp falls like this with the onset of recession, and there is absolutely no sign of that.

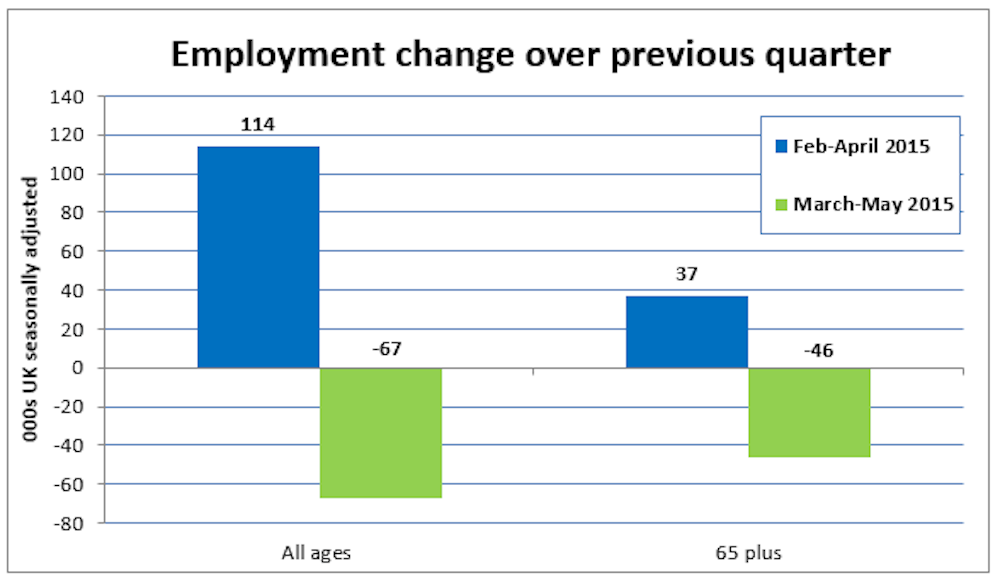

The main drivers of the decline were fewer people in self-employment and fewer employees in part time jobs. The number of employees in full-time jobs went up and so did permanent employment, albeit very slightly. The labour market had been growing strongly in recent months. Indeed, in the three months to April 2015 total employment went up by 114,000. So it looks as though something fairly dramatic happened to employment between April and May.

We would expect GDP growth to start to slow in line with the budget forecast – and growth may have slowed more than expected in the period to May. Another possibility is that some employers, especially those with public sector contracts, postponed recruitment in the run up to the May election given the unusually high level of uncertainty about the outcome. Public sector employers may have accelerated job cuts at the start of the financial year. This combination might be enough to explain the fall in employment.

Older workers

However, when we see a sharp shift like this in the labour market without an obvious macro-economic explanation, then more often than not it is due to a policy change. My money is therefore on older workers leaving the labour market, encouraged by the ability of people to use their pension savings more flexibly from April 2015.

We know that outflows from self-employment have been unusually low in recent years and that a much higher share of self-employed workers are in their 60s than employees. It would be no surprise that as outflows return to pre-recession rates, some of these older workers who had postponed exit and have reached or exceeded “normal” pension age have now decided to retire. This might also explain the sharp drop in part-time work, as some of those approaching and beyond pension age prefer to work part-time rather than full-time.

There was a very marked fall in the employment of those over 65 in the latest figures – down by nearly 4% compared with a fall of 0.1% in those of “working age” (between 16 and 64). In the previous figures covering the three months to April, employment among those over 65 went up by 3.3%. This is part of a long-run upward trend which had seen employment for this age group increase by 15% in the past two years to April 2015 compared with 4% in overall employment. The sudden reversal of this upward trend is dramatic.

Put another way, in May 2015 those over 65 represent less than 4% of all those in work, but accounted for nearly 70% of the overall decline in employment in the three months to May compared with the previous three months. The chart below shows the changes over the previous quarter in thousands for the three months to April and the three months to May respectively.

Slow recovery

If this proves to be the explanation, then the impact is likely to be temporary, a one-off adjustment in response to the implementation of the April pension reform, coinciding with a period of more cautious hiring among some private sector employers. The next set of labour market figures should be better and concerns that the recovery has moved seriously off course can be set to one side.

Nonetheless, even if we allow for these one-off impacts, the underlying state of the labour market is still much weaker than it was. Had employment for the over 65s not changed we would still have seen little if any employment growth. It is very likely that a combination of weaker growth and faster productivity will mean that future jobs growth will be much slower than we have previously seen. We may also see a further recovery in wage growth, although the latest figures showing no change are not very encouraging.

The new government has announced some ambitious plans – not only a National Living Wage, but significant increases in the employment rate and major reductions in the unemployment rate for young people. These may still all be achievable, but the going has suddenly got harder. The plans for the NLW imply annual increases of between 6 and 7% between now and 2020.

The risk is always that such an aggressive policy will lead to job losses - indeed, the government has accepted there will be some, albeit on a modest scale. The risk of job loss would be much less if the policy was introduced in a labour market with strong growth in both jobs and wages. In the absence of either progress towards the desired NLW of 60% of median earnings may have to be more cautious than planned.