Governments and donors have tried hard to improve dairy farming in sub-Saharan Africa in recent years. Many recognise that it has much potential to boost the economic situation of poor farmers in the region. And unlike many other products such as cut flowers or mange tout, it tends to supply local consumers rather than people in other countries. This means that making it affordable has implications for local health, spending power and so forth.

Yet so far, any notion of a “white revolution” in milk production remains far from reality. To understand what is holding it back, I undertook a three-year research project into dairy farming in Malawi. My findings suggest that those who want to improve the sector need to look more closely at how the produce gets from the farm to consumers’ kitchens.

Milk from A to B

Most of Malawi is suitable for dairy farming, but approximately 90% of commercial milk production is located in Southern Region in the Shire Highlands, a major area of agricultural production on a plateau east of the Shire river. Most of the rest of the country’s milk production is in Central Region, with a remnant in the north.

Raw milk production in Malawi is mainly undertaken by smallholder farmers with typically one to two cows. The number of farmers seems to fluctuate between around 5,000 and 7,500, who produce 80%-90% of the country’s milk between them.

Cows are milked once or twice a day. The amount produced by each cow depends on the animal breed and the feed. Crossbreeds, which are the most common cows in the south, yield between six and 11 litres per day; while pure-bred cows produce between 16 and 30 litres.

Farmers usually deliver the milk by pushbike or on foot to the local milk station – known locally as the “milk bulking group” (though sometimes they sell quantities along the way informally to street vendors). From here it is picked up roughly every second day by the local processor in a refrigerated truck, though the rainy season and poor roads sometimes get in the way.

The milk station pays farmers at the end of each month, based on the amounts delivered that they record in their copybook each day. The price per litre is set by the processor, deducting a small amount to pay for the operation of the milk station.

Of the milk that gets processed, approximately 33% is pasteurised to serve the urban market. About 50% goes to ultra-high temperature (UHT) production, which provides a much longer shelf-life and is suitable for sale in rural areas. The remaining 17% goes to other products like yoghurt, chambiko (fermented milk) and butter.

Dairy products are mostly distributed through supermarkets and small retailers, though some processors also employ street vendors. Particularly in poor or rural areas, consumers will also buy raw milk from the streets.

Milk prices

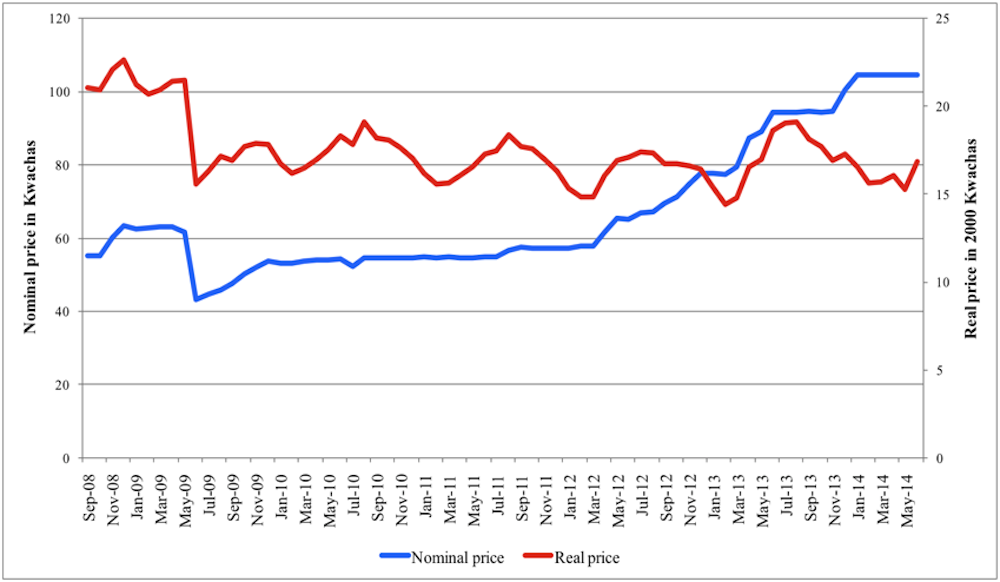

Just like any economic activity, dairy needs proper returns if it is to expand. Malawian milk prices shift sporadically, as can be seen from the figure below (real prices red, nominal prices blue). In a country with an annual inflation of above 20%, any rise in the actual price is quickly eroded.

The implications of low prices are quite clear. Brian Lewis, an advisor to the Shire Highlands Milk Producers’ Association, told me that the main driver for improving farming in the area was the milk price. “When the milk price is good, farmers want to produce,” he said. “They feed their cows better, get their cows in calf quicker, everything works. There’s money to pay for veterinary bills, to rear the heifers properly.”

“When the price of milk is poor, everything is the opposite. Farmers don’t want to spend money on treatment for their cows, so the cows don’t do very well, the heifers grow in four years instead of two years, the cows are producing eight litres instead of 15 litres after they calf. When the time comes to do AI [artificial insemination], and they say I cannot afford it … the fundamental thing is money.”

Processor and supermarket problems

The whole supply chain is hindered by poor milk quality. The bacteriological level of raw milk is generally high and as a result the milk sours quickly. This is due to unhygienic production conditions; farmers using poor quality water to clean and dirty containers to carry the milk to the stations; and also adulteration. The milk stations do test for adulteration with water, but problems still remain – along with adulteration by bicarbonate of soda to help the milk pass another test for sourness.

Evidently there are opportunities for profiting by lowering the standards. For instance, new milk stations open which are less stringent on quality. Farmers shift to them because they accept more water for the same price. And processors always agree to take the milk even if they have an existing milk station next door for fear that if they do not, one of their competitors will. Yet processors throw away 17% of raw milk on the grounds that it is not fit for processing. That is a large drag on their costs, which is not good for prices.

Then there are the supermarkets. I was involved in an analysis last year of supermarkets and smaller retailers in the two main Malawian cities of Lilongwe and Blantyre, which found that retail margins on dairy products fluctuated between 13% and 149% – even though the margins recommended by processors were between 12% and 22%.

The highest retailers’ margins we found were on 250ml bags of pasteurised and ultra-pasteurised milk – products that are targeted at low-income consumers and therefore particularly important for food security.

What does this tell us?

When specialists analyse the Malawian dairy sector, they tend to conclude that there is not enough supply of milk. I would not disagree. Undoubtedly there is the need to increase milk productivity.

To solve this problem, investors and donors tend to focus on the supply side. Examples include increasing the number of cows; replacing the cows for ones with higher yields; improving the quality of feed; subsidising feed; and educating farmers on better practices to improve the quality of milk.

But look again at the price graphic further up. If we agree there is not enough milk, you would expect the laws of supply and demand would push the price higher. Since the graphic shows that this is not happening, and certainly not when you take inflation into account, it suggests the dairy supply chain does not operate properly.

My research tends to agree. It indicates that producer prices are being held back by a failure to properly enforce quality standards and to make sure the retail price is passed down the supply chain. Without this, any investment in farming practices is unlikely to reap dividends.

This point is likely to be applicable in many farming sub-sectors not only in Malawi but across southern Africa. It is always tempting to allow impressive progress in agricultural technology such as new seed varieties or on livestock genetics and their potential for boosting productivity to overshadow other more basic needs for developing farming in the region.

But if you don’t deal with problems in the supply chain, smallholder producers are unlikely to benefit from direct investments. Ultimately this will not have the expected impact on reducing poverty, generating growth and improving food security.

This is not to say that new technology and other direct investments should stop. It is rather to highlight the fact that supply chain reform needs to happen first. Otherwise the prospect of a white revolution in Malawian dairy farming and equivalent advances elsewhere will remain out of reach.