The causes of the crisis that engulfed the global economy and its financial markets were not special or unique, even though the consequences were unprecedented for most of us. It is true that this crisis had some unique characteristics, in particular the role that credit derivatives played in inflating the credit bubble. But in the end the main cause was all too familiar: too many greedy bankers lending too much money to too many people who could not afford to pay them back.

Much of this lending was secured against property; property that kept going up and up in value. With collateral like that why should any self-respecting, greedy banker care whether the borrower could service their debt? As long as you could sign your name (although a thumb print would do) they would lend you money to buy a house. Everyone was a winner. Until the property bubble burst, first in the USA then in bubble economies like Spain, and Ireland. The rest is history.

But how can we know when property is overvalued? Greedy bankers certainly don’t seem to be able to spot a property bubble. The truth is that nobody can know for sure when an asset class is in bubble territory. Asset price valuation is art not science.

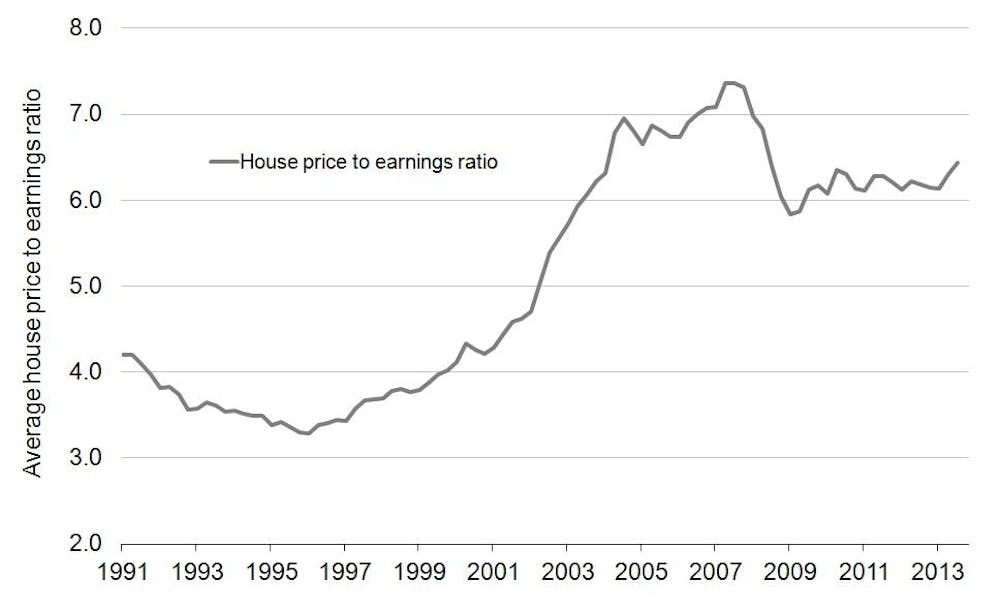

However, there are some indicators we can use that clearly hint at bubble conditions. The chart below shows one such indicator for the UK economy. It is the house price to earnings ratio (HPER), which I have created by dividing the average UK house price by the average UK salary. It is currently around 6.5 which means that the price of the average UK house is six and a half times the average salary.

The average for this indicator in the 1990s was about 3.5. It peaked in the halcyon summer of 2007 at just under 7.5. So why are Brits still willing to pay six and half times their salary for a house today, when they were only willing to pay three and a half times their salary in the 1990s?

Is it because people think that their earnings prospects are so fantastic today that spending so much money on a house, relative to their salary, is worth it? Or is it because they believe that house prices will rise so rapidly from here that it is an investment worth making? Either of these explanations would help to bring down the ratio, perhaps to pre-bubble levels.

But real earnings growth has been negative for many in past years, and few believe that it will be very different over the next few years. So maybe people think that capital gains on their homes are, once again, a surefire bet? The government has encouraged this view, by stoking up the housing market with its idiotic “Help to Buy” scheme, a policy that is akin to giving a recovering alcoholic a bottle of whisky as a reward for staying off the booze for a while.

As the chart shows the UK’s property market, relative to household income, has corrected. But not by much. By nowhere near as much as the corrections seen in other bubble economies. And as the UK’s property market participants have begun to swig from the bottle handed to them by the government, rather than deflating, the chart shows that the bubble is inflating once again. It will end in tears eventually; asset price bubbles always do.

In early 1990 (not shown on chart) the UK’s property market peaked, with buyers paying close to six times their earnings. Back then, rising interest rates triggered a catastrophic fall in house prices as the economy plunged into recession.

Today interest rates are virtually zero; any significant increase up to the historical norm could have a similar effect on house prices. So once UK rates do start to rise, investors would be well advised to steer clear of any investments that are exposed to the UK’s bubble-prone, residential property market.

A version of this article first appeared on Cass Finance Blog.