A recent report by the Organisation for Economic Co-operation and Development (OECD) into the financing of high growth firms highlights the important role played by angel investors or business angels. The term “business angel” is thought to have its origins in New York’s Broadway musical scene. Producers who wanted to launch a new show would receive investment funding from wealthy “up-town” patrons of the theatre who would come “down-town” like angels to invest in these risky ventures.

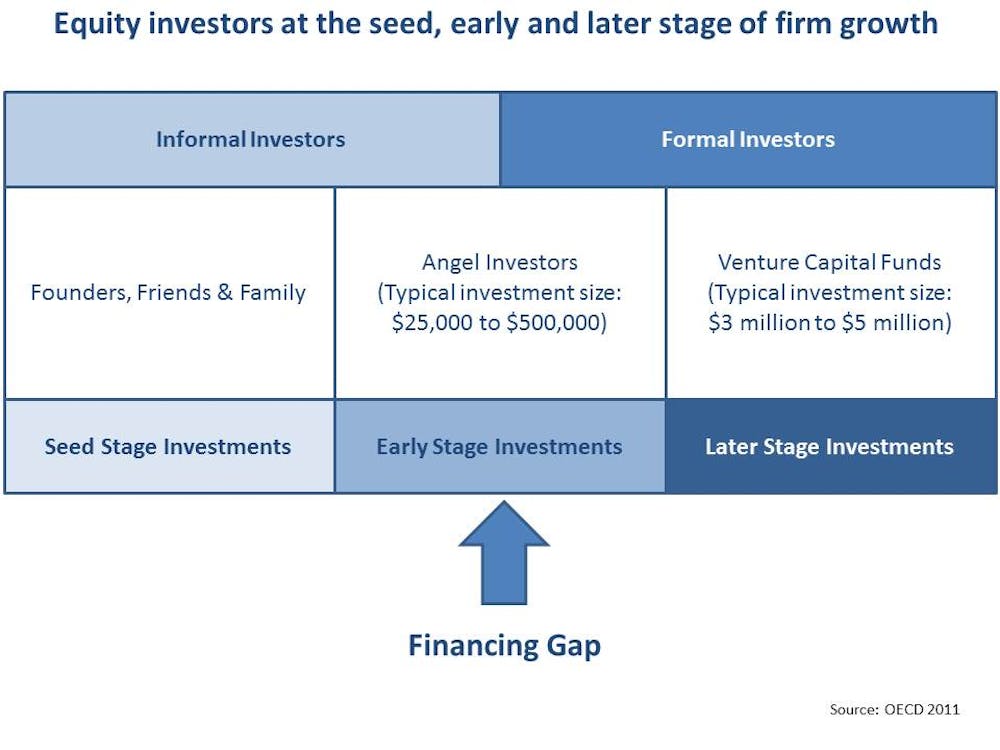

Today business angels are a major source of venture capital financing that helps to fill a gap that lies between the start-up and seed capital stage (i.e. typically less than $25,000), and the point at which formal venture capital funds will take an interest (i.e. typically above $3 million to $5 million). This is shown in the following diagram.

Another OECD report, published this year, into emerging trends in the financing of small to medium sized enterprises (SMEs) and entrepreneurial ventures found that the Global Financial Crisis (GFC) had impacted severely. Bankruptcy rates increased significantly and there has been a severe contraction in the availability of bank financing. While large firms were able to secure financing via such means as bond markets, most SMEs were restricted to the banks. In some countries such as Hungary, South Korea and Portugal, SMEs comprised between 60% and 81% of the banks total business loans portfolios.

This report also noted a “sharp decline” in the growth of venture capital financing during the period 2008 to 2010, much below the period prior to the GFC. In an earlier article I have noted that venture capital funding has not performed particularly well since the peaks it reached at the end of the 1990s with the “Dot.com” boom. However, the OECD notes that while business angels are potentially important, there is very little data available on them. This is due in part to the informal nature of their investment practice, and also because they tend to prefer to keep their investing activities private.

So who and what are business angels?

Research into business angels is relatively scant. The definition of “business angel” remains unclear, with the terms “business angel”, “informal investor” and “informal venture capital” all used interchangeably. In an interesting paper on business angels published in the journal “Strategic Change” in 2009, Veland Ramadani notes that companies such as Bell Telephone, Ford Motor Corporation, Apple Computers, Body Shop and Amazon all had business angel funding in their early years.

The typical profile of a business angel is a middle aged male with an above average education and a professional or business career background. Most have experience either in running their own companies or managing businesses and organisations. They also have high personal net worth.

In the United Kingdom business angels have been found to invest an average of £10,000 per deal and to hold a portfolio of around two to five investments. Research undertaken in Australia suggests a similar profile. The average Australian business angel is a middle aged male with a personal net worth of around $2 million and an annual income of more than $180,000. They invest an average of $200,000 in new business ventures and hold around 10% to 14% of the capital in these ventures.

Among the features that distinguish business angels from more formal venture capital investors is the personal nature of their investments. Business angels invest their own money and therefore take more significant personal risks with their investments than the managers of venture capital funds. They also tend to invest close to home, with most investing in ventures that are within their local community, typically within a distance of 1 to 2 hours of driving time from their home.

Business angels also prefer to invest in privately held business ventures that have not been quoted publicly on the stock market. The high risk nature of their investing is fraught with potential failure and they are usually keen to keep any investment activities private. They generally invest around 5% to 15% of their assets into new businesses and seek rates of return of between 20% and 30% from their investments.

What does the research say about business angels?

A study by Cheryl Mitteness, Richard Sudek and Melissa Cardon, published this year in the “Journal of Business Venturing”, suggests that business angels rely upon personality characteristics of the entrepreneur when making investment decisions. Entrepreneurs who display high levels of passion for their venture may get a more favourable treatment by business angels. However, the study also suggests that differences can be found depending on whether the business angel is older or younger (older people being more likely to view passion favourably), and their level of creative or intellectual capacity.

Their study suggests that entrepreneurs seeking to impress a business angel investor should do their homework on the people who they hope to make their pitch for capital to. They should also seek to inject a sense of passion into their presentations and look for cues from the investors that suggest they are responding favourably.

In another study by Andrew Maxwell, Scott Jeffrey and Moren Levesque, published in the “Journal of Business Venturing” in 2011, it was found that business angels make investment decisions based on a set of heuristics. These tend to eliminate proposals based on eight broad criteria. The first four of these include the willingness of the market to adopt, the status of the new product’s development, how protected the intellectual property is, and how likely the customers will be to engage. The second four factors are the route to market for the business model, the potential of the market for growth, the relevant experience of the management team within the venture and the soundness of the financial modelling.

An earlier study from the Journal of Business Venturing published in 2002 by Colin Mason and Richard Harrison, suggests that most business angels hold onto their investments for around 4 years. They generally seek to exit from their deals by trade sales not IPO. As mentioned above, they select deals for investment more as a process of avoiding making bad decisions than trying to pick winners. Compared with formal venture capital funds managers, business angels make fewer investments that lose money, but they often make a significantly higher proportion of investments that either break-even or generate only modest returns.

How much value do business angels provide?

Although the amount of available research on business angels is limited there have been some recent studies published. A paper by Stephanie Macht and John Robinson, published in the “International Journal of Entrepreneurial Behaviour & Research” in 2009, examined what benefit business angels provided to their investee companies.

This study found that they were generally helpful in overcoming funding gaps for fast growing small firms. They also assisted the management of such firms with knowledge and experience by providing time on the firm’s board. In addition, these angels were useful in their ability to help widen the range of contacts and networks that the firm needed to secure additional capital and follow-on financing.

According to the OECD review of the role played by business angels, a major contribution is their ability to bridge the gap between the seed capital and later stage investments. If they do their job well the business angel can help a fledgling firm build up its balance sheet, managerial competencies and strategic networks.

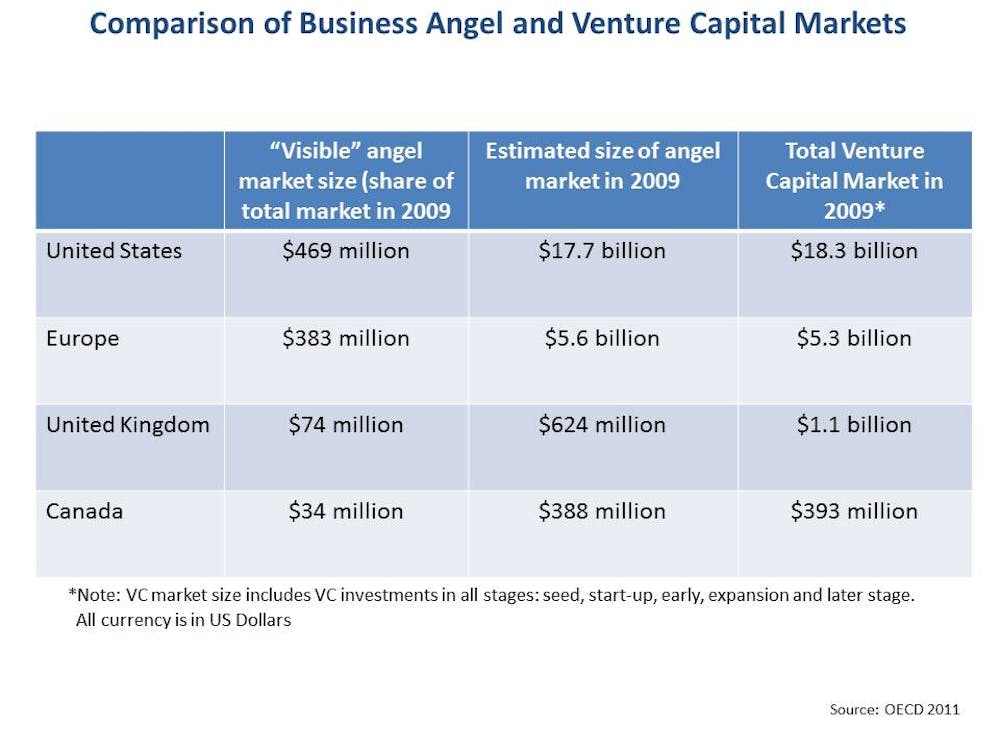

Estimating the value of business angels is difficult due to a paucity of reliable data. However, as shown in the figure below, the overall size of the business angel investment “market” is quite large. This data is from the OECD and shows the “visible” angel market and the estimated total angel market in 2009. These figures are for the United States, Europe the UK and Canada. It is clear that even if only the “visible” part of the market is accepted as reliable, the total contribution of angels to funding early stage ventures is significant.

It is also worth noting that business angels have been particularly active in funding some of the more risky new technology ventures. Key areas include information and communications technologies (ICT), biotechnology and health technologies, and clean technologies.

What about angels in Australia?

The business angel market in Australia is difficult to map due to the lack of readily available data. According to the OECD the first business angel group identified in Australia was established in Melbourne in the 1980s. This failed to take off due to the lack of interest by the business community at the time.

During the 1990s there were a number of state and federal government initiatives to help foster business angel networks. This included the “Business Equity Information Service”, that aimed to help match angel investors with deals. This service ceased to function in June 1997. The Productivity Commission (then known as the Industry Commission), had investigated the business introduction service and concluded that there was no need for public subsidies for such services.

A number of business angel programs were set up around Australia in the past decade. Some of these were facilitated by state governments and others were private initiatives. In 2006 the federal Department of Industry, Tourism and Resources commissioned a report entitled “Study of Business Angel Market in Australia”. This report surveyed the known business angel market and suggested that some two-thirds of angels were not part of any formal angel networks, and did not wish to be.

It also recommended that there was a need for better education of entrepreneurs to increase the number of “investment ready” opportunities. In other words, it was not a lack of funding that was holding back entrepreneurial ventures, it was the lack of well-considered business models by those entrepreneurs seeking funding. The report also recommended business education courses for entrepreneurs, academics and university students in the process of business angel investing.

The most visible business angel network is the Australian Association of Angel Investors Ltd (AAAI). This was founded in 2007 as a not-for-profit company with the purpose of providing a nation voice and focal point for the angel investor community. According to the AAAI, in 2010 business angels in Australia had invested around $1 billion in 5,000 early-stage businesses, which created an estimated 25,000 jobs.

A key issue for business angel investment is to get angel investors to work collaboratively and join into investment groups and syndicates. However, many angel investors are private about their deals and getting them to work via such formal networks can be difficult.

Overall the business angel is a valuable part of the venture financing environment. Their capacity to bridge the funding gap is a critical role. Further, their willingness to invest locally and in many cases mentor novice entrepreneurs is a valuable contribution. This “psychic capital” is often viewed as being of as much importance as the financial capital they provide.