Since almost immediately after his inauguration as 45th president of the United States, Donald Trump has been claiming credit for what he sees as a miraculous recovery in the nation’s economy. Barely a day goes by without a tweet trumpeting a new jobs deal or the strength of the US stockmarket.

But how much credit is actually due to his administration? Incoming governments have a tendency to claim merit for post-electoral improvements in the economy and to blame their predecessors for worsening conditions – but how long does it really take for any policy changes to work their way through the system?

In a recent tweet, Donald Trump emphasised the increasing strength of the US economy, based on different indicators.

Here, Trump is referring to the S&P 500 Index and the newly released February 2017 Consumer Confidence Survey. The Standard & Poor’s 500 Index (S&P 500) is commonly accepted as an accurate indicator of equity performance, being based on 500 stocks selected by analysts considering a number of factors such as market size and sector weight.

The S&P 500 has gone up by 3.8% since Trump took office. And that’s great – but the S&P 500 has been rising since before the November 8 election and, notably, was also rising when polls were favouring Hillary Clinton as the next US president. The most recent data on the very same index also shows that it is now moving downwards – after peaking at 2395.96 on March 1 it fell over the following days, closing at 2362.98 on March 8. Given its volatility, it is difficult to extract from this a clear signal of performance.

Consumer confidence is measured via the Consumer Confidence Index, which is published on the last Tuesday of every month. The analysis of the survey data shows that consumers’ confidence increased in February and remains at a 15-year high, reflecting improved expectations regarding the short-term outlook for business, and to a lesser degree jobs and income prospects. That said, the Consumer Confidence Index showed a moderate decline in January.

Jobs, jobs, jobs

Here, the president is referring to the March 2017 LinkedIn workforce report, showing that the “hiring rate” across the US was 1.4% higher in February 2017 than in February 2016.

Some caution needs to be applied here, as the “hiring rate” considered in this report is calculated as the percentage of LinkedIn members who changed the name of their new employer on their profile the same month they began their new job, divided by the total number of LinkedIn members. The report shows that this “hiring rate” has been on the rise since December – but it has fallen since January, and, considering the past two years, it has exhibited higher peaks during Obama’s term.

If we consider the Business Confidence Index (BCI) provided by the OECD and based on enterprises’ assessment of production, orders and stocks, as well as its current position and expectations for the immediate future, it’s clear that business confidence has been on the rise since the beginning of 2016.

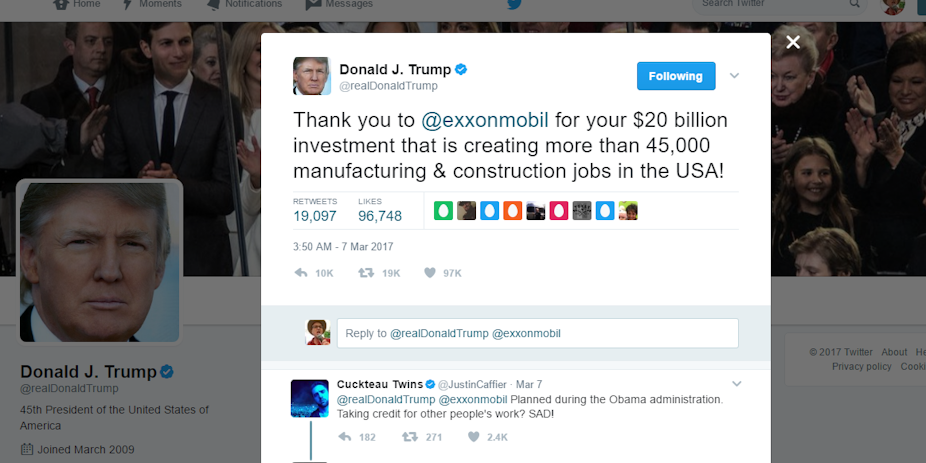

Trump recently tweeted boastfully about Exxon Mobil’s plans to invest US$20 billion over ten years in the US Gulf region to expand its manufacturing and export capacity.

But you need to take this with a pinch of salt. This investment actually began in 2013 and is motivated by the desire to take advantage of the American energy revolution – in fact, it began even before Trump’s announcement to contest the presidential election.

Time lags

Overall, some of these figures represent positive news for the US economy – and it is understandable that Donald Trump is keen to tweet about them, as tweets can move markets. But can he legitimately take the full credit for improved economic conditions?

Economic policy is subject to different types of lags: recognition lags, decision lags and implementation lags. These refer to the time necessary to learn about economic conditions, the time it takes to decide on an appropriate policy response, and the implementation period once the policy is chosen. Empirical evidence suggests that it takes policymakers and legislatures more than a quarter from learning about the economic conditions to deciding what fiscal measures are appropriate, passing them through legislature and actually implementing them.

Then there is the impact lag – the length of time from the implementation of an economic policy decision to when it has an observable effect on the economy. This is generally measured in terms of output.

The magnitude of policy multipliers – that is, the effects of monetary or fiscal policy on output – and the time required to observe the effects of a policy is still an open question for economists. But there seems to be an agreement that the multipliers peak after a considerable amount of time.

One influential study by British economist Andrew Mountford and US economist Harald Uhlig in 2009, which was based on data on the US economy, found that the maximum impact is estimated to occur only after five years.

So while it’s difficult to disentangle the effect of economic policies put in place under the Obama’s administration from the possible effect on business confidence associated with Trump’s announcements, the real test will be to consider the sustainability of such confidence after detailed policy plans are unveiled and implemented by the new president.

It will take patience realistically to assess the impact of Trump on the US economy. And patience is something that Donald Trump lacks, judging by his tweets.