Companies have finished reporting results for the financial year so it’s time to take stock of how the different business sectors of Australia are fairing. In our company results wrap series we take a step back from the short-term focus of quarterly profit and loss statements and examine what big picture factors are at play

The biggest Australian banks are fairing well in a year of increased pressure to reform from politicians, international events like the Britain’s exit from the European Union and more regulation from the Australian Prudential Regulation Authority (APRA).

A number of interrelated factors have contributed to the relatively strong performance of the Australian banks. For instance, the banks have limited exposure to the types of securities which led to massive losses for their counterparts in other countries. The banks also heavily rely on domestic loans, particularly the low risk household sector, so better lending standards and a proactive approach to prudential supervision by APRA may have contributed.

The Basel III regulatory requirements, brought in after the 2008 financial crisis, emphasise holding an increased amount of subordinated debt, as a measure of market discipline. However all the big four banks are holding less and less subordinated borrowings. More specifically, it declined by more than 50% from 2007 to 2014, according to our calculations.

APRA limits banks’ holdings of higher risk securitised assets, these are loans packaged into securities, to a maximum of 25% of the banks’ loan portfolio. These are high risk if not properly understood or defined, as happened with United States home loans, blamed for the start of the global financial crisis.

When Australian banks calculate bank capital requirements, they need to fully account for securitised assets. This is a rule from APRA that goes beyond international standards, to reflect the risk inherent in these products.

Inter-bank liquidity tightened significantly with all banks increasing their holdings of Exchange Settlements Accounts at the Reserve Bank, this a form of low risk liquidity. Australian banks have lower interbank deposits compared to their Europe and USA counterparts and are also heavily involved in long term wholesale funding and are required to hold more liquid assets including government debt to deal with liquidity. All of this makes Australian banks less risky in times of crisis because spillover effects from other banks are less likely.

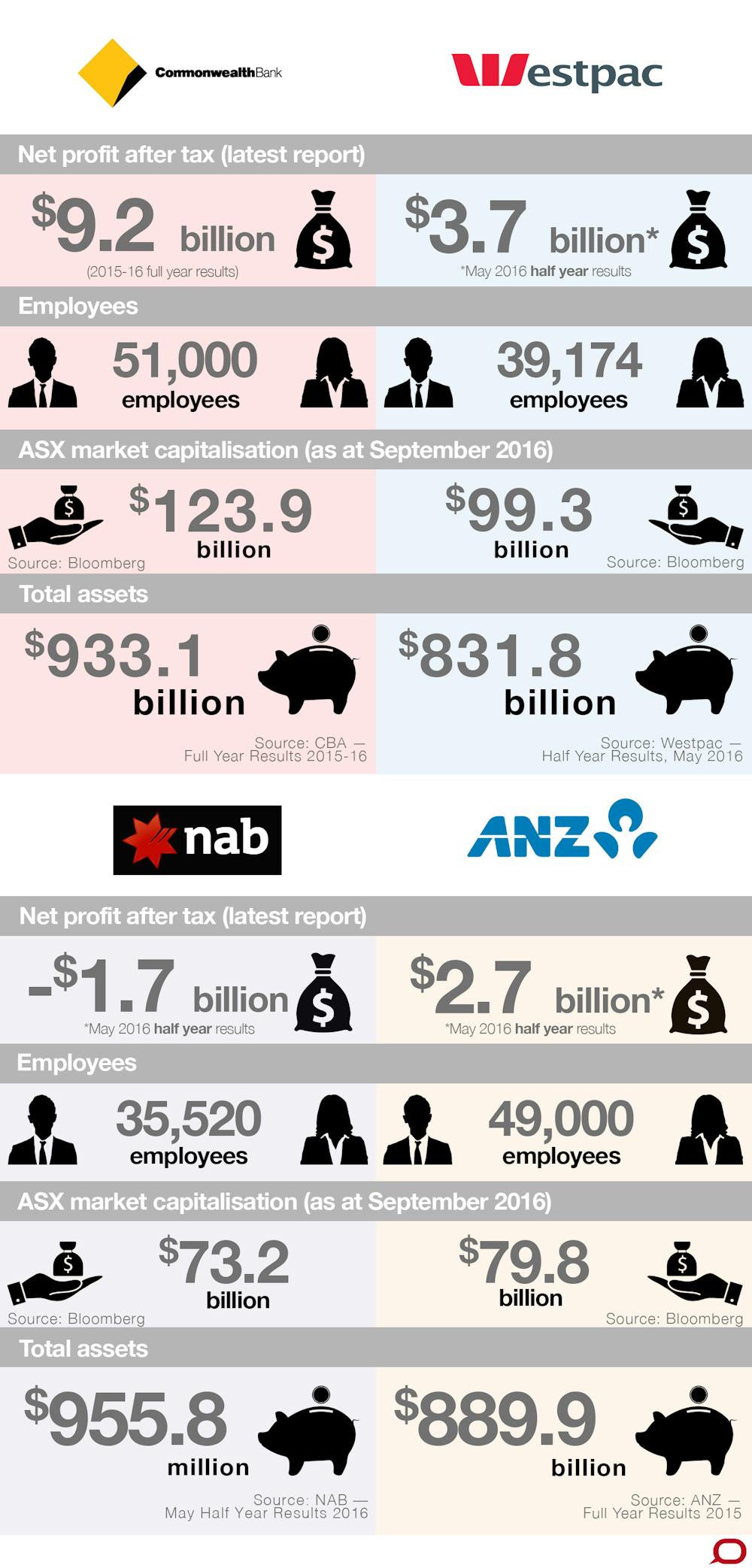

There has been a significant increase in concentration in the Australian banking industry since the global financial crisis. For example with Westpac and the Commonwealth Bank of Australia taking over St. George Bank and Bank West, respectively.

Following mergers, the big four account for 88% of the Australian banking system assets. This reinforces the idea that the banks are “too big to fail”.

The banks have also moved to more fee generating activities, which increases risk, but to a lesser extent in Australian banks. Data shows between 1998 and 2014, on average, 1.2% greater interest income was generated relative to non-interest income for Australian banks, according to our analysis. However, there is also similar evidence for the top eight publicly-listed Canadian banks. They exhibit on an average, a 2.5% increase in net interest revenue relative to non-interest income over the same time period.

This reinforces that Australian and Canadian banks demonstrated extra ordinary resilience during the credit turmoil in the global financial crisis. The World Economic Forum in 2008 reported that Australia and Canada were among the top four safest banking systems in the world.

Large banks in Australia are active in international markets through direct ownership of foreign based banks and having offshore operations as a source of capital. Deregulation of banking in countries such as the USA, Canada, Australia and many developing countries has opened up new markets for foreign banks. Australian banks’ largest international exposure is to New Zealand, where all big four banks retain sizeable operations.

Although the growing interdependence among international economies and financial markets is certain to continue, the impact of Brexit on Australian banks remains minimal. It remains to be seen in the long-run how Australian banks will weather the international banking/economic developments.

As a last measure of the bank health, we can measure the domestic systemic risk with a methodology based on one used by the official Basel Committee on Banking Supervision. Based on July 2016 monthly data, the big four banks account for 80.38% of the systemic risk in the financial system and the riskiest, from highest to lowest, are the National Australia Bank, the Commonwealth Bank of Australia, Westpac and ANZ.