Even before the result of the Greek referendum, it was clear the overwhelming majority of Greek citizens want to stay in the eurozone and see an end to punishing austerity.

In contemplating the options now available to Greece the question is whether her creditors will allow that combination.

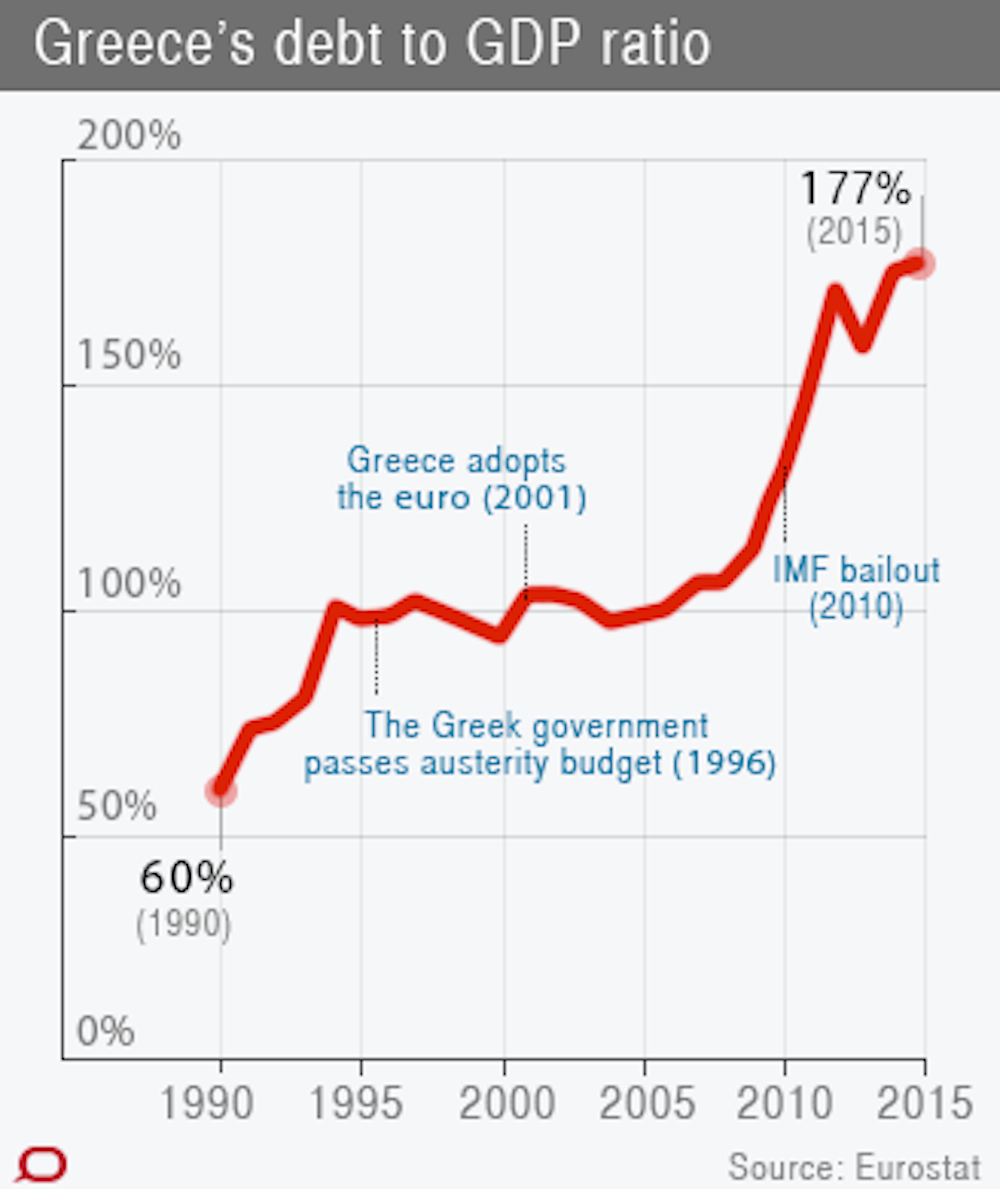

The fundamental economic fact that must be dealt with is the inexorable logic of debt sustainability. For a nation state, this depends upon the trajectories over time of just three sets of variables: GDP growth rates, interest rates on public debt and primary government budget surpluses (budget surpluses net of interest payments on existing public debt) in proportion to GDP.

A viable agreement between Greece and her creditors requires mapping a feasible time path of the ratio of Greek public debt to GDP, by way of credible and acceptable figures for growth, interest rates and budget surpluses. In the course of the Greek crisis to date, the creditors have imposed unsustainable and hence impossible policy objectives on the country. She has been set up to fail, and thereby forced to return as a fiscal supplicant, to receive yet more orders from her creditors. This is a cruel and savage political game, rather like a cat playing with a mouse.

What motivates the creditors? Putting aside stupidity as an explanation (though its role should not to be underestimated), it can be attributed to a particularly vicious approach to moral hazard: punishing bad behaviour so as to deter any repetition (and as a warning to others of “the south”). Perhaps some of this punitive savagery could have been imposed upon Greece’s original creditors. After all, there would have been no buildup of Greek government debt in the absence of willing lenders.

In any case, all rational and impartial observers (including now the IMF) agree the trajectory of Greece’s debt-to-GDP ratio is unsustainable. One way or another it will be changed. A trajectory over time of lower debt relative to GDP would then enable easing the punishing budget surpluses that have been demanded by the creditors, and hence less austerity. Big budget surpluses also compromise economic growth, exacerbating austerity and unemployment – and if GDP grows less rapidly than debt, the debt-to-GDP ratio of course will continue to deteriorate.

All eyes shift to the European Central Bank

Fundamentally, two options are now available to Greece: the creditors agree to a significant debt rescheduling of one kind or another (reduction in the face value of the debt, and/or lengthening its maturity), or Greece unilaterally defaults.

The former is to be preferred but will by no means be an easy path – merely tolerable.

As to the latter, the much-asserted proposition in the run-up to the referendum – that rejecting the creditors’ previous offer was synonymous with choosing to exit the euro – was false. Indeed, there is no intrinsic inseparability between even a Greek unilateral default and exit from the euro. If the default option were chosen and Greece then departed the euro, the latter outcome would be an act of political will, not an inevitable necessary corollary of default.

In the absence of an acceptable deal with its creditors, Greece could default and refuse to leave the eurozone. Since Greece can run a zero or surplus primary budget balance (and no more interest payments to make after default), the government could cover its expenditures, without external assistance.

But the viability of this scenario would depend upon the euro monetary payments system continuing to function in Greece. That would probably be impossible without the support of the European Central Bank (ECB). So long as there is significant uncertainty about Greece staying in the euro, there is motive for substantial depositor withdrawal from the Greek banking system (as is happening already). To ensure the banking system does not become illiquid, the ECB would have to stand ready to provide unlimited liquidity (as it must do right now, if the Greek banking system is not to collapse).

Panic breeds panic and, symmetrically, confidence in Greece enduring in the eurozone would see deposits return to the banks. Such confidence would be engendered by the ECB being prepared to do “whatever it takes” to ensure the liquidity of the Greek banking system.

But would the ECB be prepared to do this? If not, the only way Greece could make up for the lack of liquidity is to create an alternative means of payment, a so-called (euro-denominated) “parallel currency”.

The most plausible version of this is the government issuing notes that can be used to pay Greek taxes. This capacity to be used for meeting tax liabilities is what might literally give these notes “currency” as a means of payment. But here again, lack of confidence breeds lack of confidence. The probability of such a system working is low.

If that failed, then default would be combined with Greece re-establishing its own currency. This might be a preferable economic framework “in the long run” (!); but the transitional phase, which could be lengthy, would be horrendously painful.