The world’s biggest iron ore producer, Vale, has announced its intention to expand production despite a falling price. This follows similar announcements by Rio Tinto and BHP.

This expansion in production by the three largest iron ore exporters in the world, accounting for over 60% of the market, is puzzling and it may not be in the best interests of the resource owners in Western Australia and Australian taxpayers generally.

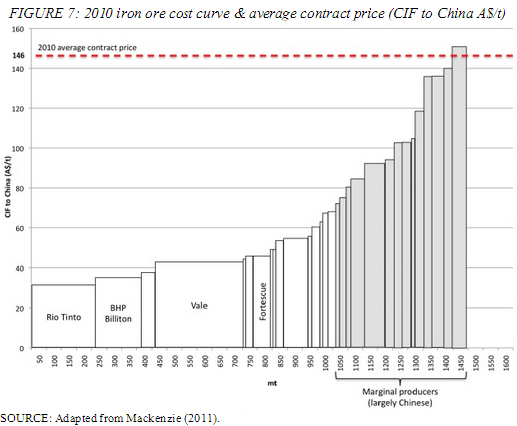

Why would firms pursue such a strategy? Western Australian Premier Colin Barnett has suggested the big miners may be flooding the market to reduce the price and drive higher-cost suppliers from the market.

Indeed, Vale’s CEO has indicated the objective is to displace competitors’ quantities. This is plausible as there are many producers that are marginally profitable at current world prices. They will likely exit the market if prices are reduced further.

{kind=link}

Given the big miners’ market share, it stands to reason that higher production volume will have a negative impact on iron ore prices. Perhaps the big miners hope that once higher cost producers exit the market, prices may rise again.

However, there many reasons to suggest such a view is too simplistic and this strategy will not work.

Crucially, iron ore production is by and large a mining and extraction activity. This means underground resources do not disappear if a high-cost miner exits the market. Equally, once resources are mined, extracted and sold at a potentially low price, the resources are gone and its owners will not be able to enjoy future higher prices.

It may make sense for the big miners to ramp up production now, despite causing a reduction in prices, if there are particular reasons to believe the demand for iron ore will decrease in the future. If this were the case, then it might be better to sell now, even if at reduced prices, vis-à-vis selling in the future at even lower prices. But this is unlikely given that many countries in Asia, Africa and South America will still need steel to catch up to the level of development of richer countries.

Is this just supply and demand at work? Is it a case of lower-cost producers vying for larger market shares even if this happens at the expenses of these companies’ shareholders? Unfortunately this ignores the interests of those who own the resources.

Iron ore resources are owned by the state (that is, by the people). The economic rents – the income derived from the ownership of a resource that exists in fixed supply – are captured in two different ways in Australia.

The Western Australian government charges (ad valorem) royalties on the value of iron ore sales. By increasing production, causing prices to fall, the big miners’ action will affect the value of the royalties captured by the government. Even if the big miner’s revenue rises due to quantities rather than prices, royalties may still fall if other Western Australian producers exit the market.

Similarly, Australians at large benefit from the tax revenue collected by the federal government. As the corporate tax is levied on accounting profits, lower iron ore prices may mean lower tax revenue as well.

Again, even if prices increase in the future, Australian governments will not be able to fully capture additional revenue as many high-cost producers are located in other jurisdictions.

Mining companies own capital that can be driven harder, as well as owning the mining rights. Managers may be tempted to increase production and enjoy a higher return on capital even at the expense of not maximising the value of the resource over the life of the mine.

The public, however, captures the value of the resources through ad valorem royalties and the corporate tax system. This means the public would benefit from actions that maximise the value of the resources over the life of the mine.

The challenge for the big miners is how to overcome this temptation of any short-term gains from increasing production to capture market share, at the expense of reducing prices further, resulting in a reduced value for the resources over the life of the mine. The challenge for governments, on behalf of the resource owners, is to continue to challenge the big miners’ thinking as Premier Barnett has done.