Private firms experiencing financial distress are sometimes compelled to sell-off profitable business units just to survive. But the state of New South Wales is not in that position, which is just one of the reasons why the latest push to privatise its electricity assets does not make economic sense.

The Baird government’s campaign for re-election essentially involves privatising profitable businesses – Transgrid, Ausgrid and Endeavour Energy – and spending most of the proceeds on non-revenue generating infrastructure.

Premier Mike Baird is a former investment banker, and he has claimed that his government “has been working tirelessly to Rebuild NSW … [and] fix the budget”, among its top priorities.

However, from our examination of NSW finances, several telling facts emerge.

Among our findings was that without state-owned electricity revenues, all other things being equal, the NSW Coalition government would have struggled to avoid deficits in every budget since its election in 2011. We also found that curious accounting methods have masked the underlying profitability of the agencies to be privatised.

Keeping NSW in the black

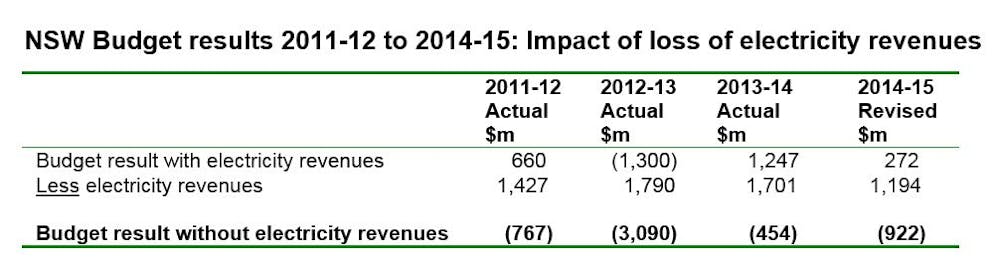

The table below is from our recent briefing paper on Electricity Privatisation, which we prepared out of concern at how poorly-informed the public debate has been about the true costs of privatisation.

As this table shows, the state’s electricity agencies have been a key contributor to keeping the NSW budget in surplus over the past four years.

The electricity revenues in the table are predominantly from network agencies, with some small amounts from generation, and represent both dividends and notional taxes that government businesses pay to the budget.

Obviously with the proposed partial privatisation, not all of these revenues will be lost – but the real loss will not be known until after the election.

Even an investment bank involved with the government’s electricity privatisation plan has concluded it is “likely have a negative impact on state finances in the long run” because of the loss of billions of dollars in dividends and other payments. The original 14-page UBS report released this week was entitled “Bad for the budget, good for the state”. After being contacted by Premier Baird’s office, the UBS report was reissued with a new title, “Good for the state” and new information about supposed other benefits from increased infrastructure spending.

We agree with the original UBS conclusion that privatisation would be “bad for the budget” – yet as we have shown above, that negative impact would not just be “in the long run”, but felt immediately.

Future loss to NSW taxpayers

The Baird government has tried to downplay the scale of any future loss of budget revenues by referring to the Australian Energy Regulator’s draft determination. This would reduce the reported profits of the retained electricity interests – but their effective return on shareholders’ funds would still be the envy of most listed companies.

Moreover, the NSW government has avoided any mention of the potential loss of revenues since partly-owned network agencies will be exposed to “real” Commonwealth taxes – a fact conceded by a Treasury official during a recent hearing of a Senate committee inquiry into privatisation of state and territory assets and new infrastructure.

Mention should be made of three crucial matters.

First, a state budget only reflects the financial results of the “general government” sector. State-owned corporations are required by national competition policy to pay commercial rates of interest on debt, and in NSW this is handled by the payment of a loan guarantee fee to the NSW Treasury Corporation, or TCorp, which is not part of the general government sector.

Anti-privatisation campaigns have referred to the A$1.7 billion in dividends and tax equivalents that the electricity agencies paid to the NSW government last year. That amount is actually an understatement, as it doesn’t take into account loan guarantee fees.

An internal government document distributed to Coalition MPs and selected journalists identified loan guarantee fees from the electricity businesses as amounting to A$338 million in 2012-13. The agencies’ financial statements did not separately disclose loan guarantee fees but aggregated them with “interest” expense.

Second, governments can influence how earnings are calculated. Depreciation expense is a percentage of reported asset values, and in NSW government businesses have based those values on current replacement costs (not historical costs), and that has led to higher depreciation expenses and lower reported profits.

Third, and more significant, is the fact that the state government can choose how much of the electricity networks’ (reported) profits are paid into government coffers as dividends. That’s an important point, because of a recent report that the electricity dividends and other payments to the state are set to fall from A$1.7 billion last financial year to around A$1.1 billion this year.

If dividends fall, is that necessarily a sign of falling profits? No – it could simply mean the NSW government is choosing to pay less into the budget. State governments can often “manage” budget results simply by requiring state-owned corporations to pay higher or lower levels of dividends to their consolidated fund.

In addition, at 30 June 2014, the three agencies slated for privatisation by the Baird government (Transgrid, Ausgrid and Endeavour Energy) disclosed nearly A$2.6 billion in retained earnings. That was an increase of A$666 million on 2012-13, or A$1.35 billion over the past two financial years.

NSW Treasurer Constance has claimed that the budget will not lose as much from privatisation as his opponents claim, arguing that Treasury forecasts diminishing returns to government to 2017-18.

But you can safely bet that if privatisation goes ahead, the network agencies will be stripped of cash in a last-chance effort to bolster budget results.

Curious accounting masks super profits

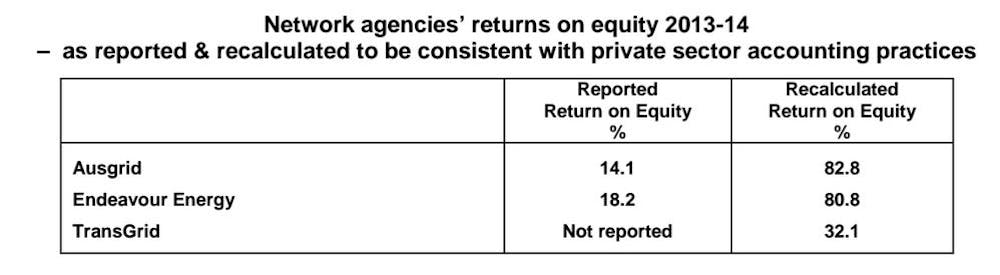

Our analysis also found that NSW electricity network agencies were far more profitable than shown in their 2013-14 accounts.

As noted above, the network agencies had based their asset valuations on current replacement prices rather than historical cost. Then in 2012, the NSW Treasury reversed its stance on the appropriate method valuing specialised assets for which there was no market evidence of “fair value”.

On the last day of the 2012-13 financial year, Ausgrid revalued system assets upwards by A$2.9 billion. That was done without explaining how those book entries had affected reported indicators of profitability. But the effect was to almost halve the reported rate of return the following year.

As explained in greater detail in our briefing paper, we calculated what the financial results of the network agencies would have been with normal private sector accounting techniques, as used by listed industrial companies.

Those recalculations revealed that Ausgrid and Endeavour Energy were earning returns on shareholders’ equity of between 80-82% per year – which are extraordinary super-profits.

That suggests either Ausgrid and Endeavour Energy are highly efficient, and/or they have been allowed to gouge consumers with excessive charges. Either way, they have been far more profitable than their accounting reports have suggested.

Reviving an old proposal, despite better economic conditions

New South Wales has low levels of debt. In June 2014, NSW had general government net debt of A$6.869 billion, or just 1.4% of Gross State Product.

This level of debt is highly manageable on annual budget revenues of around A$70 billion – especially at a time when Australian government borrowing costs are at record lows. NSW can keep its electricity businesses and use their revenues to fund new projects in other areas.

The current privatisation proposal is hardly new. Privatisation was first mooted by then Labor Treasurer Michael Egan in 1997, with a price tag of A$22 billion. Yet had he succeeded, the state would have missed out on dividends and tax equivalent payments to the budget in the period up to 2014-15 of A$20.2 billion – plus loan guarantee fees, and many billions of dollars in retained earnings. In that time, the electricity agencies were also able to fund tens of billions of dollars of infrastructure renewal.

Currently NSW is experiencing a boom in real estate prices, which will flow through to increased revenues from land tax and stamp duties on property transfers. This tends to be cyclical. The loss of a relatively stable source of revenues from the electricity network agencies would only make NSW more dependent on volatile property taxes.

Whether it was under Labor in the past or under the Coalition government now, the push to privatise NSW’s electricity assets is indicative of poor financial management. If it goes ahead, it would be bad news for NSW’s budget bottom line.

* This article was co-authored with Dr Betty Con Walker, an economist with experience in the private and public sectors, including with the NSW Premier’s Department and NSW Treasury. She has worked with various governments on policy and legislative development, and state budgets. She runs her own government and corporate consultancy. Her books include Casino Clubs NSW: Profits, tax, sport and politics, and Privatisation: Sell off or sell out (co-written with Dr Bob Walker), which are both available from Sydney University Press.