Much of the current political turmoil in Australia can be traced to Bill Clinton’s famous aphorism: “it’s the economy stupid” – in particular, the plunge in world commodity prices over the past few years.

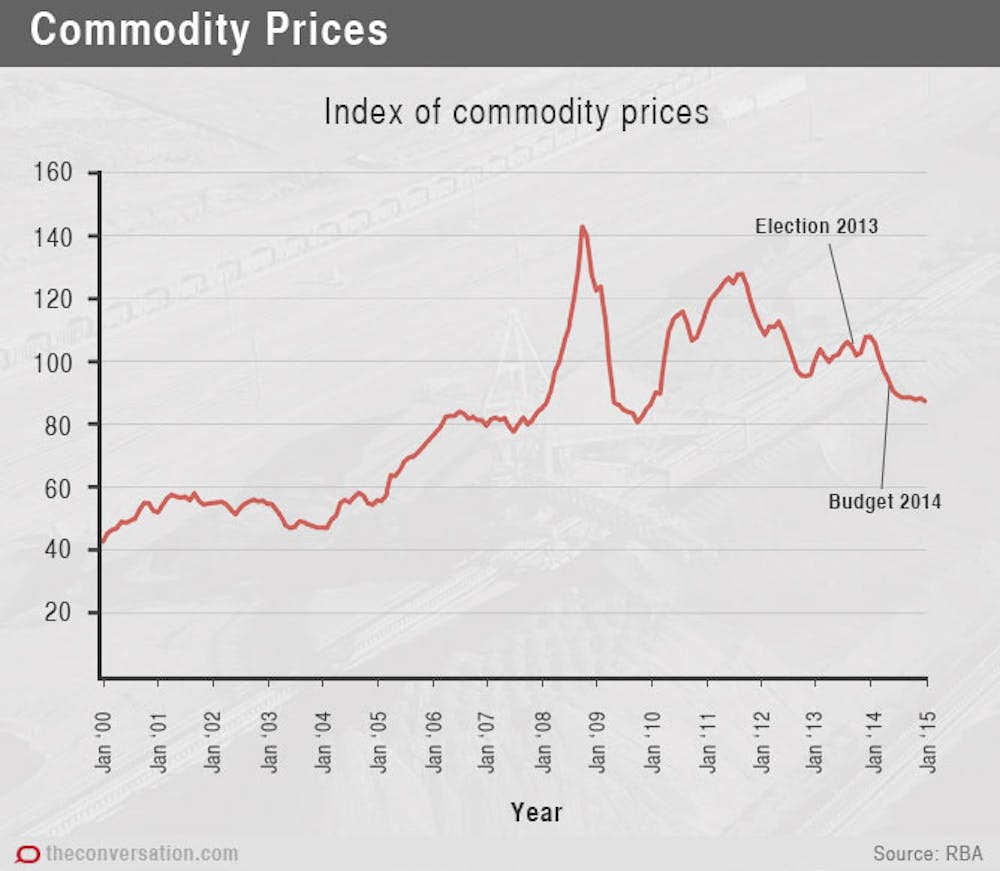

The prices we get for our iron ore and many other minerals have fallen by 50% from their peak in July 2011, and 33% in the last two years since January 2013. High prices are not coming back any time soon and in fact probably have a little further to fall. We have taken a hit to our living standards, partly through a 25% drop in the value of the Australian dollar against the US dollar since Jan 2013, which makes overseas goods and services 25% more expensive.

We would be feeling even more pain if the Abbott and former Rudd-Gillard governments had not temporarily protected us by letting the budget deficit blow out. Lower commodity prices hit the Australian government’s budget bottom line through lower tax revenue. In ball park terms, every 1% drop in commodity prices knocks about A$1 billion off federal government revenue in company tax and capital gains tax. So a 30% drop knocks roughly A$30 billion off government revenue. To put that in perspective the Australian government budget deficit is nearly A$50 billion, so the collapse in commodity prices is equivalent to more than half of the current budget deficit.

By letting the budget deficit blow out, the current and former governments have simply shifted the cost to the future – we will eventually pay through either less government services or higher taxes.

The impact on living standards

We may be facing a “new norm” of stagnant living standards. This will be a new experience. In Australia, as in other advanced countries, we have been used to rising living standards over time. The core driver has been productivity growth where the average worker produces more goods and services due to technology improvements. Labour productivity growth has averaged over 1% per year for decades. While this may even continue in the long term, it is being offset by lower commodity prices which are in turn driven by two factors that are not likely to reverse in the next few years: weaker economic growth in China and a deep malaise in Europe caused essentially by too much government debt.

It is this combination of lower commodity prices and the prospect of inevitable debt reduction through higher taxes and/or lower government spending on services and welfare that will continue to squeeze our living standards over the next few years – at least. Add to this a weak world economy and a lack of business confidence that has caused business investment to slump by about 4% on average over the past two years. The result has been weakening demand for labour which has seen wages growing at only 2.6%, barely keeping pace with inflation.

This is not a rosy outlook. Now more than ever we need policies to boost productivity growth in order to offset the effects of low commodity prices and the inevitable government tax/spending squeeze.

Time for bipartisanship

Yet we face immovable obstacles to achieving this. While both Labor and the Coalition tend to agree that productivity growth is important, they have very different views on how to enable it. And both are determined to block each other’s attempts.

The Coalition believes productivity growth comes from the private sector, provided governments get out of the way. They want less regulation of labour markets (such as lower penalty rates, relaxing unfair dismissal laws, individual wage bargaining), less protection of firms against imports, and lower taxes, for example. Labor generally doesn’t support any of this – it used to for a while under Hawke and Keating, but things changed. Instead Labor emphasises more government investment in education, training and public infrastructure which should be owned by government. Labor also thinks productivity growth is no holy grail and is not worth the candle if it means making the distribution of income and wealth more unequal, even in the short term.

Economists are unfortunately no help in this debate – there are enough economists in both camps.

The result is a stalemate: no real action on productivity and no attempt to control the future tax burden of rising government debt.

As voters, we must take our share of the blame. We vote out big spending governments but then threaten new governments with oblivion should they dispense the necessary medicine.

We will have to resolve this mess because the world economy is not about to come to the rescue any time soon.