In the midst of the row about Google’s low tax settlement, former chancellor Lord Lawson came up with a radical proposal. In an era where multinationals can artificially shift profits around the world, he said that taxing those profits has “had its day”, and corporation tax should instead be greatly reduced and “bolstered” by a tax on companies’ sales – the total amount of money that a business receives from selling goods or services to its customers.

He didn’t elaborate on what this might look like, but the notion of taxing sales raises serious objections. Given that Lawson is both very influential and an adviser to the present chancellor, George Osborne, these need to be laid out.

1. Stand by for failures

If companies were taxed on their sales, they would have to pay tax even when making small profits or losses. In the current system, many companies enjoy two different benefits – not paying tax when they make losses and then obtaining a tax refund during hard times by offsetting losses against past profits. This can make the difference between survival and failure.

2. Investments could dry up

Companies can make losses or low profits as a consequence of major investments. A sales tax could therefore act as a disincentive to making those investments. In addition, it could be a major burden on new companies in their early years. It might therefore discourage entrepreneurialism across the board.

3. Trouble for the little guys

A sales tax would have to be introduced on a global scale. You couldn’t have companies paying taxes on profits in some jurisdictions but sales in others. But as a result, it wouldn’t just be multinationals like Google that had to deal with multiple national tax authorities. Smaller companies in the export business would have to as well, which would impose an extra business burden. Such companies might be discouraged from seeking out new export markets.

4. A new race to the bottom

Countries would probably set different tax rates. Companies, particularly those selling high-value items, may consequently focus their sales on countries with lower tax rates. This wouldn’t be conducive to economic co-operation and development.

5. What to do with long-term contracts?

Determining sales is not straightforward in some sectors. Take construction companies with long-term contracts, for example. Long-term contracts often have a retention clause, which means that customers do not pay for all the work until the end of a contract. With a sales tax, you would be taxing companies on money retained by customers, which would impact their cashflow.

6. Out with group relief

At present, a loss by a subsidiary in a group of companies can be offset against a profit made by another subsidiary in the same group. A move to sales-based taxation would not allow this, since all companies that made sales would be taxed on them. Instead the group’s tax burden would rise.

7. Goodnight, Tesco

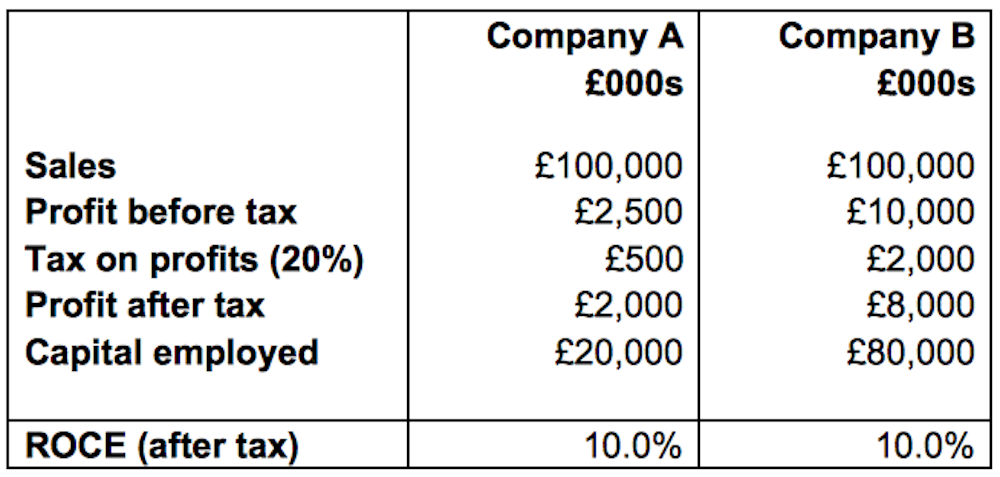

What would be the right tax rate to apply? The simple answer might appear to be the rate that would generate about the same tax at present. But this presents a problem for one of the classic business models: the high-volume, low-margin business. In the following example, Company A is a supermarket and this kind of business, whereas Company B is a manufacturer of jet engines and a low-volume, high-margin business. The table below shows their current tax arrangements. While Company B makes four times as much profit after tax, it makes the same return on capital employed due to its high investment in plant and machinery.

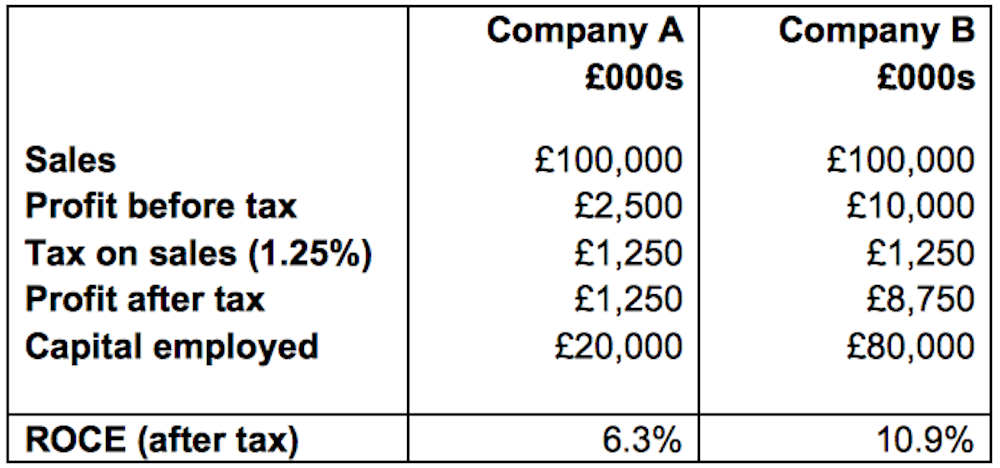

The next table demonstrates what would happen if corporation tax was charged on sales using a rate of 1.25%. Now that they are being taxed on sales, which is £100m for both companies, Company A’s profits fall and Company B’s rise. Company B now makes seven times the after tax profits. Company A would have less money for investment and Company B more, which would quickly warp the economy.

For this reason, governments could not set a single sales tax rate. They would have to somehow set appropriate rates for different business sectors and different business models within the same sector. Even if this were possible, the sales-tax rates would have to be constantly updated to take account of changing circumstances.

The alternative

Bear in mind that Lord Lawson suggested a hybrid of the two kinds of tax – a greatly reduced corporation tax bolstered by a sales tax. This sounds like the worst of both worlds. Companies and governments would still have to deal with the current complex, controversial tax system (which would bring in very little tax receipts) and cope with a wholly inappropriate new tax.

One alternative would be to scrap corporation tax. This might sound radical, but onshore corporation tax brings in only 8% of the UK’s tax revenues. Abolishing it would cut public spending by freeing HMRC from managing the current complex system. It would save companies the cost of complying with corporation tax, and give them more cash for investment. And it would attract businesses, which would both boost economic activity and increase receipts from income tax and national insurance.

Having said all that, such a move would be politically unacceptable, so it’s never going to happen. Back to the drawing board, then. Just don’t let the idea of sales taxes catch on.