One of the certainties in the energy business used to be the regular year-in, year-out rise in demand for electricity [1].

Up until about 6 years ago, demand growth could be counted on with metronomic precision. Across our National Electricity Market – the NEM - electricity demand grew at about 2% annually.

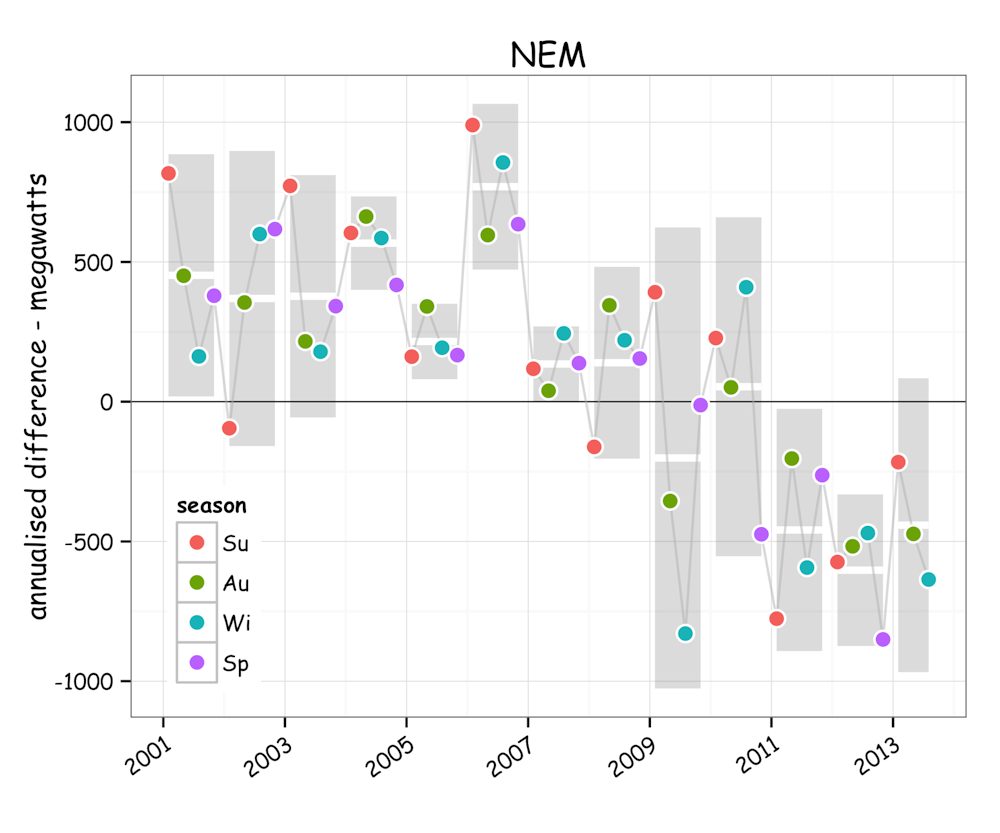

That all stopped in 2008. On the basis of the numbers for June and July this year, we are on the verge of our twelfth straight season where demand has reduced on the year before.

Over the last 3 years, the annualised demand reduction has been about 500 megawatts - or about 2.2%. And since the peak in 2008, average demand has reduced by about 2 gigawatts or about 8%.

On these figures, Australia is clearly undergoing a profound de-electrification. If it continues for a few more years then, by analogy with economics, it will be worthy of the appellation the great de-electrification.

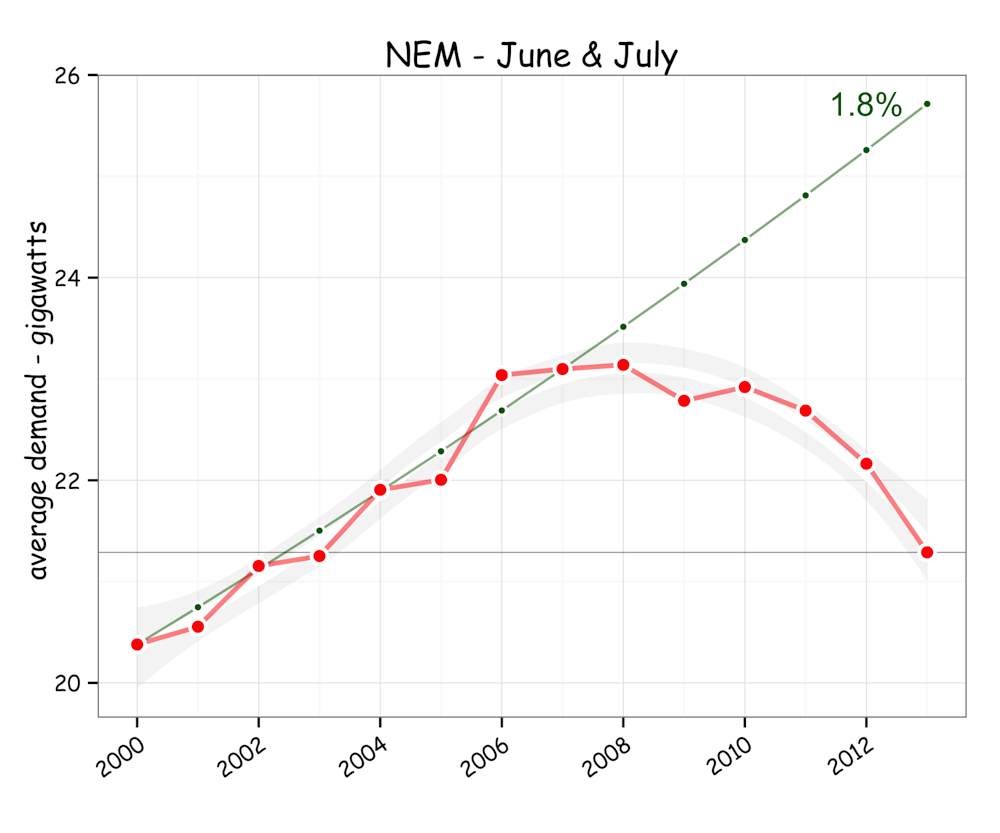

To appreciate the real significance of these numbers we need to look back a few years. Because the planning for new generating plant takes many years, we are still in an investment cycle that dates back half a decade or more.

Looking back to 2007 and the outlook for electricity investment was looking rosy. In 2007 planning would have been for a generation capacity growing at 2% each year. Then forecasts were for an average winter-time demand of around 26 gigawatts.

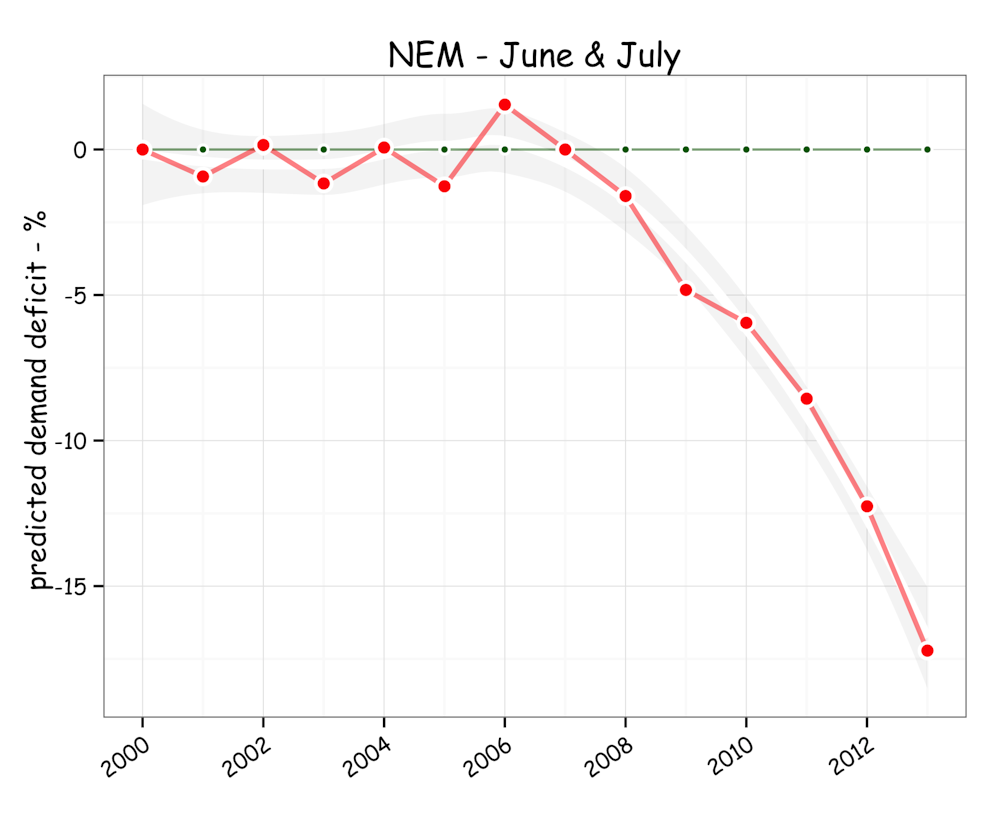

That is almost 4.5 gigawatts greater than we have seen so far this winter. In percentage terms the 2007 forward projections were out by about 17%.

And the problem is that all the pointers seem to indicate demand reduction is accelerating. The latest figures for the June-July period show the largest annual reduction recorded - amounting to about 5% on those forward projections.

Across the NEM the generating capacity is a bit over 50 gigawatts, or a bit over twice the average demand.

The fall in demand is creating a tremendous capacity overhang in generation. That has significantly depressed wholesale electricity prices over the last few years.

And that is impacting industry players such as AGL, who have been recently reported as calling for a retirement of up to 9 gigawatts of generation capacity across the NEM.

That is a massive amount, representing a bit more than the total capacity of the generation fleet in the Latrobe Valley that supplies about 85% of Victoria’s electricity.

The logic for a 9 gigawatt retirement is straight forward. At about 17% of the total NEM-wide generation capacity, it is more-or-less identical with the demand reduction on the forward projections of just 6 years ago shown in the figure above.

The big question in the electricity game is what will happen to demand in the next few years. Despite industry pundits having consistently forecast return to growth for a number of years, all the signs are that demand reduction is accelerating.

Certainly the trends in the figures shown above seem to indicate we haven’t bottomed out yet. So at least for the near term the great de-electrifcation is a stronger bet than a return to growth.

If so, there will be need for very significant restructuring in the generation sector, of the likes we have never seen. In the meantime we should expect some very aggressive repositioning amongst our energy utilities.

In a normal market, oversupply should lead to some very aggressive pricing to maintain market share. The question is, how normal is our electricity market?

[1] The term “demand” is used here to refer to the average demand and so provides a measure of the total electricity demand over period of time, rather than the instantaneous “peak” in demand.