Not too long ago, cynics were wondering if David Cameron’s fears over the global economy were a ploy to shift blame for any flaws in the UK’s performance as we near the May 2015 general election. However, the publication of the Organisation for Economic Co-operation and Development’s latest Economic Outlook can only make the British prime minister’s “red warning lights” flash a little brighter.

The headline forecasts for global growth from the OECD are for an increase from 3.3% in 2014 to 3.9% in 2016, but they mask considerable variations in the prospects of the leading economic powers. Brazil, India, and the United States are, if the OECD’s forecasts come to pass, likely to see growth rates accelerating. Meanwhile, China is expected to see its economy grow at an impressive 7% a year through to 2016. In contrast, the euro zone and Japan are expected to languish with annual growth rates around 1%.

American dream

What a difference a year makes. For many, doubts about the US recovery were finally set aside in 2014, so much so that the Federal Reserve stopped its policy of quantitative easing (QE). Like many others, the OECD is pretty bullish on India after the torpor that set in during the run up to the national election in May. Japan shot itself in the foot by raising a consumption tax and the euro zone slides ever closer towards deflation. Indeed if the manufacturing sector’s falling producer prices defined inflation, as opposed to consumer prices, then much of the euro zone is already in serious trouble.

On the whole, the OECD found that governments have eased off on austerity, while central bankers are still expected to pull a rabbit out of the hat and turn stagnating economies around. Economic reforms have stalled in many countries. With the exception of Japan, policy surprises have been few and far between. And by and large, government leaders continue to duck the fundamental challenge of rebalancing national economies.

In the meantime the divergence between rosy pre-crisis trends and present circumstances becomes clearer and clearer. World trade growth is markedly slower than in previous recovery phases. Private investment rates remain below trend in many industrialised economies. The OECD reckons that the maximum speed with which many countries can now grow without stoking high rates of inflation has slowed markedly. Economists are used to distinguishing between longer term trends and shorter term cycles; nowadays a faltering recovery appears to be undermining the drivers of longer-term living standards.

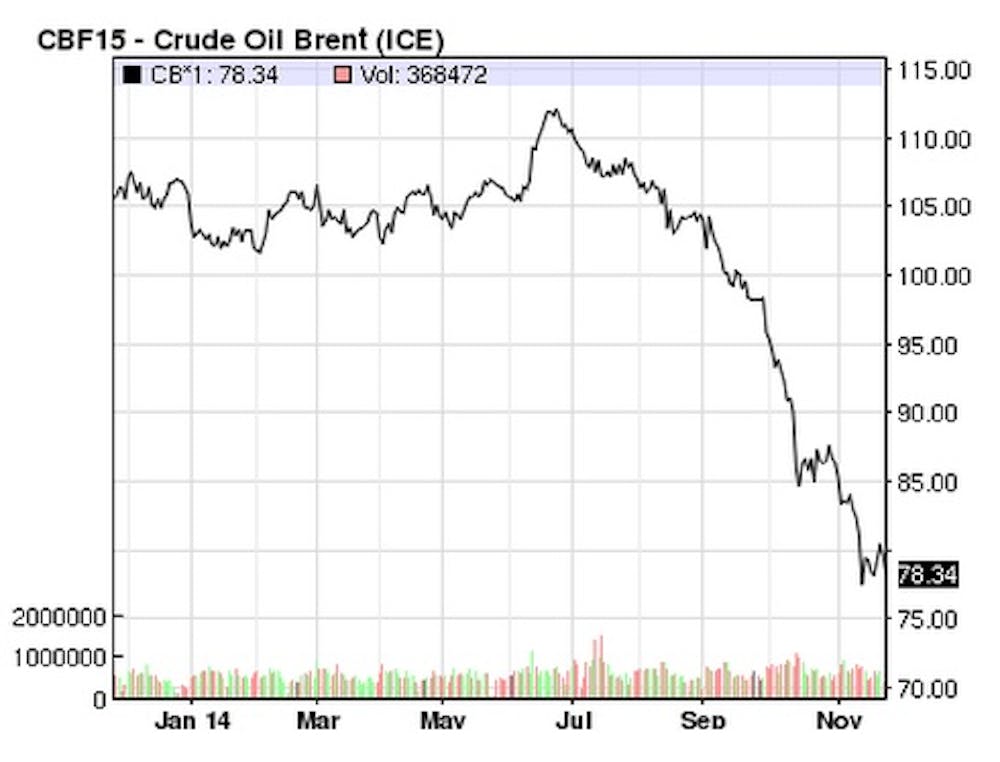

Oil well

The combination of low growth and falling prices is relentlessly pushing up private sector debt levels in Europe, while borrowing binges in many emerging markets go unchecked and add to financial vulnerabilities. Still, at least we have seen the end of last year’s “taper tantrum” in many emerging markets sparked by the end of US quantitative easing, and the OECD notes that most indicators of financial market instability have calmed down.

One factor, likely to be a net positive for the global economy, but which the OECD has given little attention to is falling oil prices. The price of a barrel of Brent crude is down 29% this year (see the chart below). Some experts estimate that the fillip to consumption spending that resulted from lower oil prices will, among other effects, boost global growth by between 0.5-1.5% in 2015, which in the current era of relatively slow growth is pretty significant.

Expect a positive impact on many governments’ fiscal deficits too, especially in those countries where energy subsidies are rife and where climate change concerns are being used as a pretext to increase taxes on oil. Of course, given the rollercoaster of oil prices during the past decade plus the growing interest in shale gas, forecasting energy prices is particularly fraught. Still, so long as oil prices stay low, then eventually this is going to feed into the global economy.

Danger zones

All of which might make you think we were home and dry. The concern remains, however, that policymakers in the euro zone and Japan will resort to more desperate measures. Here the OECD report contained the results of a simulation that is almost certainly going to raise eyebrows in many national capitals. The OECD simulated the impact of Japan and the euro zone devaluing their currencies by 1% in each of the next 10 quarters on trading partners’ growth. These devaluations would cut into China, India, and Russia’s growth rates in 2015 and 2016.

According to the forecast, however, the country most harmed will be the UK, with its extensive trading ties to the continent. The OECD reckons that these relatively mild devaluations would by 2016 knock half a percentage point off British growth, further slowing an already weak recovery. If so, Cameron’s fears about the global economy may be valid after all.