Readers of the Financial Times would have recently encountered a story that encompasses the paper’s version of bad/good news when it comes to the oil business. According to the author Daniel Yergin, the bad news is that several major oil exporters are suffering from insurrection and civil war, which threatens global supplies. But, there is also good news:

The sum of these risks is trumped by the old-fashioned forces of supply and demand. While there may be a surplus of geopolitical risk in the world, there is an even greater surplus of oil.

To deconstruct these sentences, I set aside the glaring misuse of “supply and demand” (be it “old-fashioned” or up-to-date, these so-called forces apply only in an imaginary world of perfect competition, which the petroleum market is not). Readers discover that the trump card in question comes out of the US deck of energy cards. To be specific: “US crude oil is up almost 80% from 2008” and this year US production exceeded that of Saudi Arabia, making the Land of the Free the world’s largest source of black gold.

So, to paraphrase: a lot of bad stuff is happening in the parts of the world where we used to get our oil, but that’s ok because there’s a new kid on the energy producing block, and it’s one of our friends.

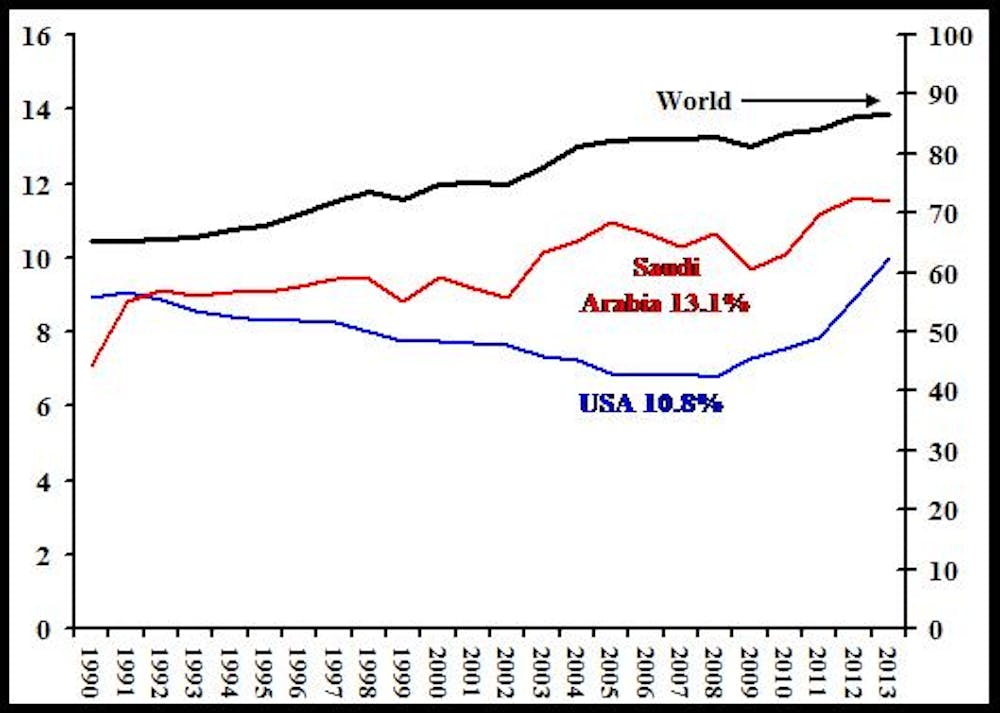

US takes over the oil race

The chart below shows this US race to first place through 2013, when the Saudis were still number one with 13.1% of world output, and the US hot on Saudi heels with 10.8% (Saudi Arabia and the US are measured on the left axis, world output is on the right). According to Yergin, the increase in US production will more than compensate for any declines in conflict-affected oil producing countries.

Energy prices

As if to verify the cliche that there is nothing as old as yesterday’s newspaper, just three days later the FT ran another article with the title: “Crude oil rallies sharply after near four-year low”. In fairness to Yergin and his “good news” about an oil glut, petroleum prices are notoriously variable – and evidence suggests that he might be correct over the medium term.

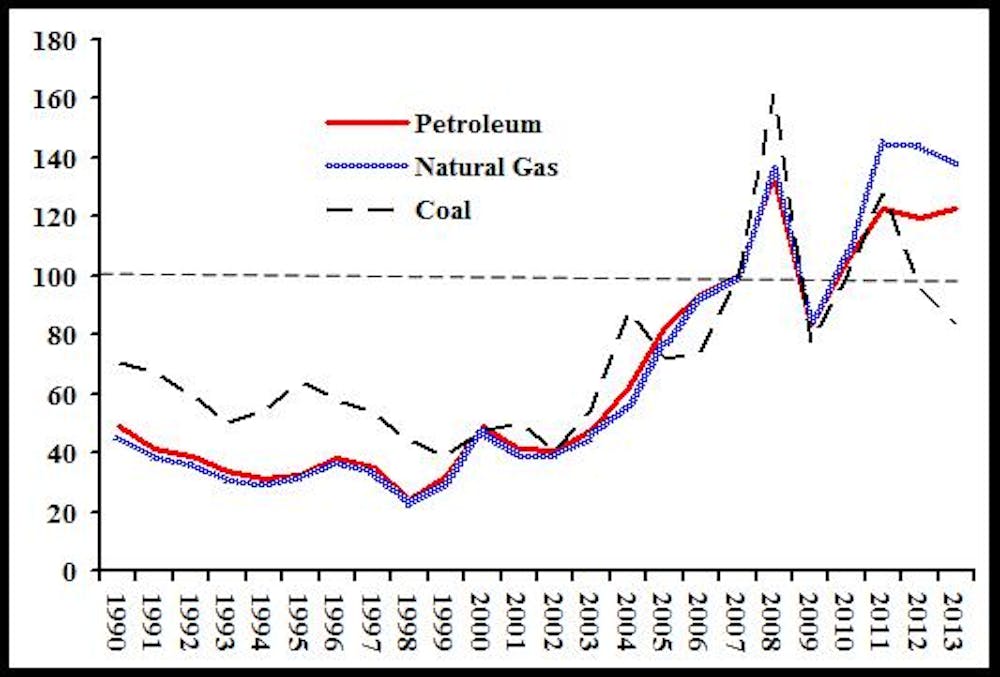

The chart below shows the prices of petroleum (based on the “West Texas Intermediate”, a crude oil grade used as a benchmark in oil pricing), natural gas (the average price for OECD countries), and coal (US central Appalachia – again a benchmark for pricing), all divided by the US producer price index to give a measure of “real” energy prices.

Essentially, the result measures whether energy prices go up or down compared to other goods and services. Since 2010, the annual price of all three major energy sources of greenhouse emissions have either declined (coal substantially, natural gas slightly) or flat-lined (petroleum).

The evidence further shows that petrol prices at the pump have declined for the past two-and-a-half years from a cross-national average of 141p per litre in April 2012 to 125p now – down by about 13% (see chart below). If the pump price were deflated by the cost of other goods and services bought by households, the decline would be close to 20%.

Either way, a cheaper price at the pump has to be good news, right? It certainly is for all those readers who are eagerly looking forward to the end of civilisation as we know it, but not so great for those of us hoping that the planet might achieve environmental sustainability. This is because how much of a commodity households buy depends on their incomes and the price of that commodity.

Energy consumption

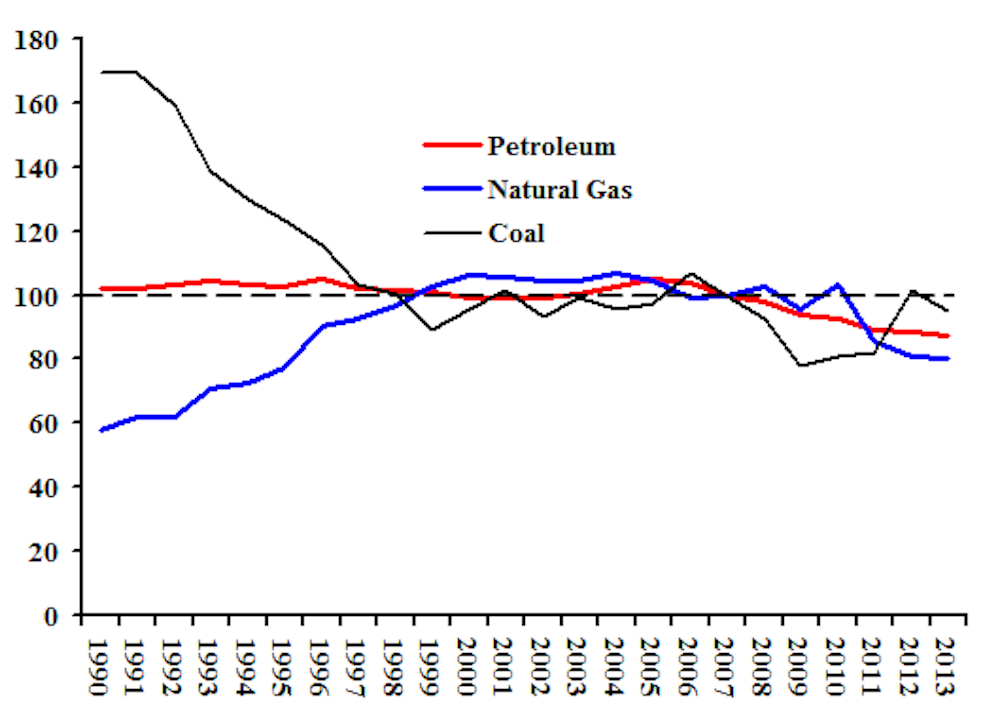

In the chart below we see that from 1990 up until the financial crisis in 2007-2008, UK consumption of petroleum hardly changed. Meanwhile, from 1990 to the end of the century natural gas replaced coal, for both for heating households and in factories and offices. After 2007, coal consumption increased, primarily due to businesses using more as coal prices declined substantially compared to prices for oil and gas.

As worrisome as this increase in use of coal is, the lower consumption of oil and gas (12% and 20%, respectively) did not result from conservation policies. It was instead because of a failure of household income and manufacturing production to recover since 2008. In other words, if the Great Recession had not occurred, it is a safe bet that consumption of hydrocarbons would today be much greater than in 2007. Needless to say, reducing energy use by a massive recession is not the best approach to conservation.

On the chance that the consequence of increased use of solid fuels is not obvious, an Environmental UK pamphlet reminds us:

Using coal and other mineral solid fuels for home heating will usually result in higher emissions of both local air pollutants (such as particles and sulphur dioxide) and carbon dioxide (the greenhouse gas) than an equivalent natural gas-fired system, and therefore coal fired heating will normally have a higher environmental impact than gas.

A 2013 report from the Department for Environmental, Food and Rural Affairs warned that after substantial reductions in emissions of air pollutants during the 1990s and early 2000s the “rate of reduction has slowed”. In the specific case of sulphur dioxide, an 11% increase in 2012 wiped out the decline of the previous two years.

It is ironic that the only substantial reduction in UK consumption of fossil fuels came during the severe economic downturn after 2007. If the chancellor had not pursued policies to depress recovery, which I have discussed in detail in previous articles , Britain would be considerably more polluted than it is now.

In a grand scheme to destroy the environment, a lower price of petrol is a minor matter. However, its impact on consumption is significant – and more for business users than households. Perhaps the greatest importance of low energy prices lies in the message they send – business as usual in face of the greatest threat to the planet.