Over the past decade, there have numerous efforts to replace petroleum-based fuels with fuel made from plants, or biofuels. One challenge to commercializing biofuel made from non-food sources — called cellulosic biofuels — has been cost.

Unlike ethanol made from corn, cellulosic biofuels are made from the inedible parts of plants or organic materials, so there isn’t competition between food and fuel. But given the rapid decline in crude oil prices since last summer, it is logical to ask what the impact of lower crude oil prices on future development of cellulosic biofuels will be.

As you might expect, plunging oil prices make it tougher for makers of cellulosic biofuels. But much of the uncertainty regarding the future stems from policies forged in Washington D.C.

Falling well short, technically

The source material, or feedstocks, for cellulosic biofuels can be dedicated energy crops such as switchgrass, miscanthus or poplar trees. Or they can be crop residues, such as corn stover and wheat straw, or even residues from logging. Municipal solid waste also contains cellulosic components. In a 2011 study, Oak Ridge National Laboratory estimated that there is enough cellulosic biomass available in the US to displace about 30 percent of the country’s petroleum consumption.

The primary driver for the development of the biofuels industry is the federal government. Legislation in 2007 established US renewable fuel targets. The Renewable Fuel Standard (RFS) in the legislation calls for 16 billion gallons of cellulosic biofuels by 2022 and the legislative mandate for 2015 is 3 billion gallons. (There are three other types of fuels, including corn ethanol.) The mandate requires fuel refiners or importers to purchase some biofuels along with petroleum-based fuels.

However, the industry has not developed at the hoped-for pace, so the US Environmental Protection Agency has had to waive most of the cellulosic portion of the mandate each year. Actual 2015 cellulosic biofuel production will be less than 100 million gallons, well short of the original three billion mandate.

In principle, the RFS guarantees any cellulosic biofuel producer a market for what they produce. That is the case for biodiesel, corn ethanol, and sugarcane ethanol, which refiners purchase to blend with petroleum-based gasoline or diesel.

Not guaranteed market

However, for cellulosic biofuels, there is an out-clause in the RFS that enables obligated parties, including refiners and fuel importers, to buy out of their cellulosic biofuel blending obligation. The current cost of this option is about $1.45 per gallon. That is, an obligated party can pay about $1.45 per gallon in lieu of purchasing cellulosic biofuel. So the RFS is not an iron-clad guarantee of a market.

In essence, the out-clause puts a cap on the price of cellulosic biofuels. If the difference between the wholesale price of gasoline and the cost of the cellulosic biofuel is greater than $1.45, obligated parties will pay, instead of purchase the fuel.

One final point of background information is that cellulosic feedstocks can be made into a wide range of biofuels. If the cellulose and hemi-cellulose in plants are separated from the lignin and converted to ethanol, this is done in a biochemical process. The lignin is then used for fuel in the plant or for other purposes.

When making a fuel, the cellulosic feedstock can be thermochemically converted to hydrocarbons, including gasoline, diesel, jet fuel and other hydrocarbons. In thermochemical processing, the entire feedstock is converted to a bio-oil (pyrolysis) or a synthesis gas (Fischer Tropsch), either of which can be further processed on to fuels and other products. These fuels are called drop-in because they are very similar to existing fossil fuels and can be used directly in existing infrastructure, unlike ethanol. Ethanol cannot be shipped in pipelines, is normally blended at 10%, and cannot be used in some applications.

Long-term investments

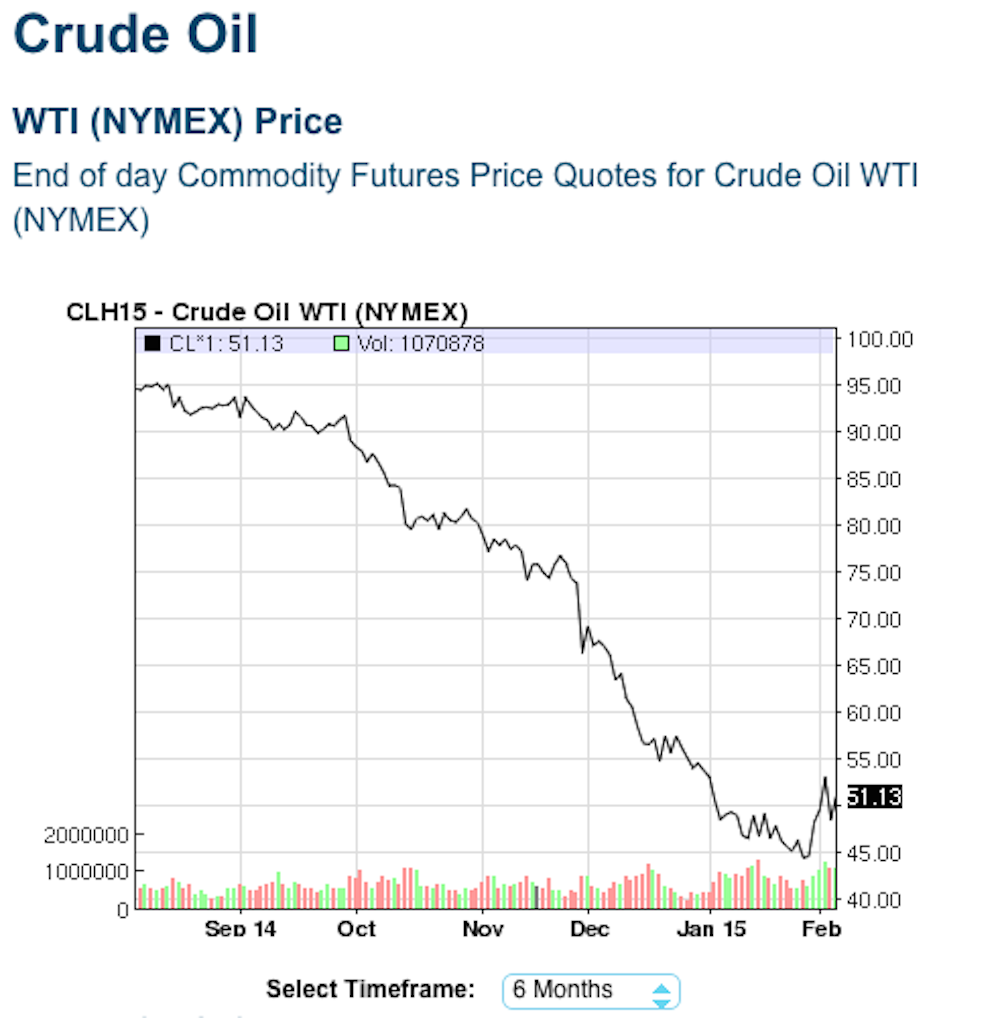

With this background in mind, what are the impacts of the plunge in crude oil prices? First of all, my estimate is that it takes crude oil at about US$140 for most cellulosic biofuels to be economic without subsidies or mandates. Thus, without government intervention, there would be no future for cellulosic biofuels with crude oil prices well below US$100. Crude oil prices have hovered around $50 for the past month.

So the real ques what is the future given that we do have the RFS? The answer to that question is uncertain. There have been a number of efforts in Congress to reform or outright repeal the RFS.

How will investors view the current situation? Making a profit on a cellulosic biofuel investment today requires one to believe that the RFS will remain in place for the 20-year life of a prospective investment, or a strong belief that low oil prices will not last long.

But even if one believes that the RFS will remain, there is still the out-clause which means that obligated parties are not really required to pay the full cost of production. production. On February 5, 2015, wholesale gasoline was $1.51/gallon. With the buy-out cost at $1.45, the maximum obligated parties would be willing to pay for cellulosic biofuel is the sum of the gasoline price and the buy-out cost, or $2.96/gallon.

Most of the technologies today have total production costs significantly greater than $2.96/gallon. Biofuels producers may be willing to sell for that price to assure having a market for their product, and they could recover variable costs, but not total costs, which includes the capital in plants to produce biofuel. There is a temporary production tax credit for cellulosic biofuel of $1.01/gallon, but no guarantee how long it will last, so investors cannot count on it for the long term.

The bottom line is that it will be difficult times for current and prospective future cellulosic biofuel producers so long as crude oil remains near where it is today.