The COVID-19 pandemic is no longer a global emergency, Canada’s GDP outperformed expectations in 2023, the economy seems to be heading for soft landing after a period of stagnation, inflation is winding down and unemployment has decreased to 5.7 per cent in January 2024 — close to pre-pandemic levels.

Despite these positive economic indicators, recent surveys suggest Canadians are dissatisfied with the direction of the economy. An overwhelming 84 per cent of Canadians believe the country is already in a recession, with 73 per cent anticipating one within the next year. Young people, in particular, are fearful of the future.

This discrepancy prompts the question: Why are Canadians’ sentiments so at odds with economic indicators? As economists, we have identified several reasons that explain why this gap exists.

1. Growing socio-economic divide

Income and wealth inequality are both growing at an alarming rate in Canada. The wealthiest 20 per cent now account for more than two-thirds of net worth, compared to the 2.7 per cent held by the bottom 40 per cent.

The top 20 per cent accounted for 40.3 per cent of net disposable income in 2023, while the bottom 20 per cent accounted for just 6.1 per cent. The top one per cent of earners, meanwhile, have grown even richer.

Read more: Two-thirds of Canadian and American renters are in unaffordable housing situations

In contrast, the number of people in the low-income cutoff group keeps increasing. Net saving for the lowest income households decreased by 9.8 per cent in the third quarter of 2023 compared to the previous year.

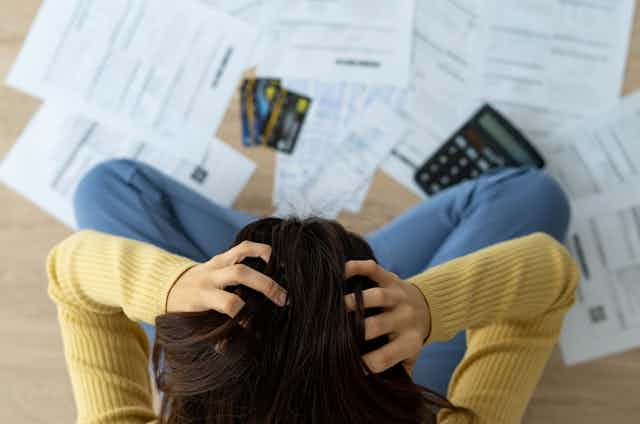

2. Debt servicing burdens

Since the onset of the pandemic, net savings have deteriorated for all except those with the highest incomes, as renters and lower-income families tend to spend more than they make on necessities.

Canada currently holds the highest amount of household debt as a percentage of disposable income among all G7 countries. With the current high interest rates, the burden of interest payments for households as a percentage of disposable income recently reached its highest level in 12 years.

3. Interest rates

The average disposable income for the top 20 per cent of Canadians is increasing at the fastest rate of any income group. This means those with financial assets benefit from rising interest rates, while those at the bottom suffer from the burden of greater debt service.

4. Housing costs

Skyrocketing housing prices have outpaced income and mortgage rates have gone up dramatically, resulting in the lowest home affordability index in the last 40 years. The dream of home ownership seems more distant than ever for many.

5. Impact of inflation

Although Canada’s inflation rate shows signs of slowing, it still remains fairly high. It reached a 39-year high of 8.1 per cent in June 2022, hitting those in low-income groups the hardest.

6. Growing corporate concentration

Canada’s most concentrated industries have become even less competitive, and the number of highly concentrated industries is growing. Profit margins and markups of already profitable firms is increasing.

This trend negatively impacts consumers and broader society by reducing industry dynamism, resulting in fewer choices and higher costs.

We are seeing this currently play out in the grocery sector, where a lack of competition has resulted in higher food prices. This is the same reason why airplane tickets and cell phone bills remain higher in Canada than in comparable countries.

7. Mental health struggles

The proportion of people reporting very good or excellent mental health decreased to 59 per cent in 2021 from 72.4 per cent in 2015.

The prevalence of some chronic conditions, including high blood pressure, heart disease and obesity, increased from 2015 to 2021 as well.

Financial anxiety, pandemic-related stress and other issues are making Canadians feel angrier in general, which affects their outlook on life and the economy.

8. Long COVID

While the impacts of the pandemic are slowing down, long COVID is still a significant issue for many. One in nine people who contracted COVID-19 suffer from symptoms, including brain fog, cognitive impairment, fatigue and shortness of breath, that affect their health and well-being.

It is shortsighted to assume we have all recovered equally from the pandemic when some people are still being affected by it.

9. Higher education funding cuts

College education has historically served as “the great equalizer” and an instrument of intergenerational social mobility, but in the face of declining government support for post-secondary education, this may no longer be the case.

The financial situation of many colleges is increasingly precarious, meaning post-secondary institutions could end up raising tuition fees or rely more on international students to meet their budgets, both of which affect domestic students.

Students from the lowest economic stratum will increasingly find it difficult to trade the security of a job right out of high school for the high cost of a university or college degree. This, in turn, will reduce their chances to move up in the socio-ecnomic ladder.

10. Youth struggles

Youth across North America are more anxious about their future, concerned about their mental health and educational prospects and more disillusioned by politicians than previous generations.

Despite being resilient and pragmatic, Gen Z are pessimistic about the world around them and the future ahead. They worry about their financial security, with high costs of rent and groceries.

A 2023 survey from the Globe and Mail found that nearly three-quarters of Gen Z disagreed that, as a generation, they would surpass their parents. Fifty-six per cent feel afraid, sad, anxious and powerless about climate changes, while 78 per cent reported that climate anxiety is impacting their mental health.

Navigating the disconnect

While more than 40 per cent of Canadians hope for positive outcomes in 2024 and the macroeconomic indicators show prosperity, there exist numerous factors causing dissatisfaction in large swathes of the population in Canada.

Managers, business leaders, policymakers, government officials and economists should all care deeply about this issue. Over-relying on aggregate indicators — like macroeconomic prosperity — while making strategic, investment, hiring and financing decisions could lead to unexpected outcomes and challenges.

For example, a real estate company might decide to invest in a large, low-end housing project based on economic numbers. While the initial logic may seem sound — if the economy is doing well, that there should be a huge demand for housing — issues might arise if the target population is financially strained and unable to afford the housing.

A comprehensive understanding of the mindset, risk preferences and motivating factors of key customers, stakeholders, investors, employees and voters is essential for making well-informed decisions that benefit all parties involved.