Where will jobs and growth come from after the mining boom? This is the fundamental question facing the next Australian government, whose success will depend to a great extent on how it addresses this question.

The resources investment of recent years may well bring additional production and exports, but it’s becoming clear that the boost to our national income growth from the high commodity prices from Australia’s latest mining boom is coming to an end, revealing a serious and potentially damaging fall in productivity.

What do we need to do to create long-term growth and jobs?

How we got here

Let’s begin at the beginning. We have to ask ourselves, did Australia make the best use of the windfall from the boom that was never supposed to end? The economic gains were unprecedented in their size and impact, and even though temporary, could have prepared us well for a post-boom economy. Prior to the 2007 election, then opposition finance spokesperson Lindsay Tanner complained that the Howard government had been:

…rained with revenue by the minerals boom and it’s wasting far too much of it and it’s not building it for the future.

The incoming Labor government had an opportunity to capitalise on the re-emerging mining boom, driven by demand from China and the region. However, apart from the government’s deft handling of the global financial crisis, which was no small achievement, it is difficult to make the case that Labor did so much better than its predecessor in constructing an economic legacy for a world of knowledge-driven products and services.

As well as being constantly distracted by leadership issues, the government made little headway against the prevailing economic orthodoxy: the misunderstanding of short term business cycle activity as longer term structural change, and the false belief that resources- driven growth had become such a permanent feature of the Australian economy that manufacturing and other sources of growth could safely be abandoned.

Clearly, the global economy is going through major structural change, but this is less about commodity price fluctuations than innovations in technology and business models and the changing patterns of international trade and development.

The problem and continuing challenge is that Australia is not taking as much advantage of these changes as we could. Both business leaders and policy makers have allowed the contribution to growth from trade to mask a steady deterioration in our productivity over the past decade, which will be fully laid bare as the mining boom fades in coming years.

This is nothing new. Australia has seen such booms before, which have ended badly, and their lessons have been widely canvassed. We have also had the benefit of observing the impact of North Sea gas discoveries in the 1970s on Dutch manufacturing, as booming gas revenues drove up the value of the currency, making it much harder for Dutch industries to compete on the international market. It took many years with a laser-like focus on industry and innovation policies to overcome the so-called “Dutch disease” and reconstruct and reposition manufacturing.

Similarly, North Sea oil and gas enabled the UK government of the 1980s to keep itself in office by fuelling a consumption boom with tax cuts. Only gradually was there a realisation that, in the words of J. K. Galbraith, the price of private affluence was public squalor, as schools and hospitals bore the brunt of neglect and key areas of manufacturing were lost, never to return. Ironically, the experience was repeated with the finance sector in the 1990s and 2000s, once more ending badly, with a new government committing to “re-balancing” the economy.

All Australia had to do was learn from the past – and observe the current approach of Norway, which actually learnt something from the experience of other resource rich economies. Norway has taken a public stake in its mammoth oil and gas assets, imposed a 76% resource rent tax, and established a sovereign wealth fund to partially quarantine the exchange rate and provide an income stream for investment in research and innovation.

Beyond the boom, Norway will have given itself the best possible chance to build a competitive knowledge-based economy. Already it is a world leader in productivity performance – we have a lot of catching up to do.

Productivity slowdown

Without a shared understanding of the problem, it’s not easy to come up with a solution to Australia’s productivity slowdown, which has only partly been reversed over the past year and not anywhere near the required scale of improvement.

While economists and policy-makers agree that productivity drives growth, competitiveness and living standards, there is much less agreement on where productivity comes from, and how to measure it – and thus on the policies which contribute to sustainable productivity improvement. The need for productivity improvement has been sharpened by two separate but related problems that have recently received considerable public attention.

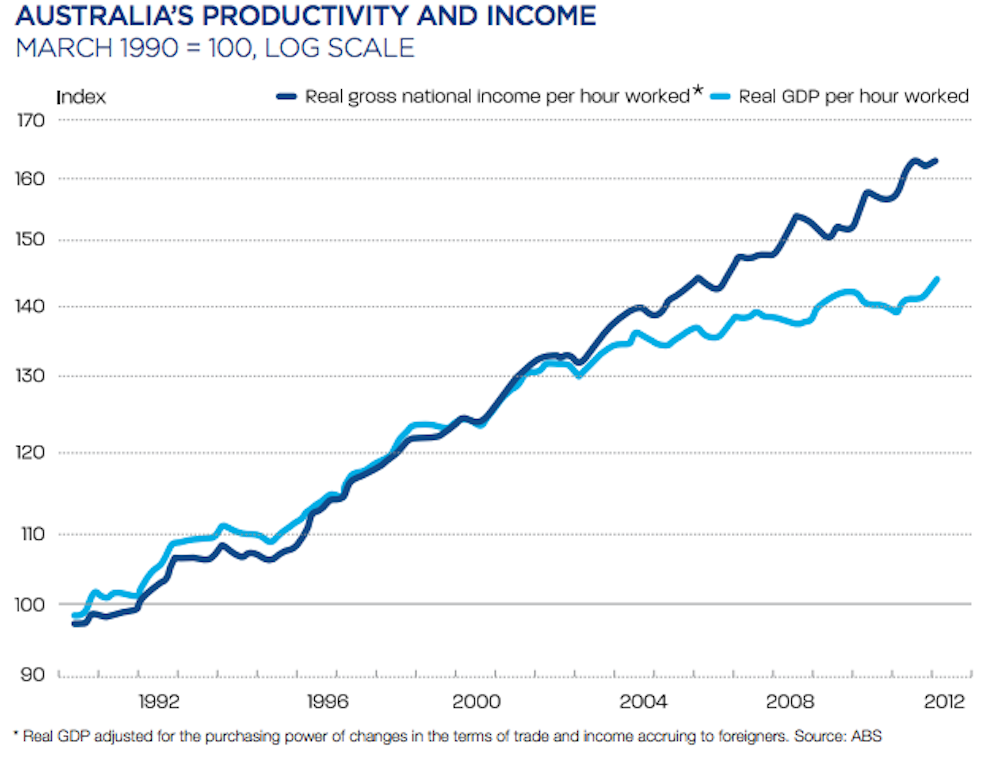

The first problem is the impending fall in Australia’s terms of trade from the heights reached during the commodity boom. The unprecedented rise in our terms of trade as a result of increased commodity prices delivered a massive boost to the growth in our national income in the early 2000s – around 15% over a five year period – and has not inaccurately been described as the “gift from China”. Combined with an effective stimulus, the boom helped to shield Australia from the worst of the global financial crisis and make our economy the envy of the world.

However, it also masked the second problem, which is the deterioration of Australia’s productivity performance since the 1990s. While this problem could be safely ignored, and was ignored in the past, as rising terms of trade took up the slack, it is now increasingly exposed as the commodity cycle runs its course. There were warning signs but many policy-makers and commentators mistakenly saw a cyclical event as structural change (see below).

Recently I prepared a detailed report with my colleagues Phil Toner and Renu Agarwal for the McKell Institute Understanding Productivity (2012), which explores Australia’s productivity slowdown and the policy measures that are being proposed to address it.

We found that just as the slowdown was previously ignored, it is now misinterpreted and exaggerated to justify measures that may have little or no relevance to our future productivity performance, and which may themselves have contributed to the slowdown.

The report notes that the most common measure of productivity performance is labour productivity, which measures the value of goods made or services provided either by hours worked, or by employed person.

Growth in this kind of productivity slowed in the early years of this century. This was less a result of the waning of the 1990s microeconomic reform agenda than a consequence of the increase in total employment and, at least since the global financial crisis, the decline in output growth.

This is an edited extract of a chapter from Pushing our luck: ideas for Australian progress from the Centre for Policy Development.