The Government’s Pre-election Fiscal Outlook (PEFO) was a non-event in one sense but it did underscore two important lessons, the absurdity of a 10 year forecast and the need for a stronger Parliamentary Budget Office.

Coming only 17 days after the 2016-17 budget, PEFO essentially confirmed the budget numbers. It would have been worrying if it had not done so, considering the PEFO comes from the same Treasury and Department of Finance that produced the budget.

The first important lesson we should draw from the budget and PEFO is the absurdity of costing spending or tax changes over a 10 year period. We are told for instance that the budget cut to the company tax rate to 25% will cost A$48.2 billion over 10 years, while Treasury noted that “as with all projections over 10 years these costings have considerable uncertainty attached to them”. Then why produce a number to one decimal point? It conveys an entirely unjustified degree of precision.

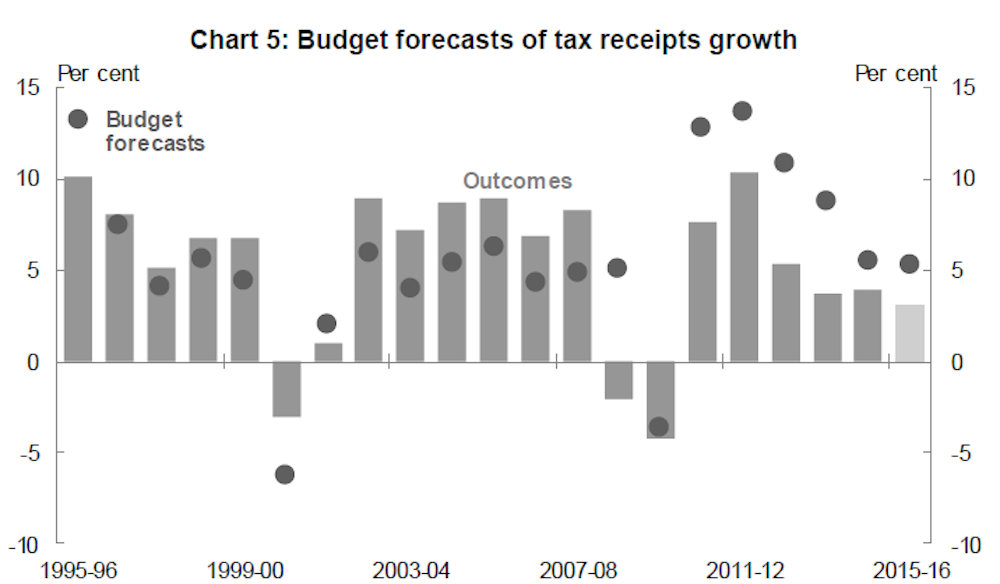

This year’sFederal Budget Paper No 1, Statement 7 is a sobering read. Chart 5, see below, shows the forecast errors for tax receipts, not 10 years out, but one year out. It compares the budget forecast for the forthcoming year with the actual outcome for that year.

In every one of the six years since 2010 the forecasts have been wrong by large margins – but worse, the errors are all in the same direction, that is, receipts have been less than forecast.

This forecasting record calls into serious question Treasury’s stubborn adherence to assumptions that repeatedly turn out to be wrong. The biggest single source of error is company tax receipts which were overestimated last year by A$3.5 billion, which makes a projected number like A$48.2billion over not one but 10 years an exercise in pure fiction, and to give the number to a decimal point is silly.

The budget forecasts (which apply to the next four years) as distinct from the projections (which extend for a further 6 years) come with “confidence intervals”. For example Treasury can only be 70% confident that tax receipts will turn out to be equal to the budget figure plus or minus A$30 billion (1.8% of GDP) by 2017-18, implying a 30% chance that the budget figure could be wrong by more than A$30 billion. The 90% confidence interval is wider - plus or minus A$50 billion (2.9% of GDP).

These are wide margins considering we are talking about outcomes only three or four years away. These margins get wider the further into the future. So 10 years out we really have no idea.

Perhaps the more important lesson from the budget and PEFO outcomes is the need to elevate the role of the Parliamentary Budget Office (PBO). It needs more teeth.

Its current role is “to inform the Parliament by providing independent and non-partisan analysis of the budget cycle, fiscal policy and the financial implications of proposals.” This needs strengthening.

Rather than just providing independent analysis of the budget the PBO should independently produce fiscal rules aimed at fiscal sustainability, ensuring that government debt is not set to rise inexorably under current settings and that our AAA credit rating is maintained. A government that breaches the fiscal rules should be called out by the PBO and suffer public censure.

The PBO should take account of the likelihood of the Senate passing legislation, of political compromises, of credit rating changes, and of international economic risks arising for example from commodity prices and China’s economy. The fiscal councils in Belgium, Denmark and Sweden operate rather like this and the evidence suggests that they have improved fiscal discipline by increasing the political costs on governments for lack of discipline.

We could go further and allow the PBO to operate like Australia’s independent Reserve Bank which controls the key monetary policy instrument and sets monetary policy independent of government. In that case the PBO would provide the government with a maximum spending limit and a deficit limit, consistent with fiscal targets.

The government would control the mix of spending and taxation consistent with these fiscal targets. Admittedly this is extreme and has not been tried in other countries, but with increasing government indebtedness around the world perhaps it should be.

The federal government’s debt has risen from minus A$45 billion (a net asset position) in 2007-8 to A$285 billion in 2015-16 (or 17.3% of GDP). The global financial crisis and subsequent drop in commodity prices had a lot to do with this.

But now that it is clear the economic cycle is not going to repair the budget, the government should tighten its belt to ensure that future generations are not picking up the tab. This is not currently happening – the budget forecasts net debt in four years’ time to be in fact higher than now, at 17.8% of GDP, and with no reduction in spending as a share of GDP.

A beefed-up PBO, acting as an independent fiscal agency, would call out the government on such a lack of fiscal discipline.