The international gas market was once constrained by pipelines and long-term trade deals. Now, it is rapidly globalising. Cross-border trade and investment in gas is growing, and national gas markets are now more connected than ever. This is largely a good thing, but for some countries these changes expose their consumers to the highs and lows of global markets.

Take the UK. Colleagues and I recently completed a research project on the country’s global gas challenge. As with everything from oil and wheat to laptops and mobile phones, the UK now sources most of its natural gas abroad. Import dependency – the ratio of gas imports to domestic consumption – hit an all-time high of over 50% in 2013.

This imported gas reaches the UK through pipelines from Norway’s offshore gas fields and the European gas market, and through specially designed ships carrying liquefied natural gas (LNG).

The international natural gas trade – and the UK’s gas supply chain – are undergoing a profound globalisation in which LNG’s much greater geographical flexibility versus pipeline gas is playing an important role.

Beyond the pipelines

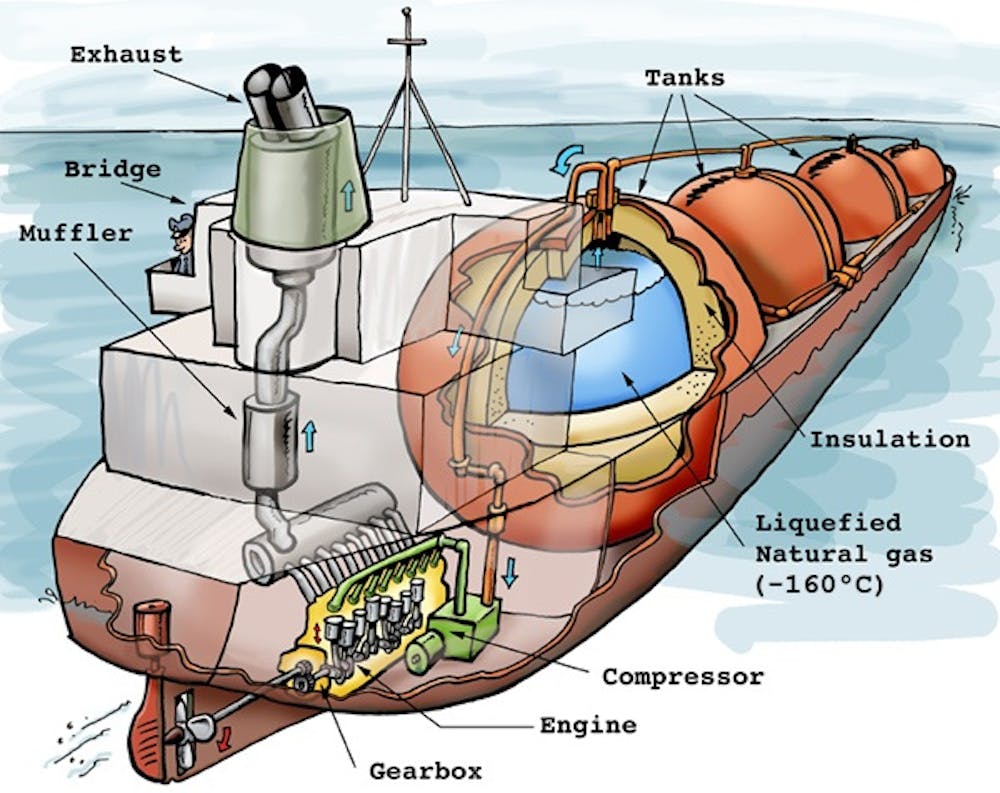

Liquefying natural gas makes it cheaper to transport and store. The gas, which is mainly methane, is cooled to below its boiling point of -162˚C so that its volume is reduced 600-fold. A tank of LNG stores roughly as much energy as the same amount of crude oil, making it commercially possible to move gas by either road or ship beyond the limits of the pipeline network.

{kind=link}

Though technology to turn natural gas into liquid is not new, major investments have driven a doubling of ocean-borne LNG trade so that it now accounts for a third of all internationally-traded gas. No longer constrained by pipelines, LNG is generating a more geographically complex and globally interconnected gas market.

The UK’s growing import dependency has drawn it into this globalising gas trade. The country’s three active terminals – South Hook and Dragon in south Wales, and the Isle of Grain near London – are capable of importing more than two-thirds of annual gas consumption. Building these terminals has opened the UK up to gas imported from far and wide.

Switching on and off

Physical infrastructure is one thing; whether gas actually shows up is quite another. The volume of liquefied gas arriving in the UK has been a lot less than physical capacity would suggest and highly variable over time.

UK imports of LNG:

Contracts concluded between LNG sellers and buyers in the UK allow cargo to be diverted to take advantage of regional differences in gas prices. Differences in price – and the strategies adopted by LNG producers in placing their gas – are important determinants of how much LNG flows to the UK and when.

LNG imports peaked at a third of UK gas consumption in 2011 as the country took delivery of liquefied gas originally intended for the US but displaced by growing shale gas production. Imports quickly fell away, however, in the second half of that year as LNG was diverted to Japan in the wake of the tsunami and the post-Fukushima nuclear shutdown.

Things changed when the large price differential between UK/European and Asian gas markets sharply narrowed, in part because of falling oil prices throughout 2014. In the past six months or so, LNG cargoes have begun to arrive in the UK more frequently.

New uncertainties

The capacity to import more gas makes the UK more resilient. Yet it also introduces new uncertainties and vulnerabilities.

The waxing and waning of liquefied gas imports indicates how the UK functions as a reserve market for global LNG: its physical infrastructure and market liquidity can absorb substantial cargoes, but much of this gas will go elsewhere when more attractive opportunities are available.

The geographical flexibility of LNG has diversified the UK’s supply options but, at the same time, it has also created new dependencies, with more than 90% of the UK’s LNG imports coming from Qatar. A substantial proportion of the UK’s current LNG supply depends, therefore, on the whim of Qatar Petroleum.

“Gas security” requires understanding the UK’s changing position in a globalising gas market: increasingly that means looking beyond Russia and Ukraine to consider the implications of new developments in global LNG.