Republican gains in this month’s election, which handed the GOP united control of Congress for the first time since 2006, have lifted hopes that the government can pass corporate tax reform next year.

But how justified is this optimism? Not only do Democrats and Republicans have different ideas of what “tax reform” means, there are also underlying fractures within the business community, the traditional constituency for reform. In addition, a recent tax reform experiment in Kansas that the GOP had planned to use as a partial model for their national efforts has led to plunging revenues and budget cuts, emboldening critics. Together, these disagreements make prospects for tax reform in 2015 uncertain at best.

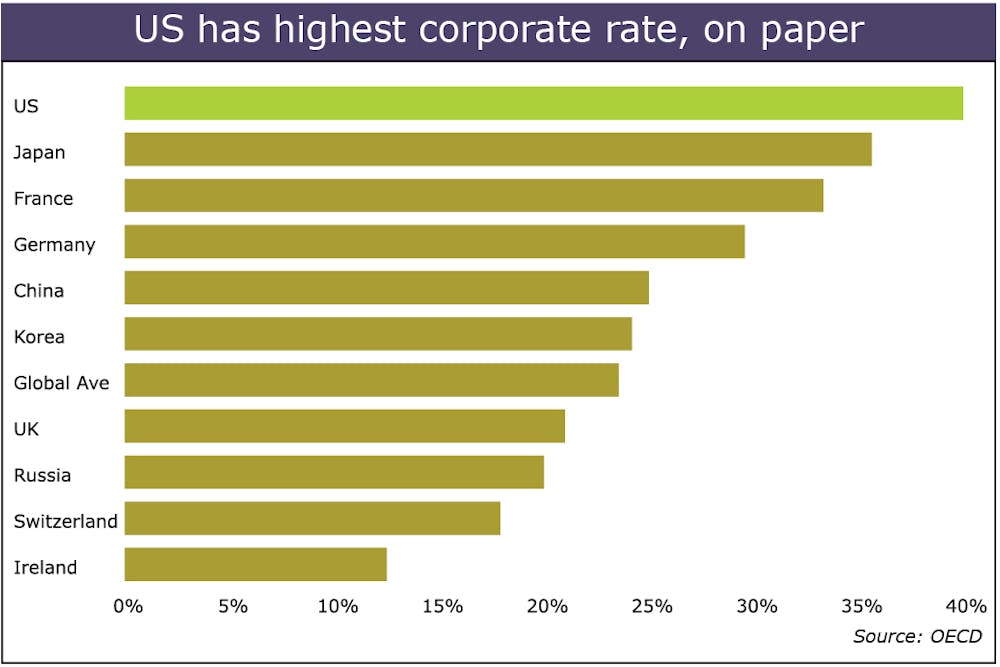

Democrats and Republicans generally agree on the need to lower federal corporate income tax rates. US rates are higher than many other wealthy countries. Yet many large companies, by taking advantage of a variety of exemptions, deductions and tax avoidance strategies, actually pay a much lower effective tax rate. Nonetheless, lawmakers and lobbyists argue that the high rates and very complex nature of the tax code still discourage investment and make tax enforcement needlessly difficult to manage.

Little common ground

Agreement largely ends here. For conservatives, the goal of tax reform has to go beyond merely recalibrating rates and closing tax “loopholes” while still ensuring that the corporate tax continues to generate the same amount of revenue. Many in the GOP would like to see overall corporate tax burdens reduced and major changes made to its structure. In particular, some Republicans have advocated that the US should adopt a “territorial” tax system in which only corporate profits earned in the US are taxed. The current method taxes all income that American multinational companies earn globally.

Many Democrats, on the other hand, would like corporate tax reform to generate new revenue that could be used for public investments. Much of this revenue would come in a one-time windfall from the repatriation of corporate profits now being held overseas which could then be taxed at a lower rate to generate funds for infrastructure spending. Liberals are also generally distressed at the declining role that the corporate income tax plays in the American revenue system. They see corporate tax reform as an important opportunity to restore this progressive tax to a more prominent role in revenue generation.

Satisfying disparate business interests

With control of both the House and the Senate in GOP hands, Democrats have less leverage over the corporate tax reform process than in the past, and this shift has increased the likelihood of legislative agreement around a proposal. However, Republicans still have to work out a reform plan that satisfies business interests.

Surprisingly, this might be the hardest task of all. Any tax reform plan creates winners and losers, and success hinges on being able to eliminate a wide variety of tax preferences built into the current system in order to pay for lower rates for everyone. The status quo may be inefficient and unwieldy, but some segments of the business community have benefited from what political scientists Paul Pierson and Jacob Hacker call “policy drift”. That occurs as policies like corporate taxation fail to keep up with changing circumstances on the ground. In other words, some businesses will actually pay higher tax rates if tax reform is successful. The beneficiaries, or winners, if the status quo remains in place tend to be large, multinational corporations that gain the most from our complicated and inefficient tax system

Bringing the losers to the table

Social science research has demonstrated that beneficiaries of tax preferences tend to be good at defending their turf. They also have the most political sway and potential to block tax reform from going forward. Successful reform will require agreeing on who the “losers” will be and getting them to come to the table anyway.

If these fractures prove difficult to manage, the GOP may end up only enacting a set of less comprehensive tax changes that reinforce rather than reform the corporate tax system. That could include extending some existing tax breaks that are set to expire at the end of the year and will likely be considered during the lame duck session, before the new Congress even takes office.

Kansas’ tax reform referendum

Last Tuesday’s election results at the state level may also point to an unexpected wrinkle in the upcoming debate over federal corporate tax reform. Kansas Governor Sam Brownback, who spearheaded massive tax cuts to the corporate and individual income tax in his state, was narrowly re-elected despite a heated debate over the state’s budget woes. Brownback’s tax cuts – and over-optimistic revenue projections that relied on assumptions that the tax cuts would stimulate greater economic growth – led to a major budget deficit in the state that deepened just weeks before the election. Then, a few days after Brownback retained office, state budget analysts announced the numbers had continued to worsen, and the state would have to cut an additional $280 million from the current fiscal year’s budget.

The governor’s reforms – or to critics, the radical implementation of supply-side economics – initially proved popular at the polls. However, the widening deficit in Kansas will give new ammunition to opponents of the Republican vision for corporate tax reform at the national level.

A unique plank of Brownback’s state-level tax reform passed in 2012 was a full exemption of business income for companies whose profits get taxed as part of the owner’s personal income, which is the case for many small businesses. Brownback’s office expected the change to eliminate income tax for almost 200,000 businesses. Republicans are eager to see similar provisions included in national corporate income tax reform, and the numbers coming out of Kansas will inject new controversy into the perennial discussion over the economic and fiscal effects of tax reform.

Electoral shifts in Congress have produced a window of opportunity for new debates on corporate tax reform. Whether the GOP can capitalize on these shifts will depend on the lessons they draw from the Kansas experiments, but most of all on how they manage the political task of balancing winners and losers among the business community.