A striking development in the Australian labour market in recent years has been the slow-down and low rate of growth in nominal wages. Low wage growth implies stalling living standards for workers; and has less obvious adverse consequences such as limiting shifts in wage relativities between jobs that are needed for the labour market to adjust efficiently.

Whichever measure of nominal wages you use, the story is the same. Wage growth is at its lowest since the measures began.

Take, for example, the Wage Price Index (WPI) (the measure that the ABS now prefers as a way to estimate wage growth). Between the December quarters of 2014 and 2015 it increased by 2.1%, the lowest rate since the series commenced in the late 1990s. Or, look at the main alternative measure, the series for ordinary full-time weekly earnings of adult males, which goes back to the early 1980s.

That measure increased by only 1% between November 2014 and 2015, again the lowest rate since the series began.

Why is wage growth so slow? My view is that events that are out of the ordinary usually only happen when there are multiple causes all pushing in the same direction. And I think this case of slow wage growth is an example.

Four main factors, all of which are pushing in the direction of slower wage growth, have happened to coincide. These factors are:

low consumer price inflation

low growth in labour productivity

a low level of labour demand

the effect on output prices due to the unwinding of the mining boom.

Low consumer price inflation and low labour productivity growth

Over extended periods of time wage growth tends to reflect growth in consumer prices and in labour productivity. Workers expect to be compensated for price inflation to maintain the purchasing power of their wage. As well, competition for their services ensures that workers receive a share of improvements in their productivity.

So a starting point for understanding why there is a slow rate of wage growth is to examine whether it might be explained by lower consumer price inflation and growth in labour productivity. Indeed, it does seem that this is part of this story.

The table above shows the annual rate of growth in the measure of ordinary full-time weekly earnings of adult males, and in the CPI and labour productivity for two time periods: 2013 to 2015, and 2008 to 2013 (December quarter). The annual rate of growth in nominal wages in the past two years was 2.3%, compared to 5.4% in the preceding five years.

Comparing across the same time periods, it can be seen that the annual rate of growth in CPI decreased by 0.85% and in labour productivity by 1.35%. Hence, slowing price inflation and labour productivity may have explained a substantial proportion of the decreasing rate of growth in nominal wages.

The economic downturn and slowing output prices

Over shorter periods of time wage growth varies with the business cycle. At present, the Australian economy is going through a downturn, and so it would be expected that this should depress the rate of wage growth.

In a downturn, there are fewer sectors of the economy where employers face constraints on the amount of workers they can hire. Hence fewer employers are likely to be forced to offer higher wages to hire extra workers or to get their employees to work extra hours. Therefore the average rate of growth in wages will decrease with the overall level of demand for labour.

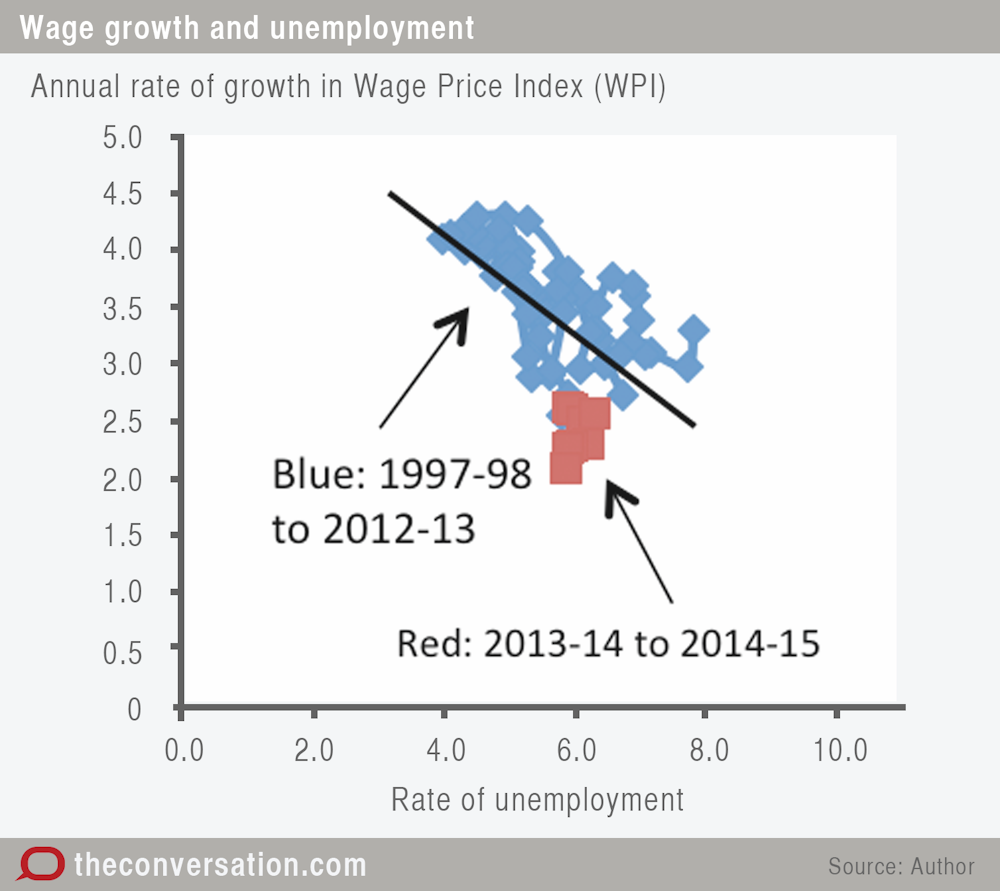

This also appears to be part of the story for current low wage growth. The chart below shows the relation between the rate of growth in the WPI and the level of labour demand, using the rate of unemployment as a proxy for labour demand. The chart shows that, given an average rate unemployment of 6% in 2015, based on the average experience, we would have expected annual growth in the WPI of about 3.3%.

This is certainly a slower rate of growth than at other times, which suggests that the current economic downturn is affecting wage growth. However, current growth in the WPI is also quite a bit lower than would be predicted from past experience.

An explanation for why the rate of growth in wages has been especially low in recent years may be the slow rate of growth in output prices. The unwinding of the mining boom has brought an end to the era of rapidly increasing output prices for Australian businesses. In fact, as the chart below shows, since mid-2011 there has been no growth in the average level of output prices in Australia. This absence of growth in the prices they receive for their output is likely to be imposing a major constraint on the capacity of employers to pay higher wages.

The future

None of the factors that have caused low nominal wage growth in recent years can be expected to disappear quickly. For example, the rate of economic growth in Australia may pick up, which will bring a rise in consumer price inflation and extra demand pressure on wages, but growth forecasts suggest this will happen only slowly.

Furthermore, other influences, such as the move to enterprise bargaining in the mid-1990s and the greater exposure of the Australian economy to international trade, mean that wage growth in Australia is on a permanently lower trajectory than two decades ago.

What therefore seems most likely in the immediate future is that, with a gradual reversal in the causes of low wage growth, there will be a slow rise in the rate of increase in nominal wages. So it’s too soon to be spending any big pay increase you might have been expecting to get.