The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

Australia’s economy is continuing down its path of slow and steady consolidation. The labour market is holding up and GDP growth remains solid. Consumer confidence, depressed after the government’s May budget, has improved slightly, as have several indicators of business sentiment.

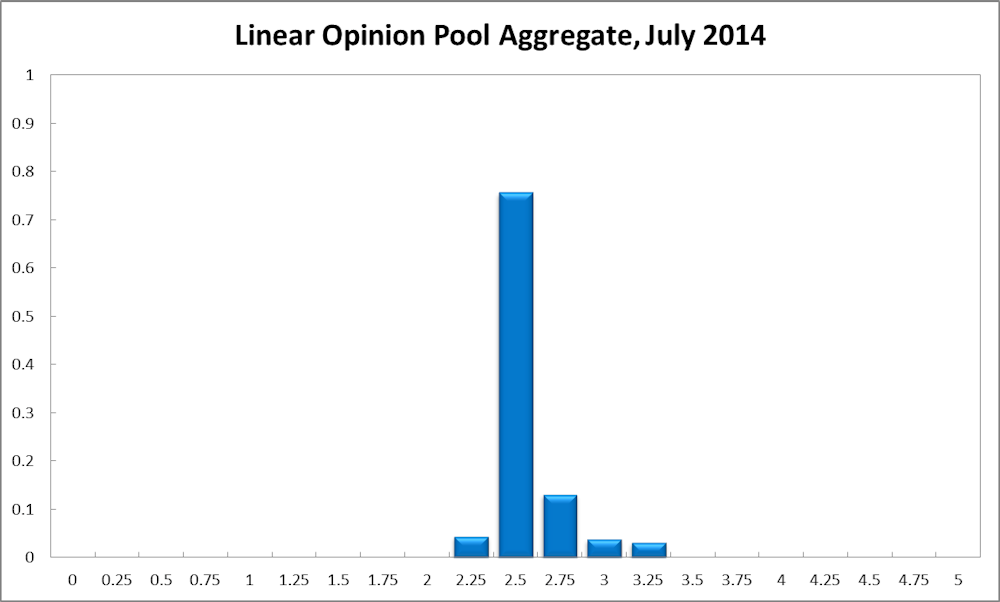

The CAMA RBA Shadow Board’s conviction that the cash rate ought to remain steady at 2.5% remains unshaken; it continues to attach a 76% probability that this is the appropriate setting.

The probability attached to a required rate cut has fallen two percentage points to 6%, while the probability of a required rate hike has risen slightly to 20%.

The unemployment rate again clocked in at 5.8%. Employment fell in May and fewer vacancies were posted, compared to the previous month. Labour costs have fallen slightly.

There is no new information about inflation until the release of second quarter inflation measures. The Australian dollar, now worth approximately 94 US cents, is strengthening slightly. Asset prices remain high, although there are possible signs that the housing market’s run is slowing, with new building approvals falling and price growth slowing. Some shadow board members, notably Professor Warwick McKibbin, remain concerned about the distortionary effects on asset prices of prolonged low interest rates.

But the global economy’s recovery remains shaky. US first quarter GDP growth was weak, with recent revisions to healthcare spending and a harsh winter indicating the world’s largest economy contracted by 2.9%. The Federal Reserve is continuing with its announced policy of phasing out monthly purchases but more weak economic data will presumably make the US central bank more doveish. European data is again mixed although tensions in the Ukraine appear to be waning which should reduce pressure on energy markets. Japan’s economy is improving, while China’s is steadying.

Promising signs for the Australian economy come from the rebound in the AIG’s manufacturing index, which in May climbed 4.5 points to 49.22, half a point shy of its 15-year average. With a slight improvement in consumer confidence as well as the AIG’s services index, we may just be seeing the fruits of sustained low interest rates. Should these indicators continue to improve over the next few months, the call for a tightening of monetary policy will likely grow louder.

What the CAMA Shadow Board believes

The consensus to keep the cash rate at its current level of 2.5% remains unchanged at 76%. The probability attached to a required rate cut has edged down to 4% (6% in June) while the probability of a required rate hike has risen to 20% (18% in June).

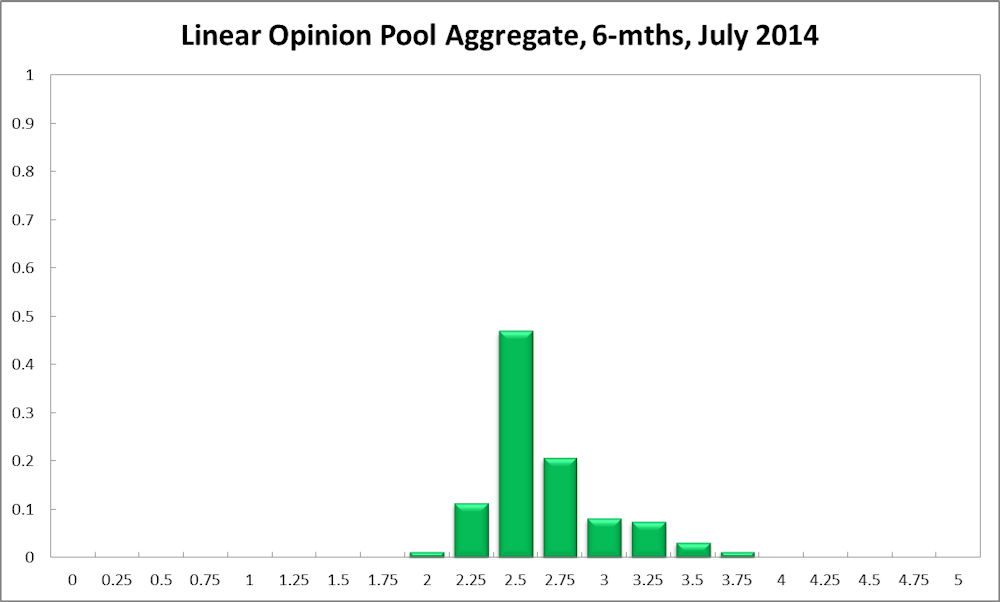

The six month probability is the cash rate should remain at 2.5% equals 47% (46% in June).

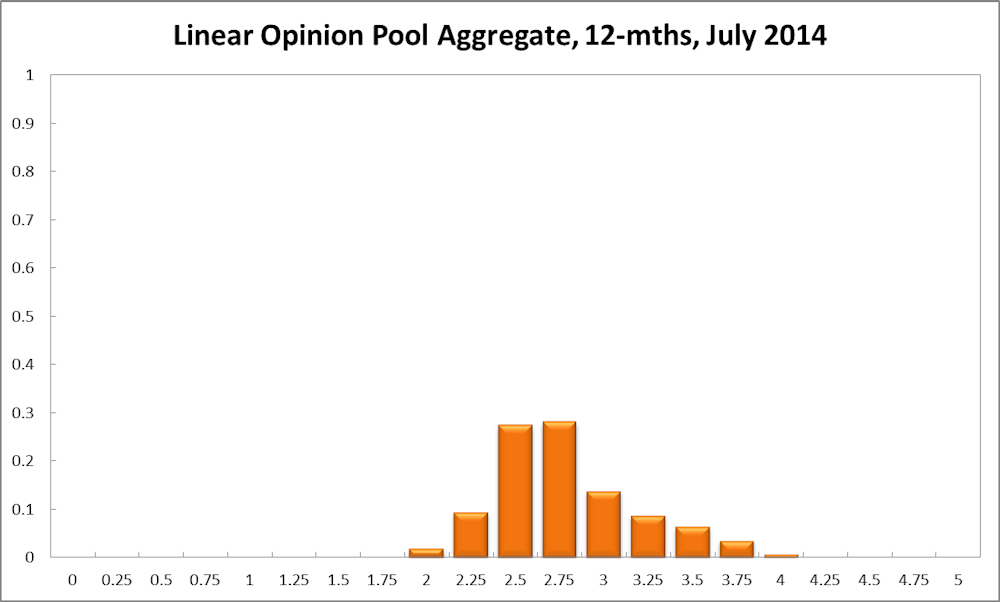

The estimated need for an interest rate increase is 41% (40% in June), while the need for a decrease has fallen to 12%. A year out, the Shadow Board members’ confidence in a required cash rate increase has risen to 61% (59% in June), the need for a decrease fell to 11% (13% in June), while the probability for a rate hold has remains at 28%.

Note: Mark Crosby did not vote in this round.

Comments from Shadow Reserve bank members

“Cash rate should remain unchanged.”

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Australia’s GDP growth was strong in the first quarter, although more timely indicators suggest some loss of momentum recently. New building approvals have fallen while growth in retail sales and housing prices has slowed.

Consumer sentiment has remained weak following cuts announced in the Federal budget. Local incomes are also being squeezed by the combination of falling commodity prices and a rising australian dollar in recent months. With inflation well contained and activity and income growth appearing to have softened in the past couple of months, there is little evidence to suggest that local interest rates will need to rise anytime soon.

At the same time, there are still signs that the domestic economy is being supported by low interest rates. Business surveys continue to suggest higher levels of confidence than last year and the labour market is showing signs of gradual improvement. I recommend that the cash rate is left unchanged this month.

“Australian rates are too low.”

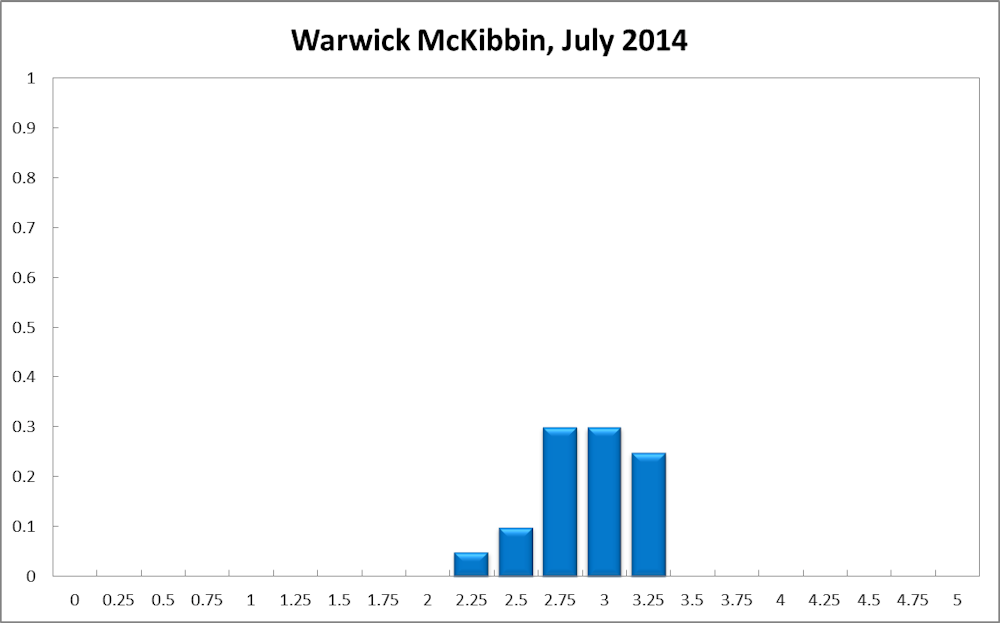

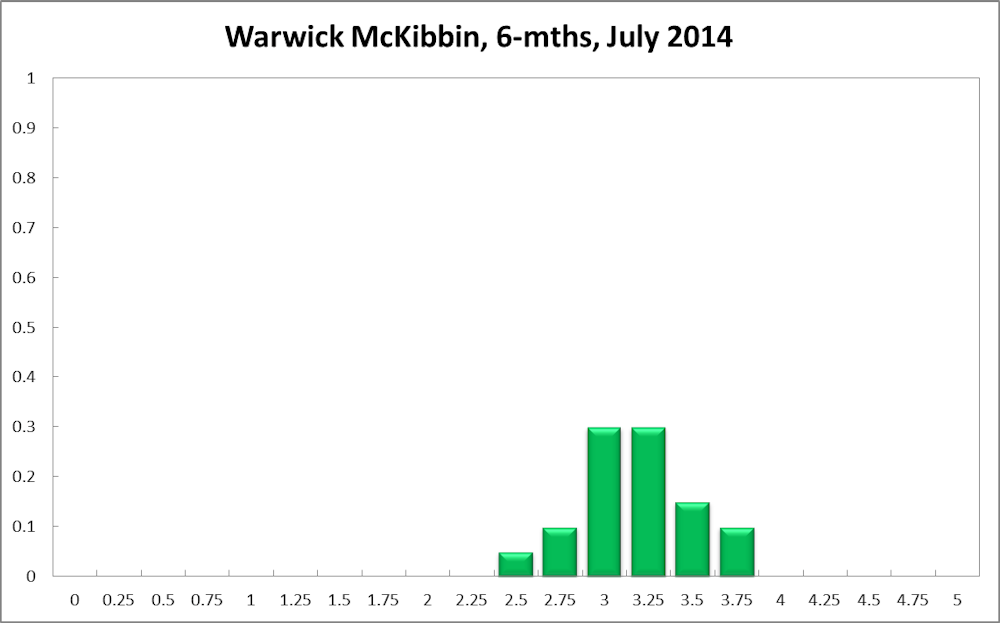

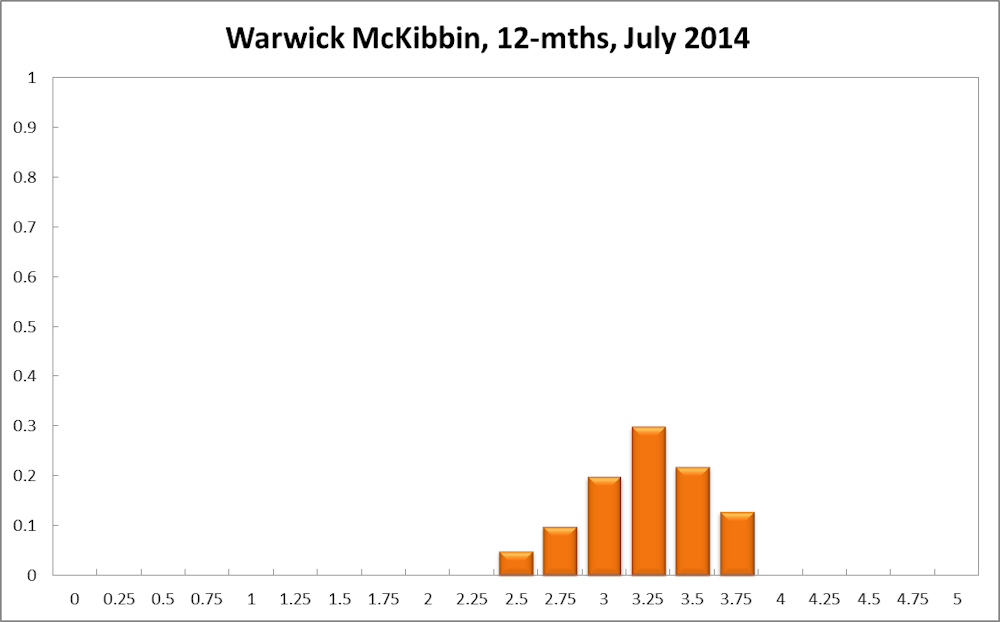

Warwick Mckibbin, Professor, Australian National University, CAMA:

In my view current Australian interest rates are too low. The problem is that monetary policy is aimed at stimulating non-mining parts of the economy particularly housing construction. Monetary policy should focus on the growth rate of nominal GDP as a benchmark to guide interest rates.

Given the current growth rate of nominal GDP of around 4-5% per year, a neutral monetary policy would be a risk adjusted interest rate of at least 4.5%. Allowing for risk adjustment, this suggests the Australian policy rate should be closer to 3% and possibly even 3.5%.

The current stance of monetary policy is at risk of increasing demand for assets, which will drive up the price of those assets. Unless there is a supply response, that will lead to pure capital gain and ultimately a bubble which will be costly to clean up.

Australia faces a shift in global portfolio preferences towards Australian assets as well ultra-loose monetary policy in major countries that experiences a financial crisis causing a search for robust currencies. This means the usual channel of loose monetary policy through weakening the $A is no longer viable even if it was the goal.

The focus on generating economic growth should be on the supply side of the economy through cost reductions (productivity improvements) improving competitiveness. There is not much a central bank can do about this except intellectual leadership in the debate.

Click here to view the full charts of all CAMA board members.

VERDICT FOR JULY: rates should remain steady.