The global market in government bonds has been bleeding red lately. “Bond market screams for help but no one answers”, says Bloomberg. It is “the worst start to a year in bonds since 2015”, according to the Financial Times.

Though bonds have been declining since last summer, the sell-off became a lot more violent in February. This meant that the yield on ten-year US Treasury bonds, which is inversely related to the price, rose by around 60% to peak at over 1.6% a couple of days ago, before falling back to 1.5% at the time of writing.

US 10-year bond yields

The US ten-year strongly influences the price of everything from mortgages to business loans in the US, and by extension around the world, so such a sharp rise has the potential to reduce borrowing and weaken the economic recovery from COVID –especially when there is so much debt in the global system. The world’s rampant stock markets responded by going into reverse in February as they factored in higher interest rates, as well as higher production costs because of surging commodity prices.

Bond prices can fall for several reasons. It can mean that the market thinks that economic growth is going to pick up (meaning investors shift their money into riskier investments). But it can also reflect fears that inflation is on the way without much accompanying economic growth, meaning that interest rates need to go higher so that lending is still profitable.

In the present case, it is a bit of both: the rollout of the vaccination programmes has made many observers more optimistic about the prospects of a recovery. But the rise in the price of commodities like oil, copper and coffee is more about pandemic-related supply issues than because this optimism has prompted a step-change in demand.

When Fed Reserve Chairman Jay Powell failed to announce any immediate intervention to put a floor under the sell-off in bonds during a public appearance in early March, it appeared to trigger more selling – a sign that falling bond prices have been more a reflection of fears than optimism.

Interestingly, in the hours since the new US$1.9 trillion (£1.4 trillion) US stimulus package has been agreed by Congress, the bond market and stock market have both been rising. Though there have been fears that sending US$1,400 stimulus cheques to most Americans will cause a further surge in inflation, the extra consumer demand will also prop up the economy. On balance, then, this appears to have been received as a net positive by the markets.

QE and perverse consequences

Any attempt to explain what is happening in the markets needs to be in the context of quantitative easing (QE). Shortly after the first wave of lockdowns in early 2020, central banks stepped in to help their national economies. They announced huge new QE plans in which they would create new money with which to buy government bonds and other financial assets. This drove up bond prices and hence kept yields (and interest rates) at very low levels to encourage as much borrowing from consumers and businesses as possible.

Most central banks originally began QE programmes after the 2007-09 financial crisis (besides the Bank of Japan, which began a few years earlier). This was primarily to help companies get access to capital to boost their business, in the hope that they would then hire staff, which would help to reduce unemployment rates that had been sent soaring after the crisis.

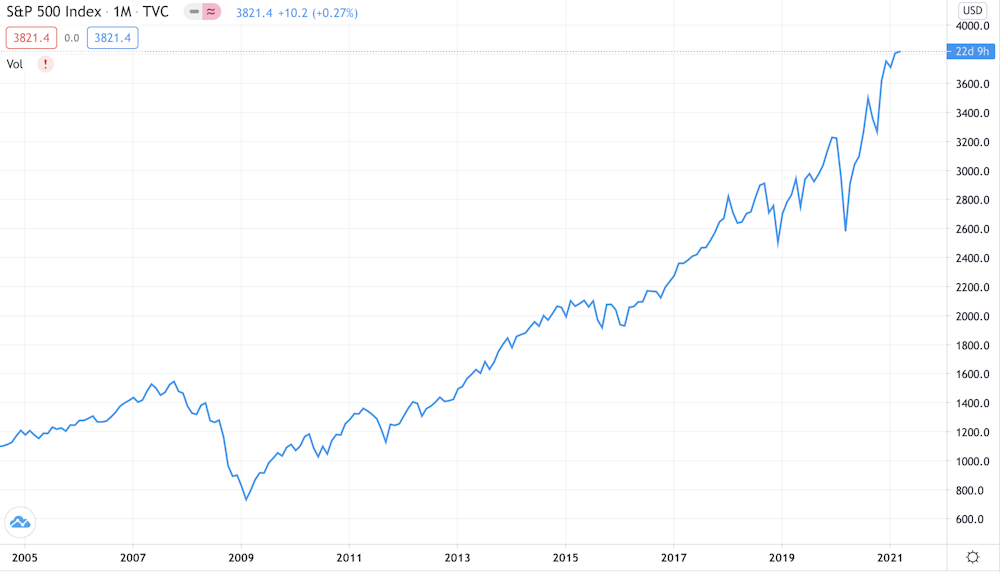

However, some companies took advantage of these low interest rates in another way: they borrowed cheaply and invested it in the stock market. With investors doing likewise, this has helped to drive the relentless rise in global stock markets over the past decade. It also helps to explain why these markets have been mainly climbing ever since the COVID panic sell-off of March 2020.

S&P 500 2005-2021

In the coming months, economies are going to reopen, but interest rates are to stay low. Fed Reserve Chairman Jay Powell may have declined to announce any new interventions to date, but it is fairly clear that he will only let yields rise so far.

This gives investors a great opportunity to continue taking advantage of the situation. So long as the gain from your investment in stocks is greater than the interest rate you have to pay on your borrowings, you are a winner. Better still, buy stocks in a company such as Apple whose bonds central banks have been buying as part of their QE activities. Apple is still trading at over double the lows of March 2020, even after the February correction.

But if you are not in a position to take advantage of this one-way bet, you are a loser. The central banks have already created a situation where major institutions like the biggest hedge funds and investment banks are achieving record earnings while many families are sinking into poverty on the back of the pandemic.

The endless stimulus is in danger of creating an ever more divided society. While it is true that the latest US package (and the support measures announced in the UK budget) will temporarily help those struggling during the pandemic, the shot in the arm is also another way of propping up markets that seem too overvalued to fail.

And if they can no longer survive without central bank life-support to keep bond yields low, the question is how to prop up the markets without exacerbating inequality. It’s not clear that anyone has the answer. It might be that a shift to a much more redistributive politics to offset the widening gap between rich and poor is about the best that we can hope for.