In case you had forgotten, electricity prices were a really big deal in the last federal election campaign in 2013, albeit often disguised under the rubric of axe the tax. Then Coalition spokesmen quite deliberately and repeatedly conflated the term carbon tax with electricity tax.

Clearly this was deemed acceptable in the court of public opinion. The justification was that Labor’s carbon pricing mechanism specifically targeted the electricity sector rather than other key emission intensive sectors of the economy such as land-use and transport.

This time round, in the 2016 election campaign, electricity prices are much less prominent. The Coalition would have us believe that by axing the tax they have driven electricity prices down. The flow on effect from reduced household expenses is a rise in consumer confidence. And that, we are told, is a key stimulus in maintaining growth in face of strong economic headwinds, and one we shouldn’t risk by changing government.

Given the success of the Coalition strategy in the last election, Labor is understandably gun-shy on electricity prices. It also likely wants to avoid provoking further Coalition delight in spruiking one of their favourite epithets - Electicity Bill.

However, this is all a bit strange, because wholesale electricity prices have almost doubled over what they were at the equivalent stage of the last election cycle. Incredibly, they are 300% above what they were in the 2010 election.

While wholesale prices are by no means the full story on electricity prices (see note 2), they are an important part of the story, and they are relevant here because carbon pricing was applied at the wholesale level.

The current record wholesale electricity prices provoke a number of questions, not the least of which is if electricity prices are so important why is consumer confidence so buoyant? Perhaps the answer is that wholesale electricity prices really don’t matter that much. And if that is the case then shouldn’t we fess up to the idea axing the tax may have been largely immaterial to our economic outlook.

What has happened to prices?

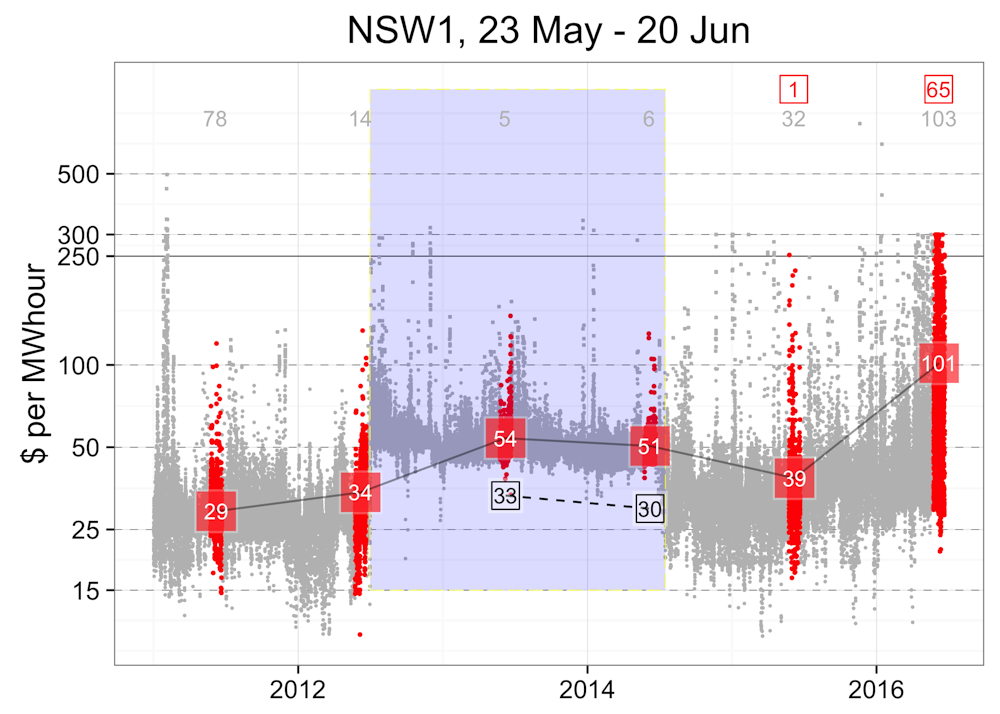

The figure below shows the wholesale electricity prices for NSW since 2011, with the four week period May 23 through June 20 indicated in red.

Prior to the start of carbon pricing period in July 2012, NSW wholesale prices averaged about $30-35 per megawatt hour, reflecting subdued market conditions due to an ongoing decline in demand for grid supplied electricity. That decline started around 2009 and continued to 2015. During the carbon pricing years (mid 2012 - mid 2014) prices jumped by ~ $20 per megawatt hour, but volatility remained very subdued as indicated by the narrow spread in the half hour prices. Following the rescinding of the carbon pricing legislation, wholesale prices fell back to near 2011 to early 2012 levels, but only for a short period of time. Over the last year prices have risen relentlessly, and volatility has returned dramatically. Half hourly prices now regularly hit $300 per megawatt hour.

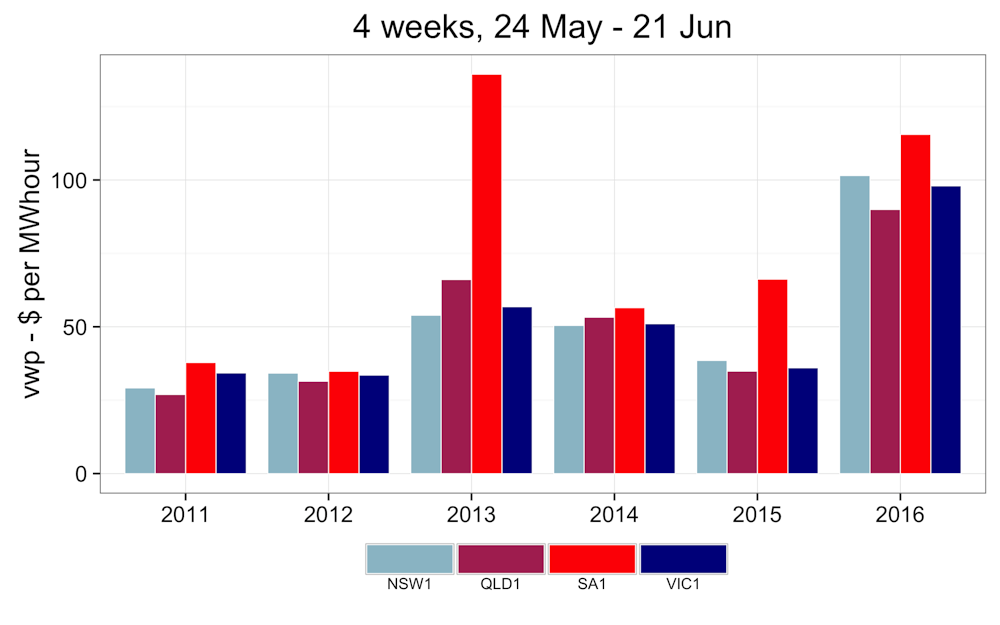

In NSW, at $101 per megawatt hour for the last four weeks, prices are almost 250% higher than the same period last year and almost double the equivalent period in the carbon pricing years. As illustrated below, other states show comparable trends, highlighting the exceptional nature of current prices. With the exception of anomalous prices in SA in 2013, current prices are way above anything that has been experienced in recent times.

Why are prices so high?

In fact, across the eastern states prices are now averaging higher than at any time since the height of the Millennium Drought in 2007. Then drought conditions affected the supply from hydro stations and from some thermal (coal) generation due to limited availability of cooling water. With demand then growing at around 2% each year, the drought tipped the balance between demand and supply, driving up prices dramatically. The breaking of the drought in 2009 coincided with a sustained decline in demand for electricity, at around 1% per year, though to 2015. Despite some power plant closures (notably Anglesea and Northern) and mothballing of others, the market has been in a state of considerable oversupply. Notwithstanding the impacts of carbon pricing, both prices and volatility have been remarkably low, especially in NSW and Victoria.

Since early 2016, rises in price arguably reflect a tightening of the demand-supply balance, as demand has begun to pick up.

While that is what might be expected in a market that is operating efficiently it is unlikely to be the full story, since there is still very substantial underutilised capacity. For example NSW black coal generation is still only operating at about two third capacity.

With such excess in relatively low cost generators, there is suspicion that the market is not operating particularly efficiently. This suggestion has been made recently in Queensland, and the AEMC has indeed flagged this issue with a request for rule change that is supported by both the regulator and the operator in their submissions (see Note 1).

Should electricity prices be part of the election agenda?

The question of price manipulation in our energy market is significant and speaks to existing market rules and the powers of the regulator. The question of market efficiency is crucial and should be addressed as part of a bipartisan approach to energy pricing.

The broader question, and one that will no doubt divide the key parties, relates to the causes and consequences of the current high electricity prices.

As alluded earlier, there would appear to be an incongruency in the Coalition position with regard to the current prices. However, it is important to note that the market prices have yet to flow through to domestic retail prices. The Coalition should be worried if and when they do. According to the logic of their own axe the tax mantra, any flow through of the wholesale price rises should stymie what it argues is a somewhat fragile consumer confidence. And along with that, so to the edifice it has built in its own attacks on Labor’s economic plans.

However, it is important to understand that even at $100 MWhour, wholesale prices are still less than 50% of the standing offer of most domestic retail contracts (see note 2). That there is fat in the system is indicated by the preparedness of most retailers to offer discounts of up to 30% on standing offers for such things as paying on time. Such sweeteners amount to more than the rise in wholesale price we have seen over the last year, and given the vertically integrated nature of the much of the industry, at least some of what is gained on the generation side can delivered by the retail side with little detriment to shareholder value.

For small generators without retail arms, and for new entrants, the wholesale price rises are a godsend. For the first time in a decade wholesale prices are approaching the cost of new generation build. With an ageing, emission intensive generation sector, there is an urgency for new build. No matter what technology is contemplated nothing is viable at less than a long-term average of about $70-$80 per megawatt hour.

So the current prices should be encouraging with regard to many of the challenges facing the industry. Providing current prices are reflective of an efficient market one would hope for bipartisan recognition that current prices are appropriate to the challenge at hand.

However it should also be acknowledged that such prices are not sufficient to encourage new build alone. We know that adding new capacity to the system without any withdrawal will collapse the price back to the marginal cost of coal-fired-power production of around $30 per megawatt hour or lower. This is particularly the case for new-build renewables which have the paradoxical effect of lowering market clearing prices because of their negligible short run costs. The prospect of such a collapse in prices has an analogue in what we have seen in the recent Saudi-led onslaught against largely US-based unconventional oil and gas, and is a powerful disincentive for new investment.

Given a primary driver for new build is the necessity to reduce emissions, rational economists are unanimous that the most efficient mechanism to facilitate transition to a low emission generation portfolio is to appropriately price emissions.

While we suspect the Prime Minister really does know this, we also know he is bound by a party room that is still a long way away from abandoning ideology for rationality, on this issue at least.

So on this point we must acknowledge any chance for bipartisanship ends. In the meanwhile, the rest of us might contemplate whether market prices would actually be any higher if we still had a carbon price.

While I don’t know the answer, my suspicion is probably not.

Notes

[1] The request for the rule change was motivated by recent incidences of strategic late bidding by generators and purported manipulation of the market by withdrawing Queensland generation, seen by some as a market distortion accentuated by the current market structure of 5 minute dispatch intervals and the 30 minute trading intervals.

[2] Of course, the elephant in the room in retail electricity prices remains the distribution network. The cost we are paying for the poles and wires remains unacceptably high, especially with the cost of capital tumbling across the world.